basic concept -...

TRANSCRIPT

SUMMARRY OF EXCISE CA MANOJ BATRA 1

BASIC CONCEPT

Union list Entry No. 84 CONSTITUTIONAL VALIDITY OF EXCISE

(1) on tobacco & other goods mfd. In India - CG Excise duty लगा सकती है

(2) लेककन alcohol, opium, narcotics etc. के ललए –SG के पास POWER है EXCISE DUTY लगाने के ललए

(3) But medical and toilet preparation containing alcohol, opium, narcotics etc

– CG के पास POWER है EXCISE DUTY लगाने के ललए

Organisational structure of central excise department

(1) CBEC (2) Chief CCE (3) CCE (4) Addl. Commissioner (5) joint

commissioner (6) AC/DC (7) SCE (8) Inspector

Sec 37B ORDER/INSTRUCTION/ DIRECTION ISSUED BY CBEC OR BINDING NATURE OF CIRCULARS

i. Order, instruction direction - Uniformity के ललए ISSUE हो सकत ेहै.

ii. ककसी PARTICULAR COMPANY के ललए ISSUE नह ीं हो सकत े

iii. 2 PURPOSE के ललए ISSUE हो सकत ेहै -CLASSIFICATION & LEVY OF

DUTY

iv. CEO को circulars follow करना MANDATORY है

v. Appellate authority, Assessee not bound by circulars. Rattan melting & Wire Industries JUDGEMENT of courts BINDING on department and NOT CIRCULAR Department can file appeal against circular

Whether it is necessary that the circular be issued under section 37B in order to be binding on the Department? Darshan Boardlam Ltd. v. UOI2013 (287) E.L.T. 401 (Guj.)

Sec 3 - CONDITION FOR LEVYING DUTY- (1) Excisable goods, (2) GOODS (MOVABLE & MARKETABLE), (3) MANUFACTURED Or produced in INDIA NOTES

(1) goods manufactured in ITW, EEZ, contiguous Zone - Liable to duty.

(2) J & K में goods manufacture ककये गए- EXCISE DUTY लगेगी

(3) SEZ में goods manufacture ककये गए- EXCISE DUTY नह ीं लगेगी

Sec 3(1)(a) - BED(CENVAT)- rates of FIRST SCH. OF CETA excluding goods mfd. In SEZ Sec 3(1)(b) - SED(in addition to BED) – Rates of SECOND SCH. excluding goods mfd. In SEZ

Sec 3(1A) - GOVT. IS also liable to PAY EXCISE DUTY

Proviso – sec 3 Removal by 100% EOU to DTA

(1) Pay Excise duty = [BCD + CVD + EC + SHEC + SP. CVD ]

(2) BCD- 50% Exempt, Sp. CVD- 100% Exempt, if sales tax leviable on subsequent sale.

(3) IF DUTY Chargeable w.r.t Value- VALUE AS PER CUSTOM,

(4) if more than 1 rate- Highest Rate of duty.

Clean energy cess [CEC]

1. Rs 50 per tonne levied on RAW COAL, RAW LIGNITE AND RAW PEAT 2. No EC,SHEC will be leviable. 3. CEC exempt on goods produced or extracted as per traditional and customary

rights enjoyed by local tribals in the state of MEGHALYA without any license or lease

4. No CCR of CEC, For payment of CEC, CCR can’t be utilised, CEC only paid through PLA.

SUMMARRY OF EXCISE CA MANOJ BATRA 2

Sec 2(d)- EXCISABLE GOODS- means goods

Specified in FIRST AND SECOND SCHEDULE TO CETA Subject to excise duty including Salt.

Nandi printers Pvt. Ltd– NIL RATE due to exemption - still goods are EXCISABLE. Solaris Chemtech (SC) – BLANK RATED goods are NON-EXCISABLE GOODS.

DIFERENCE BETWEEN NON- EXCISABLE AND NON-DUTIABLE

(1) Goods which are not listed in Tariff or goods which are mentioned in Tariff, but the column of rate of duty is blank are non-excisable goods. Excise law is not applicable on non excisable goods.

(2) “Non-dutiable goods” are excisable goods listed in Excise Tariff. Excise law is applicable to them, but they are not liable to excise duty. Non dutiable goods may be of two types-

(i) Nil duty goods-Tariff rate for such goods is nil, and (ii) Exempted goods-100% exemption is available under section 5A. for such goods.

Explanation to sec 2(d) -WHAT IS GOODS

Goods includes any article, material, substance which is capable of being bought and sold for a consideration and such goods shall be deemed to be marketable.

Goods- DCM - Movable & Marketable (Capable of being bought and sold)

Assessee Rule 2(c) CER 2002

ASSESSEE’ means 1. any person who is liable for payment of duty assessed or 2. a producer or manufacturer of excisable goods or 3. a registered person of a private warehouse in which excisable goods are

stored and 4. includes an authorized agent of such person.

MARKETABILITY

DCM - Actual sale not necessary [ मैंने बेचा नह ीं – IRRELEVANT है ]

Captive consumption

[ मैंने बेचा नह ीं –

IRRELEVANT है ] E.D

MANUFACTURE पर है

White machines- if FP exempt, intermediate product liable to duty. Dharmpal Satypal- Intermediate product removed to another premises of manufacturer

liable to duty, because marketable

Indian Aluminium Co. – Everything that is sold need not necessarily be marketable. (now overruled) Dross & Skimming will be marketable after amendment to Expl. To sec 2(d)

अगर PRODUCT SALE होता है – चाहे ORDINARY SALE हो या नह ीं- DEEMED MARKETABLE माना जायेगा

Cir 904/24/09- BAGGASE, ALUMINIUM /ZINC DROSS AND WASTE, RESIDUE arising during manufacture are capable of being sold for consideration would be marketable.

USHA RECTIFIER CORPN (I) LTD (SC)

TESTING EQUIPMENT manufacture -captively use for Testing of products manufactured.

Assesse said- मैंने बेचा नह ीं, क्योंकक बबकता नह ीं

Department- proved MARKETABLE..BALANCE SHEET में NOTE लगा था –

FOREIGN EXCHANGE को SAVE करने के ललए TESTING EQUIPMENT खुद MANUFACTURE ककया

MEDLEY PHARMACEUTICALS LTD.(SC)(2011)

Assesse said- मैंने बेचा नह ीं, क्योंकक DRUG CONTROL ACT SALE करने से मना करता है, ACT में ललखा है – SAMPLE पर ललखो – NOT FOR SALE

Department- proved MARKETABLE..DRUG ACT AND CENTRAL EXCISE ACT –दोनों अलग-अलग AREA में OPERATE करत ेहै

APSEB - Marketability doesn’t depend upon number of purchasers.

NICHOLAS PIRAMAL INDIA LTD

PERISHABLE GOODS जजनकी LIFE 2-3 DAYS है – DUTY लग सकती है IF

MARKETABLE DURING THAT PERIOD. CRUDE vitamin A has a life of 2 to 3 days, the

SUMMARRY OF EXCISE CA MANOJ BATRA 3

same shall be considered as marketable.

Bhor industries - Mere mention in tariff is not enough.

DUTY लगाने के ललए – OTHER CONITION SATISFY होनी चाहहए

Bata India Ltd Theoretical possibility of product being sold is not sufficient to establish marketability of product. The fact that product is sent outside for job work doesn’t establish its

marketability. DTRF बबना VULCANISATION PROCESS के REMOVE ककया गया –

IN THAT CONDITION, MARKETABLE नह ीं है

MANUFACTURE

DCM

- Every change is not mfr. There must be some transformation, A NEW AND DIFFERENT ARTICLE must emerge having distinctive name, character or use

OSNAR CHEMICAL PVT LTD.(2012)(SC)

Mixing polymers and additives to Bitumen results in emergence of Polymer Modified Bitumen and Crumbled Rubber Bitumen doesn’t amt to manufacture because no new product emerged but only its grade or quality improved.

Steel Authority of India Ltd. 2012 (SC)

process of removal of foreign materials from iron ore for concentration of such ore doesn’t amount to manufacture

GTC Industries Ltd. 2011 (Bom.)

the roll of aluminum foil was cut horizontally to make separate pieces of the foil

and word ‘PULL’ was embossed on it Doesn’t amount to manufacture.

DEEMED MFR

Sec 2(f)(ii) DEEMED MFR

Process specified in Section/chapter notes of 1st sch of CETA 1985 as amounting to manufacture.

Sec 2(f)(iii) DEEMED MFR

Packing/repacking of goods in unit container, labeling/relabeling of containers including declaration or alteration of RSP OF Goods specified in Third Sch. To CEA 1944.

EXAMPLES OF Deemed manufacture under the Central Excise Tariff Act, 1985, by way of Section Notes/Chapter Notes.

(i) In relation to iron and steel covered in Chapter 72, Chapter Note 5 provides that the process of galvanization shall amount to manufacture. (ii) In relation to audio or video tapes/CDs etc. falling under heading 8523 of Chapter 85, Chapter Note 10 provides that recording of sound or other phenomenon shall amount to manufacture. (iii) In relation to aluminium foils falling under heading 7607 of Chapter 76, Chapter Note 3 provides that process of cutting, slitting and printing of aluminium foils amount to manufacture.

Empire Industries Deemed mfr. Provision is constitutionally valid, may be covered in Entry 97

Johnson& Johnson Repacking from bulk pack to retail pack is manufacture. If there is no retail pack, then it is not manufacture.

Cir 910/30/2009 Repacking from tanker to drum is not manufacture

J.G. Glass industries -

Labeling doesn’t amount to manufacture Note- May be deemed mfr. For some items.

DUTIABILITY OF WASTE & SCRAP

Khandelwal Metal & Engg. works

(1) Waste & scrap, IF MARKETABLE would be chargeable to duty since it is covered in sub-headings of various chapters of tariff.

(2) Waste & Scrap DUTIABLE IF ARISE DURING MANUFACTURING PROCESS. (covered by word produced)

Grasim Industries Ltd 2011 (S.C.)

Metal scrap or waste generated during the repair of his worn out machineries/parts of cement manufacturing plant by a cement manufacturer doesn’t amounts to manufacture

WHETHER “ASSEMBLY” WOULD TANTAMOUNT TO “MANUFACTURE

(1) Assembly is a process of Putting Together A Number Of Items or parts of item to make a product (2) Assembly of various parts and components may tantamount to Manufacture If New Product Emerges,

which is movable and marketable. (3) assembly of imported kits of VTR with colour monitors imported in disassembled condition amounted to

SUMMARRY OF EXCISE CA MANOJ BATRA 4

manufacture since the end product had a distinct character and use (4) whereas Assembly Of Plant At Site Will Not Be Liable To Duty, If “Immovable Property” emerges after such

assembly

Processing and manufacturing

(1) If due to certain process a new and different product emerge having distinctive name character and use, then it is manufacture.

(2) Whereas if no new product emerge then it is process.

OSNAR CHEMICAL PVT LTD.(2012)(SC)

Mixing polymers and additives to Bitumen results in emergence of Polymer Modified Bitumen and Crumbled Rubber Bitumen doesn’t amount to manufacture because no new product emerged but only its grade or quality improved.

Sony Music Entertainment (I) Pvt Ltd.

Importing recorded audio and video discs in boxes each containing 50 discs. Each individual disc then packed in jewel boxes not amounting to manufacture.

State briefly whether the following circumstances would constitute “manufacture” for purpose of sec 2(f) of Central excise Tariff Act 1985

1) (1) Both inputs and the final product fall under the same tariff heading under the first schedule to CETA 2) (2) Inputs and final product fall under different tariff headings of tariff Act.

CHANGE IN TARIFF ENTRY- IRRELEVANT TO DECIDE WHETHER IT IS MANUFACTURE.

Laminated packing

- input and output covered by same tariff entry is irrelevant for determining manufacture

Technoweld indust

- input and output covered by different heading irrelevant for determining manufacture

SITE RELATED ACTIVITIES

Solid & Correct engineering Works (2010)(sc)

Affixation of Asphalt Drum/ Hot-mix Plant by nuts and bolts on foundation on earth to ensure wobble- free operation of the plant – Movable

Larsen & Tourbo Limited (2009)(Bom)

Fabrication, assembly, erection of waste water treatment is immovable. Merely bringing of duty paid parts at site doesn’t amount to manufacture.

Virgo industries (Engineers) Pvt. Ltd.

Signage Erected at Various petrol bunks of IOC are movable because capable of being shifted from one place to another without dismantling them.

Circular No. 58/1/2002

1. Site Related Activties-Movable, marketable, mfr., mentioned in CETA 2. change in identity in course of construction of a structure which is immovable property 3. Capable of being shifted as such, without dismantling – Movable 4. Examples of Immovable Property- turnkey project, huge tanks, Refrigeration/Air-conditioning Plants, Lifts and escalators.

MANUFACTURER- Sec 2(f)

M.M Khambatwala- Whether a RMS can be trated as manufacturer ? Are there any Exception to this ?

Raw material supplier is not manufacturer. Job-worker is treated as manufacturer, if relationship is principal to principal basis. IN THESE CASES A RAW MATERIAL SUPPLIER CAN BE TREATED AS MANUFACTURER: (i) There is no principal to principal relationship and job worker functions like a hired labour. (ii) Job Worker functions as an agent of raw material supplier. (iii) Job worker functions as labourer under the supervision and control of raw material supplier. (iv) Job workers are not manufacturing on their own account and they are dummy or bogus concerns and the arrangement is made to evade duty.

Food Specialist Brand owner is not manufacturer.

Provisional collection of

If duty imposed or increased in budget & declaration given in Bill then Rate of excise and custom duty applicable immediately on next day of budget. If subsequently cancelled or

SUMMARRY OF EXCISE CA MANOJ BATRA 5

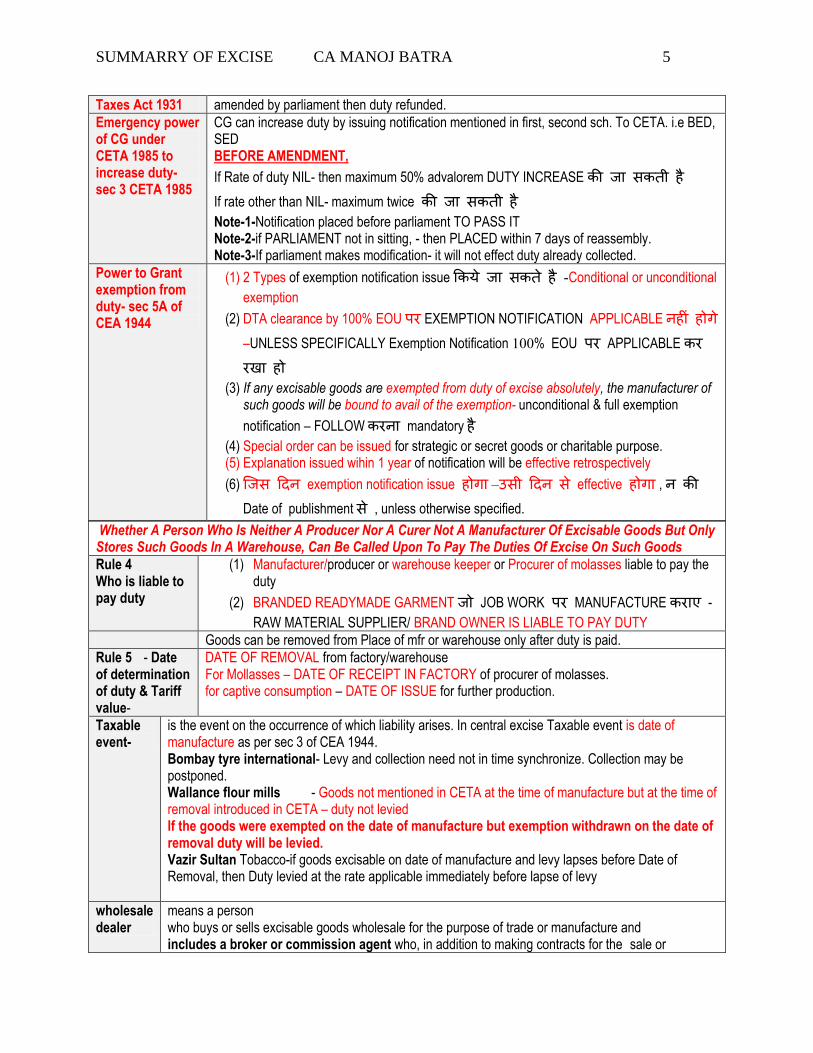

Taxes Act 1931 amended by parliament then duty refunded.

Emergency power of CG under CETA 1985 to increase duty- sec 3 CETA 1985

CG can increase duty by issuing notification mentioned in first, second sch. To CETA. i.e BED, SED BEFORE AMENDMENT,

If Rate of duty NIL- then maximum 50% advalorem DUTY INCREASE की जा सकती है

If rate other than NIL- maximum twice की जा सकती है

Note-1-Notification placed before parliament TO PASS IT Note-2-if PARLIAMENT not in sitting, - then PLACED within 7 days of reassembly. Note-3-If parliament makes modification- it will not effect duty already collected.

Power to Grant exemption from duty- sec 5A of CEA 1944

(1) 2 Types of exemption notification issue ककये जा सकत ेहै -Conditional or unconditional

exemption

(2) DTA clearance by 100% EOU पर EXEMPTION NOTIFICATION APPLICABLE नह ीं होगे –UNLESS SPECIFICALLY Exemption Notification 100% EOU पर APPLICABLE कर रखा हो

(3) If any excisable goods are exempted from duty of excise absolutely, the manufacturer of such goods will be bound to avail of the exemption- unconditional & full exemption

notification – FOLLOW करना mandatory है

(4) Special order can be issued for strategic or secret goods or charitable purpose. (5) Explanation issued wihin 1 year of notification will be effective retrospectively

(6) जजस हदन exemption notification issue होगा –उसी हदन स ेeffective होगा , न की Date of publishment से , unless otherwise specified.

Whether A Person Who Is Neither A Producer Nor A Curer Not A Manufacturer Of Excisable Goods But Only Stores Such Goods In A Warehouse, Can Be Called Upon To Pay The Duties Of Excise On Such Goods

Rule 4 Who is liable to pay duty

(1) Manufacturer/producer or warehouse keeper or Procurer of molasses liable to pay the duty

(2) BRANDED READYMADE GARMENT जो JOB WORK पर MANUFACTURE कराए -

RAW MATERIAL SUPPLIER/ BRAND OWNER IS LIABLE TO PAY DUTY

Goods can be removed from Place of mfr or warehouse only after duty is paid.

Rule 5 - Date of determination of duty & Tariff value-

DATE OF REMOVAL from factory/warehouse For Mollasses – DATE OF RECEIPT IN FACTORY of procurer of molasses. for captive consumption – DATE OF ISSUE for further production.

Taxable event-

is the event on the occurrence of which liability arises. In central excise Taxable event is date of manufacture as per sec 3 of CEA 1944. Bombay tyre international- Levy and collection need not in time synchronize. Collection may be postponed. Wallance flour mills - Goods not mentioned in CETA at the time of manufacture but at the time of removal introduced in CETA – duty not levied If the goods were exempted on the date of manufacture but exemption withdrawn on the date of removal duty will be levied. Vazir Sultan Tobacco-if goods excisable on date of manufacture and levy lapses before Date of Removal, then Duty levied at the rate applicable immediately before lapse of levy

wholesale dealer

means a person who buys or sells excisable goods wholesale for the purpose of trade or manufacture and includes a broker or commission agent who, in addition to making contracts for the sale or

SUMMARRY OF EXCISE CA MANOJ BATRA 6

purchase of excisable goods for others, stocks such goods belonging to others as an agent for the purpose of sale.

Rule- 21 REMISSION OF DUTY-

if FP lost or destroyed before removal BY NATURAL CAUSES BY UNAVOIDABLE ACCIDENT CLAIMED BY MANUFACTURER AS unfit for consumption for marketing –

DUTY REMITTED.

As per rule 3(5C) CCR 04, CCR reversed on IP, if duty remitted on FP.

Gupta Metal Sheets – in case of theft, no remission can be claimed Hindustan Zinc - Loss found during physical stock taking due to Shifting of concentrate , seepage of rain water, loading in Truck, de-bagging - remission allowed

VALUATION

Duty payable on Following Basis (1) Specific Duty- duty payable on the basis of weight, length, volume and thinkness etc.

Cigarette(length basis), Matches( per 100 boxes), sugar (per quintal basis) (2) Duty on basis of value

a. on Tariff Value Sec 3(2) b. on Maximum Retail Price Sec 4A c. on the basis of Valuation U/s 4

3. on the basis of production capacity/ compounded levy scheme

Sec 3(2) Tariff value- Av = fixed by CG, Sec 4 Not Applicable.

Sec 4A VALUATION OF GOODS ON THE BASIS OF RSP

1. AV= RSP DECLARED ON PACKGE LESS- Abatement 2. Conditions under which MRP base valuation shall apply u/s 4A (1) excisable

goods (2) sold in package (3) requirement in LMA 2009 to declare RSP (4) CG issued notification u/s 4A for those goods.

3. Explanation 1 -Retail Sale Price:- the maximum price at which the excisable goods in packaged form may be sold to the ultimate consumer and includes all taxes, local or otherwise, freight, transport charges, commission payable to dealers, and all charges towards advertisement, delivery, packing, forwarding and the like, as the case may be, and the price is the sole consideration for such sale.

LEGAL/PENAL ACTIONS TAKEN IN CASE THE RSP NOT MENTIONED OR UNDULY TAMPERED AFTER THE REMOVAL

4. excisable goods confiscated and value determined by CG, if (1) if excisable goods removed without declaring RSP (2) declares wrong RSP (3) tampers, obliterates or alters MRP After Removal.

Explanation 2

more than 1 RSP then RSP= maximum of such RSP

if altered to increase RSP then RSP = altered RSP

different RSP on different package for sale in different area then RSP= each such RSP for different area note- (1) in case of Quantity discount for MRP NOTIFIED GOODS- duty will be payable on MRP Less Abatement (2) in case of Sample of MRP notified goods, AV = MRP Less Abatement

SUMMARRY OF EXCISE CA MANOJ BATRA 7

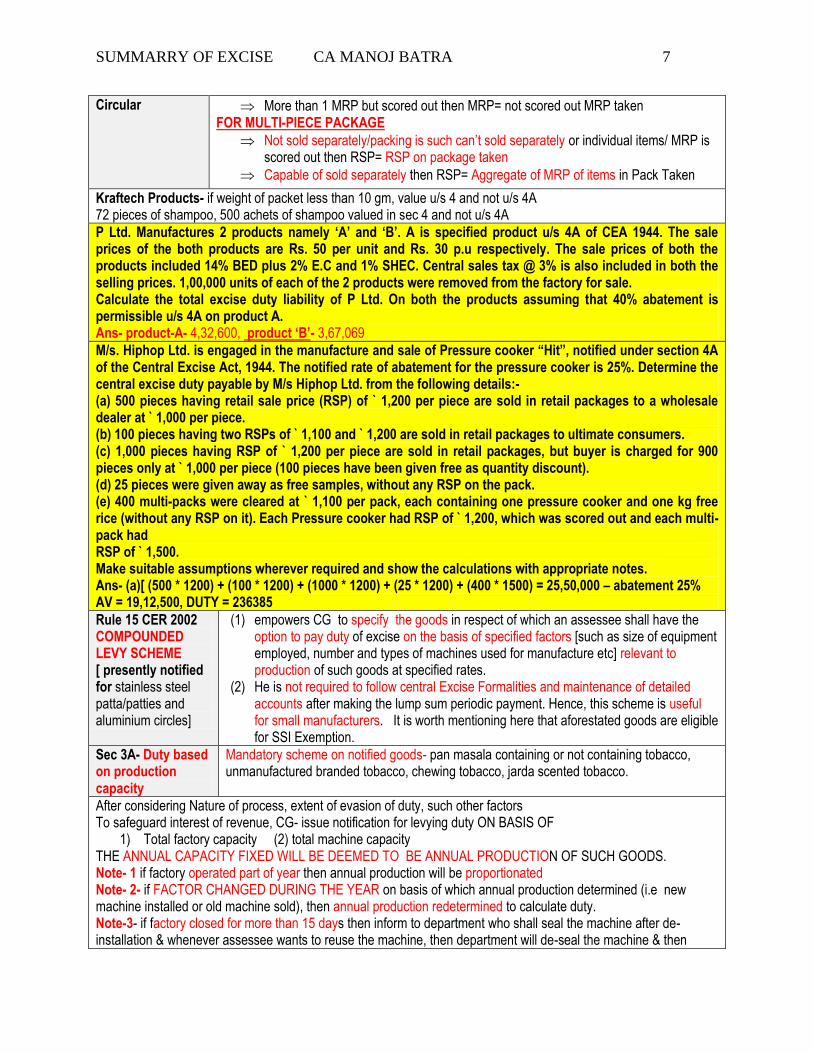

Circular More than 1 MRP but scored out then MRP= not scored out MRP taken FOR MULTI-PIECE PACKAGE

Not sold separately/packing is such can’t sold separately or individual items/ MRP is scored out then RSP= RSP on package taken

Capable of sold separately then RSP= Aggregate of MRP of items in Pack Taken

Kraftech Products- if weight of packet less than 10 gm, value u/s 4 and not u/s 4A 72 pieces of shampoo, 500 achets of shampoo valued in sec 4 and not u/s 4A

P Ltd. Manufactures 2 products namely ‘A’ and ‘B’. A is specified product u/s 4A of CEA 1944. The sale prices of the both products are Rs. 50 per unit and Rs. 30 p.u respectively. The sale prices of both the products included 14% BED plus 2% E.C and 1% SHEC. Central sales tax @ 3% is also included in both the selling prices. 1,00,000 units of each of the 2 products were removed from the factory for sale. Calculate the total excise duty liability of P Ltd. On both the products assuming that 40% abatement is permissible u/s 4A on product A. Ans- product-A- 4,32,600, product ‘B’- 3,67,069

M/s. Hiphop Ltd. is engaged in the manufacture and sale of Pressure cooker “Hit”, notified under section 4A of the Central Excise Act, 1944. The notified rate of abatement for the pressure cooker is 25%. Determine the central excise duty payable by M/s Hiphop Ltd. from the following details:- (a) 500 pieces having retail sale price (RSP) of ` 1,200 per piece are sold in retail packages to a wholesale dealer at ` 1,000 per piece. (b) 100 pieces having two RSPs of ` 1,100 and ` 1,200 are sold in retail packages to ultimate consumers. (c) 1,000 pieces having RSP of ` 1,200 per piece are sold in retail packages, but buyer is charged for 900 pieces only at ` 1,000 per piece (100 pieces have been given free as quantity discount). (d) 25 pieces were given away as free samples, without any RSP on the pack. (e) 400 multi-packs were cleared at ` 1,100 per pack, each containing one pressure cooker and one kg free rice (without any RSP on it). Each Pressure cooker had RSP of ` 1,200, which was scored out and each multi-pack had RSP of ` 1,500. Make suitable assumptions wherever required and show the calculations with appropriate notes. Ans- (a)[ (500 * 1200) + (100 * 1200) + (1000 * 1200) + (25 * 1200) + (400 * 1500) = 25,50,000 – abatement 25% AV = 19,12,500, DUTY = 236385

Rule 15 CER 2002 COMPOUNDED LEVY SCHEME [ presently notified for stainless steel patta/patties and aluminium circles]

(1) empowers CG to specify the goods in respect of which an assessee shall have the option to pay duty of excise on the basis of specified factors [such as size of equipment employed, number and types of machines used for manufacture etc] relevant to production of such goods at specified rates.

(2) He is not required to follow central Excise Formalities and maintenance of detailed accounts after making the lump sum periodic payment. Hence, this scheme is useful for small manufacturers. It is worth mentioning here that aforestated goods are eligible for SSI Exemption.

Sec 3A- Duty based on production capacity

Mandatory scheme on notified goods- pan masala containing or not containing tobacco, unmanufactured branded tobacco, chewing tobacco, jarda scented tobacco.

After considering Nature of process, extent of evasion of duty, such other factors To safeguard interest of revenue, CG- issue notification for levying duty ON BASIS OF

1) Total factory capacity (2) total machine capacity THE ANNUAL CAPACITY FIXED WILL BE DEEMED TO BE ANNUAL PRODUCTION OF SUCH GOODS. Note- 1 if factory operated part of year then annual production will be proportionated Note- 2- if FACTOR CHANGED DURING THE YEAR on basis of which annual production determined (i.e new machine installed or old machine sold), then annual production redetermined to calculate duty. Note-3- if factory closed for more than 15 days then inform to department who shall seal the machine after de-installation & whenever assessee wants to reuse the machine, then department will de-seal the machine & then

SUMMARRY OF EXCISE CA MANOJ BATRA 8

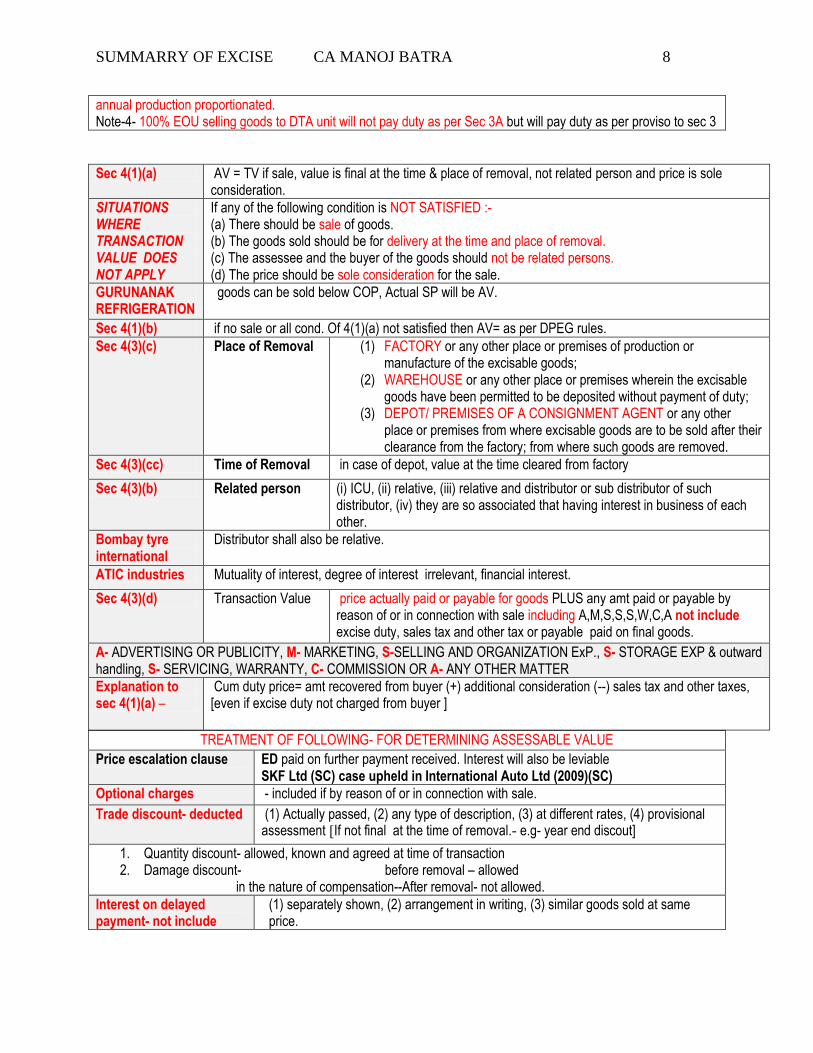

annual production proportionated. Note-4- 100% EOU selling goods to DTA unit will not pay duty as per Sec 3A but will pay duty as per proviso to sec 3

Sec 4(1)(a) AV = TV if sale, value is final at the time & place of removal, not related person and price is sole consideration.

SITUATIONS WHERE TRANSACTION VALUE DOES NOT APPLY

If any of the following condition is NOT SATISFIED :- (a) There should be sale of goods. (b) The goods sold should be for delivery at the time and place of removal. (c) The assessee and the buyer of the goods should not be related persons. (d) The price should be sole consideration for the sale.

GURUNANAK REFRIGERATION

goods can be sold below COP, Actual SP will be AV.

Sec 4(1)(b) if no sale or all cond. Of 4(1)(a) not satisfied then AV= as per DPEG rules.

Sec 4(3)(c) Place of Removal (1) FACTORY or any other place or premises of production or manufacture of the excisable goods;

(2) WAREHOUSE or any other place or premises wherein the excisable goods have been permitted to be deposited without payment of duty;

(3) DEPOT/ PREMISES OF A CONSIGNMENT AGENT or any other place or premises from where excisable goods are to be sold after their clearance from the factory; from where such goods are removed.

Sec 4(3)(cc) Time of Removal in case of depot, value at the time cleared from factory

Sec 4(3)(b) Related person (i) ICU, (ii) relative, (iii) relative and distributor or sub distributor of such distributor, (iv) they are so associated that having interest in business of each other.

Bombay tyre international

Distributor shall also be relative.

ATIC industries Mutuality of interest, degree of interest irrelevant, financial interest.

Sec 4(3)(d) Transaction Value price actually paid or payable for goods PLUS any amt paid or payable by reason of or in connection with sale including A,M,S,S,S,W,C,A not include excise duty, sales tax and other tax or payable paid on final goods.

A- ADVERTISING OR PUBLICITY, M- MARKETING, S-SELLING AND ORGANIZATION ExP., S- STORAGE EXP & outward handling, S- SERVICING, WARRANTY, C- COMMISSION OR A- ANY OTHER MATTER

Explanation to sec 4(1)(a) –

Cum duty price= amt recovered from buyer (+) additional consideration (--) sales tax and other taxes, [even if excise duty not charged from buyer ]

TREATMENT OF FOLLOWING- FOR DETERMINING ASSESSABLE VALUE

Price escalation clause ED paid on further payment received. Interest will also be leviable SKF Ltd (SC) case upheld in International Auto Ltd (2009)(SC)

Optional charges - included if by reason of or in connection with sale.

Trade discount- deducted (1) Actually passed, (2) any type of description, (3) at different rates, (4) provisional assessment [If not final at the time of removal.- e.g- year end discout]

1. Quantity discount- allowed, known and agreed at time of transaction 2. Damage discount- before removal – allowed

in the nature of compensation--After removal- not allowed.

Interest on delayed payment- not include

(1) separately shown, (2) arrangement in writing, (3) similar goods sold at same price.

SUMMARRY OF EXCISE CA MANOJ BATRA 9

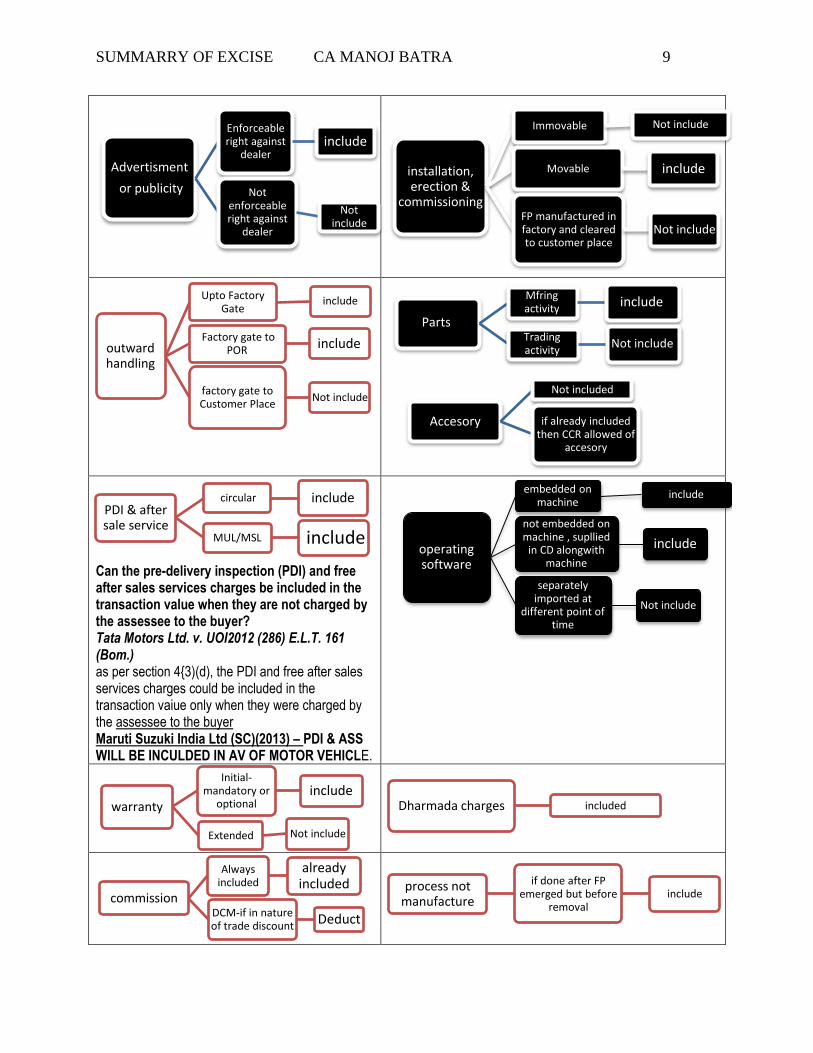

Can the pre-delivery inspection (PDI) and free after sales services charges be included in the transaction value when they are not charged by the assessee to the buyer? Tata Motors Ltd. v. UOI2012 (286) E.L.T. 161 (Bom.) as per section 4{3)(d), the PDI and free after sales services charges could be included in the transaction vaiue only when they were charged by the assessee to the buyer Maruti Suzuki India Ltd (SC)(2013) – PDI & ASS WILL BE INCULDED IN AV OF MOTOR VEHICLE.

Advertisment

or publicity

Enforceable right against

dealer include

Not enforceable right against

dealer

Not include

installation, erection &

commissioning

Immovable Not include

Movable include

FP manufactured in factory and cleared to customer place

Not include

outward handling

Upto Factory Gate

include

Factory gate to POR include

factory gate to Customer Place

Not include

Parts

Mfring activity

include

Trading activity

Not include

Accesory

Not included

if already included then CCR allowed of

accesory

PDI & after sale service

circular include

MUL/MSL include operating software

embedded on machine

include

not embedded on machine , supllied

in CD alongwith machine

include

separately imported at

different point of time

Not include

warranty

Initial- mandatory or

optional include

Extended Not include

Dharmada charges included

commission

Always included

already included

DCM-if in nature of trade discount

Deduct

process not manufacture

if done after FP emerged but before

removal include

SUMMARRY OF EXCISE CA MANOJ BATRA 10

price variation

increase

Pay duty on increase amt.

Int also payable

decrease refund

MRF CASE- NA

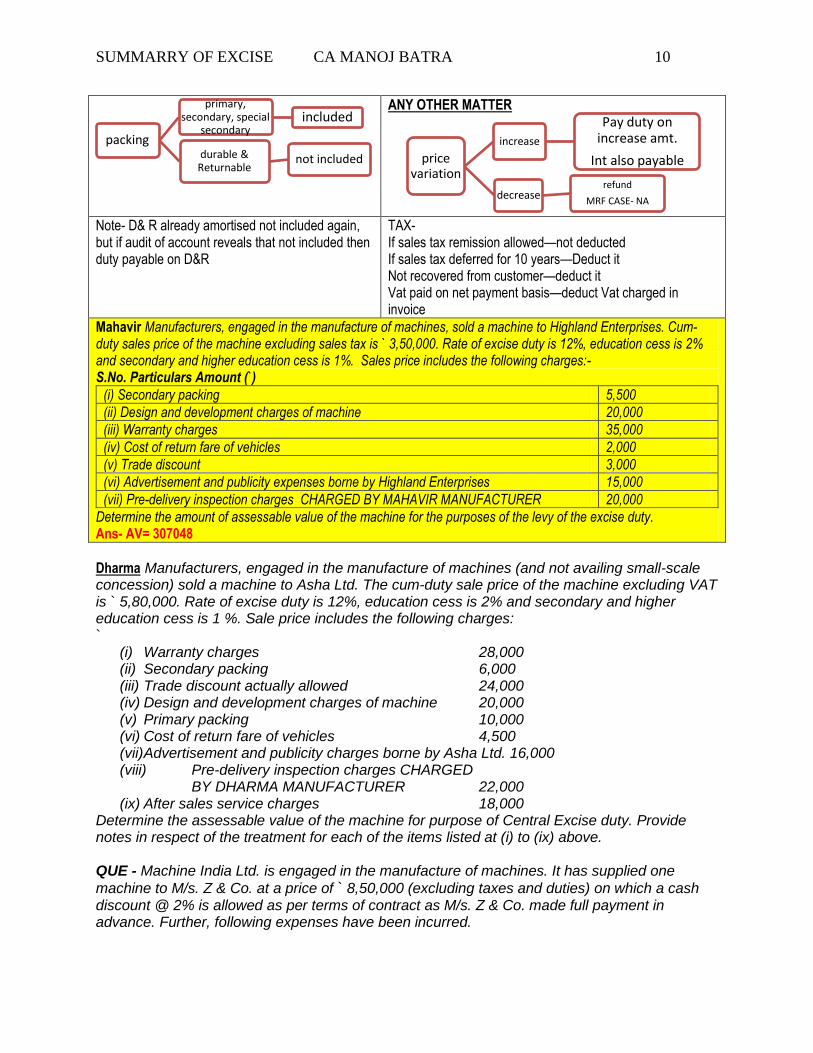

ANY OTHER MATTER

Note- D& R already amortised not included again, but if audit of account reveals that not included then duty payable on D&R

TAX- If sales tax remission allowed—not deducted If sales tax deferred for 10 years—Deduct it Not recovered from customer—deduct it Vat paid on net payment basis—deduct Vat charged in invoice

Mahavir Manufacturers, engaged in the manufacture of machines, sold a machine to Highland Enterprises. Cum-duty sales price of the machine excluding sales tax is ` 3,50,000. Rate of excise duty is 12%, education cess is 2% and secondary and higher education cess is 1%. Sales price includes the following charges:- S.No. Particulars Amount (`)

(i) Secondary packing 5,500

(ii) Design and development charges of machine 20,000

(iii) Warranty charges 35,000

(iv) Cost of return fare of vehicles 2,000

(v) Trade discount 3,000

(vi) Advertisement and publicity expenses borne by Highland Enterprises 15,000

(vii) Pre-delivery inspection charges CHARGED BY MAHAVIR MANUFACTURER 20,000

Determine the amount of assessable value of the machine for the purposes of the levy of the excise duty. Ans- AV= 307048

Dharma Manufacturers, engaged in the manufacture of machines (and not availing small-scale concession) sold a machine to Asha Ltd. The cum-duty sale price of the machine excluding VAT is ` 5,80,000. Rate of excise duty is 12%, education cess is 2% and secondary and higher education cess is 1 %. Sale price includes the following charges: `

(i) Warranty charges 28,000 (ii) Secondary packing 6,000 (iii) Trade discount actually allowed 24,000 (iv) Design and development charges of machine 20,000 (v) Primary packing 10,000 (vi) Cost of return fare of vehicles 4,500 (vii) Advertisement and publicity charges borne by Asha Ltd. 16,000 (viii) Pre-delivery inspection charges CHARGED

BY DHARMA MANUFACTURER 22,000 (ix) After sales service charges 18,000

Determine the assessable value of the machine for purpose of Central Excise duty. Provide notes in respect of the treatment for each of the items listed at (i) to (ix) above. QUE - Machine India Ltd. is engaged in the manufacture of machines. It has supplied one

machine to M/s. Z & Co. at a price of ` 8,50,000 (excluding taxes and duties) on which a cash discount @ 2% is allowed as per terms of contract as M/s. Z & Co. made full payment in advance. Further, following expenses have been incurred.

packing

primary, secondary, special

secondary included

durable & Returnable

not included

SUMMARRY OF EXCISE CA MANOJ BATRA 11

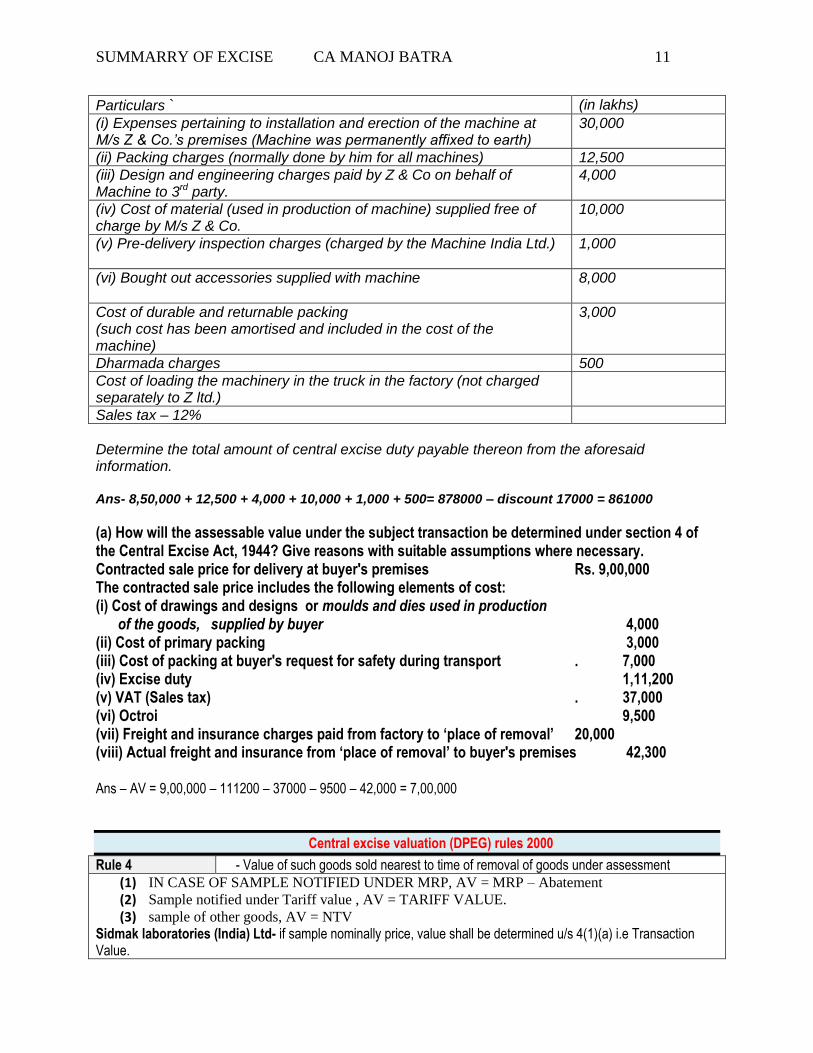

Particulars ` (in lakhs)

(i) Expenses pertaining to installation and erection of the machine at M/s Z & Co.’s premises (Machine was permanently affixed to earth)

30,000

(ii) Packing charges (normally done by him for all machines) 12,500

(iii) Design and engineering charges paid by Z & Co on behalf of Machine to 3rd party.

4,000

(iv) Cost of material (used in production of machine) supplied free of charge by M/s Z & Co.

10,000

(v) Pre-delivery inspection charges (charged by the Machine India Ltd.) 1,000

(vi) Bought out accessories supplied with machine 8,000

Cost of durable and returnable packing (such cost has been amortised and included in the cost of the machine)

3,000

Dharmada charges 500

Cost of loading the machinery in the truck in the factory (not charged separately to Z ltd.)

Sales tax – 12%

Determine the total amount of central excise duty payable thereon from the aforesaid information. Ans- 8,50,000 + 12,500 + 4,000 + 10,000 + 1,000 + 500= 878000 – discount 17000 = 861000

(a) How will the assessable value under the subject transaction be determined under section 4 of the Central Excise Act, 1944? Give reasons with suitable assumptions where necessary. Contracted sale price for delivery at buyer's premises Rs. 9,00,000 The contracted sale price includes the following elements of cost: (i) Cost of drawings and designs or moulds and dies used in production of the goods, supplied by buyer 4,000 (ii) Cost of primary packing 3,000 (iii) Cost of packing at buyer's request for safety during transport . 7,000 (iv) Excise duty 1,11,200 (v) VAT (Sales tax) . 37,000 (vi) Octroi 9,500 (vii) Freight and insurance charges paid from factory to ‘place of removal’ 20,000 (viii) Actual freight and insurance from ‘place of removal’ to buyer's premises 42,300 Ans – AV = 9,00,000 – 111200 – 37000 – 9500 – 42,000 = 7,00,000

Central excise valuation (DPEG) rules 2000

Rule 4 - Value of such goods sold nearest to time of removal of goods under assessment

(1) IN CASE OF SAMPLE NOTIFIED UNDER MRP, AV = MRP – Abatement (2) Sample notified under Tariff value , AV = TARIFF VALUE.

(3) sample of other goods, AV = NTV Sidmak laboratories (India) Ltd- if sample nominally price, value shall be determined u/s 4(1)(a) i.e Transaction Value.

SUMMARRY OF EXCISE CA MANOJ BATRA 12

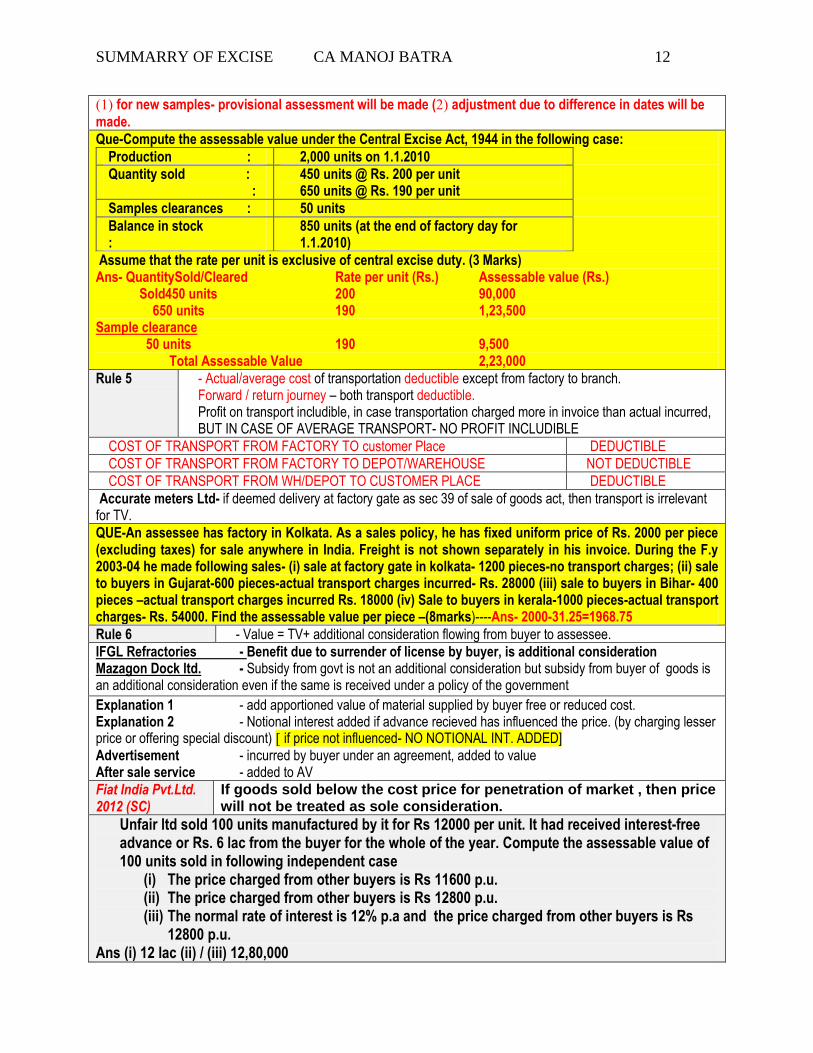

(1) for new samples- provisional assessment will be made (2) adjustment due to difference in dates will be

made.

Que-Compute the assessable value under the Central Excise Act, 1944 in the following case:

Production : 2,000 units on 1.1.2010

Quantity sold : :

450 units @ Rs. 200 per unit 650 units @ Rs. 190 per unit

Samples clearances : 50 units

Balance in stock :

850 units (at the end of factory day for 1.1.2010)

Assume that the rate per unit is exclusive of central excise duty. (3 Marks) Ans- QuantitySold/Cleared Rate per unit (Rs.) Assessable value (Rs.) Sold450 units 200 90,000 650 units 190 1,23,500 Sample clearance 50 units 190 9,500 Total Assessable Value 2,23,000

Rule 5 - Actual/average cost of transportation deductible except from factory to branch. Forward / return journey – both transport deductible. Profit on transport includible, in case transportation charged more in invoice than actual incurred, BUT IN CASE OF AVERAGE TRANSPORT- NO PROFIT INCLUDIBLE

COST OF TRANSPORT FROM FACTORY TO customer Place DEDUCTIBLE

COST OF TRANSPORT FROM FACTORY TO DEPOT/WAREHOUSE NOT DEDUCTIBLE

COST OF TRANSPORT FROM WH/DEPOT TO CUSTOMER PLACE DEDUCTIBLE

Accurate meters Ltd- if deemed delivery at factory gate as sec 39 of sale of goods act, then transport is irrelevant for TV.

QUE-An assessee has factory in Kolkata. As a sales policy, he has fixed uniform price of Rs. 2000 per piece (excluding taxes) for sale anywhere in India. Freight is not shown separately in his invoice. During the F.y 2003-04 he made following sales- (i) sale at factory gate in kolkata- 1200 pieces-no transport charges; (ii) sale to buyers in Gujarat-600 pieces-actual transport charges incurred- Rs. 28000 (iii) sale to buyers in Bihar- 400 pieces –actual transport charges incurred Rs. 18000 (iv) Sale to buyers in kerala-1000 pieces-actual transport charges- Rs. 54000. Find the assessable value per piece –(8marks)----Ans- 2000-31.25=1968.75

Rule 6 - Value = TV+ additional consideration flowing from buyer to assessee.

IFGL Refractories - Benefit due to surrender of license by buyer, is additional consideration Mazagon Dock ltd. - Subsidy from govt is not an additional consideration but subsidy from buyer of goods is an additional consideration even if the same is received under a policy of the government

Explanation 1 - add apportioned value of material supplied by buyer free or reduced cost. Explanation 2 - Notional interest added if advance recieved has influenced the price. (by charging lesser price or offering special discount) [ if price not influenced- NO NOTIONAL INT. ADDED]

Advertisement - incurred by buyer under an agreement, added to value After sale service - added to AV

Fiat India Pvt.Ltd. 2012 (SC)

If goods sold below the cost price for penetration of market , then price will not be treated as sole consideration.

Unfair ltd sold 100 units manufactured by it for Rs 12000 per unit. It had received interest-free advance or Rs. 6 lac from the buyer for the whole of the year. Compute the assessable value of 100 units sold in following independent case

(i) The price charged from other buyers is Rs 11600 p.u. (ii) The price charged from other buyers is Rs 12800 p.u. (iii) The normal rate of interest is 12% p.a and the price charged from other buyers is Rs

12800 p.u. Ans (i) 12 lac (ii) / (iii) 12,80,000

SUMMARRY OF EXCISE CA MANOJ BATRA 13

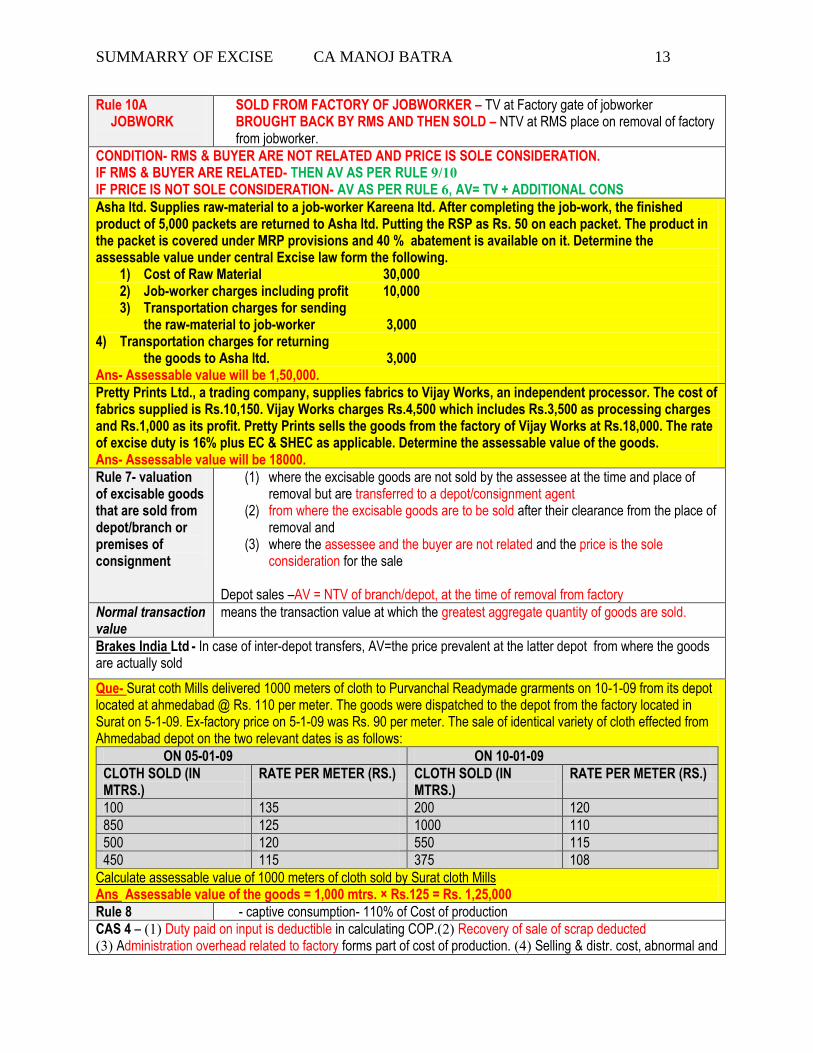

Rule 10A JOBWORK

SOLD FROM FACTORY OF JOBWORKER – TV at Factory gate of jobworker BROUGHT BACK BY RMS AND THEN SOLD – NTV at RMS place on removal of factory from jobworker.

CONDITION- RMS & BUYER ARE NOT RELATED AND PRICE IS SOLE CONSIDERATION. IF RMS & BUYER ARE RELATED- THEN AV AS PER RULE 9/10 IF PRICE IS NOT SOLE CONSIDERATION- AV AS PER RULE 6, AV= TV + ADDITIONAL CONS

Asha ltd. Supplies raw-material to a job-worker Kareena ltd. After completing the job-work, the finished product of 5,000 packets are returned to Asha ltd. Putting the RSP as Rs. 50 on each packet. The product in the packet is covered under MRP provisions and 40 % abatement is available on it. Determine the assessable value under central Excise law form the following.

1) Cost of Raw Material 30,000 2) Job-worker charges including profit 10,000 3) Transportation charges for sending

the raw-material to job-worker 3,000 4) Transportation charges for returning the goods to Asha ltd. 3,000 Ans- Assessable value will be 1,50,000.

Pretty Prints Ltd., a trading company, supplies fabrics to Vijay Works, an independent processor. The cost of fabrics supplied is Rs.10,150. Vijay Works charges Rs.4,500 which includes Rs.3,500 as processing charges and Rs.1,000 as its profit. Pretty Prints sells the goods from the factory of Vijay Works at Rs.18,000. The rate of excise duty is 16% plus EC & SHEC as applicable. Determine the assessable value of the goods. Ans- Assessable value will be 18000.

Rule 7- valuation of excisable goods that are sold from depot/branch or premises of consignment

(1) where the excisable goods are not sold by the assessee at the time and place of removal but are transferred to a depot/consignment agent

(2) from where the excisable goods are to be sold after their clearance from the place of removal and

(3) where the assessee and the buyer are not related and the price is the sole consideration for the sale

Depot sales –AV = NTV of branch/depot, at the time of removal from factory

Normal transaction value

means the transaction value at which the greatest aggregate quantity of goods are sold.

Brakes India Ltd - In case of inter-depot transfers, AV=the price prevalent at the latter depot from where the goods are actually sold

Que- Surat coth Mills delivered 1000 meters of cloth to Purvanchal Readymade grarments on 10-1-09 from its depot located at ahmedabad @ Rs. 110 per meter. The goods were dispatched to the depot from the factory located in Surat on 5-1-09. Ex-factory price on 5-1-09 was Rs. 90 per meter. The sale of identical variety of cloth effected from Ahmedabad depot on the two relevant dates is as follows:

ON 05-01-09 ON 10-01-09

CLOTH SOLD (IN MTRS.)

RATE PER METER (RS.) CLOTH SOLD (IN MTRS.)

RATE PER METER (RS.)

100 135 200 120

850 125 1000 110

500 120 550 115

450 115 375 108

Calculate assessable value of 1000 meters of cloth sold by Surat cloth Mills Ans Assessable value of the goods = 1,000 mtrs. × Rs.125 = Rs. 1,25,000

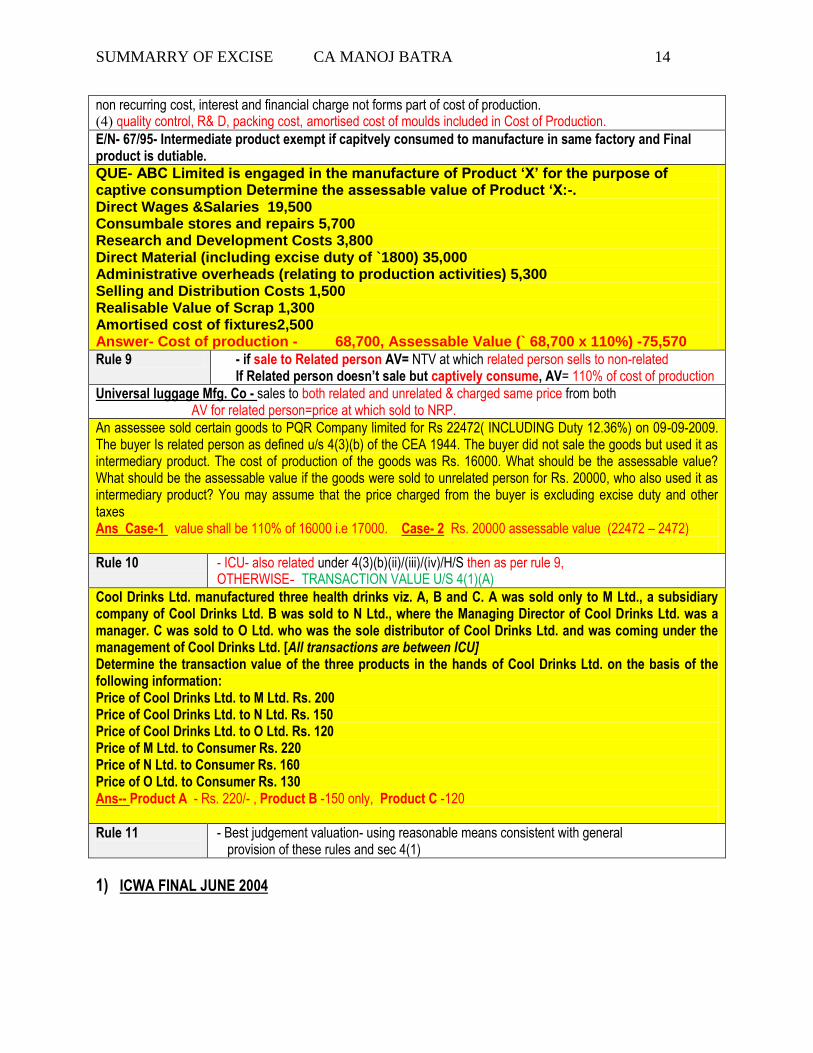

Rule 8 - captive consumption- 110% of Cost of production

CAS 4 – (1) Duty paid on input is deductible in calculating COP.(2) Recovery of sale of scrap deducted (3) Administration overhead related to factory forms part of cost of production. (4) Selling & distr. cost, abnormal and

SUMMARRY OF EXCISE CA MANOJ BATRA 14

non recurring cost, interest and financial charge not forms part of cost of production. (4) quality control, R& D, packing cost, amortised cost of moulds included in Cost of Production.

E/N- 67/95- Intermediate product exempt if capitvely consumed to manufacture in same factory and Final product is dutiable.

QUE- ABC Limited is engaged in the manufacture of Product ‘X’ for the purpose of captive consumption Determine the assessable value of Product ‘X:-. Direct Wages &Salaries 19,500 Consumbale stores and repairs 5,700 Research and Development Costs 3,800 Direct Material (including excise duty of `1800) 35,000 Administrative overheads (relating to production activities) 5,300 Selling and Distribution Costs 1,500 Realisable Value of Scrap 1,300 Amortised cost of fixtures2,500 Answer- Cost of production - 68,700, Assessable Value (` 68,700 x 110%) -75,570

Rule 9 - if sale to Related person AV= NTV at which related person sells to non-related If Related person doesn’t sale but captively consume, AV= 110% of cost of production

Universal luggage Mfg. Co - sales to both related and unrelated & charged same price from both AV for related person=price at which sold to NRP.

An assessee sold certain goods to PQR Company limited for Rs 22472( INCLUDING Duty 12.36%) on 09-09-2009. The buyer Is related person as defined u/s 4(3)(b) of the CEA 1944. The buyer did not sale the goods but used it as intermediary product. The cost of production of the goods was Rs. 16000. What should be the assessable value? What should be the assessable value if the goods were sold to unrelated person for Rs. 20000, who also used it as intermediary product? You may assume that the price charged from the buyer is excluding excise duty and other taxes Ans Case-1 value shall be 110% of 16000 i.e 17000. Case- 2 Rs. 20000 assessable value (22472 – 2472)

Rule 10 - ICU- also related under 4(3)(b)(ii)/(iii)/(iv)/H/S then as per rule 9, OTHERWISE- TRANSACTION VALUE U/S 4(1)(A)

Cool Drinks Ltd. manufactured three health drinks viz. A, B and C. A was sold only to M Ltd., a subsidiary company of Cool Drinks Ltd. B was sold to N Ltd., where the Managing Director of Cool Drinks Ltd. was a manager. C was sold to O Ltd. who was the sole distributor of Cool Drinks Ltd. and was coming under the management of Cool Drinks Ltd. [All transactions are between ICU] Determine the transaction value of the three products in the hands of Cool Drinks Ltd. on the basis of the following information: Price of Cool Drinks Ltd. to M Ltd. Rs. 200 Price of Cool Drinks Ltd. to N Ltd. Rs. 150 Price of Cool Drinks Ltd. to O Ltd. Rs. 120 Price of M Ltd. to Consumer Rs. 220 Price of N Ltd. to Consumer Rs. 160 Price of O Ltd. to Consumer Rs. 130 Ans-- Product A - Rs. 220/- , Product B -150 only, Product C -120

Rule 11

- Best judgement valuation- using reasonable means consistent with general provision of these rules and sec 4(1)

1) ICWA FINAL JUNE 2004

SUMMARRY OF EXCISE CA MANOJ BATRA 15

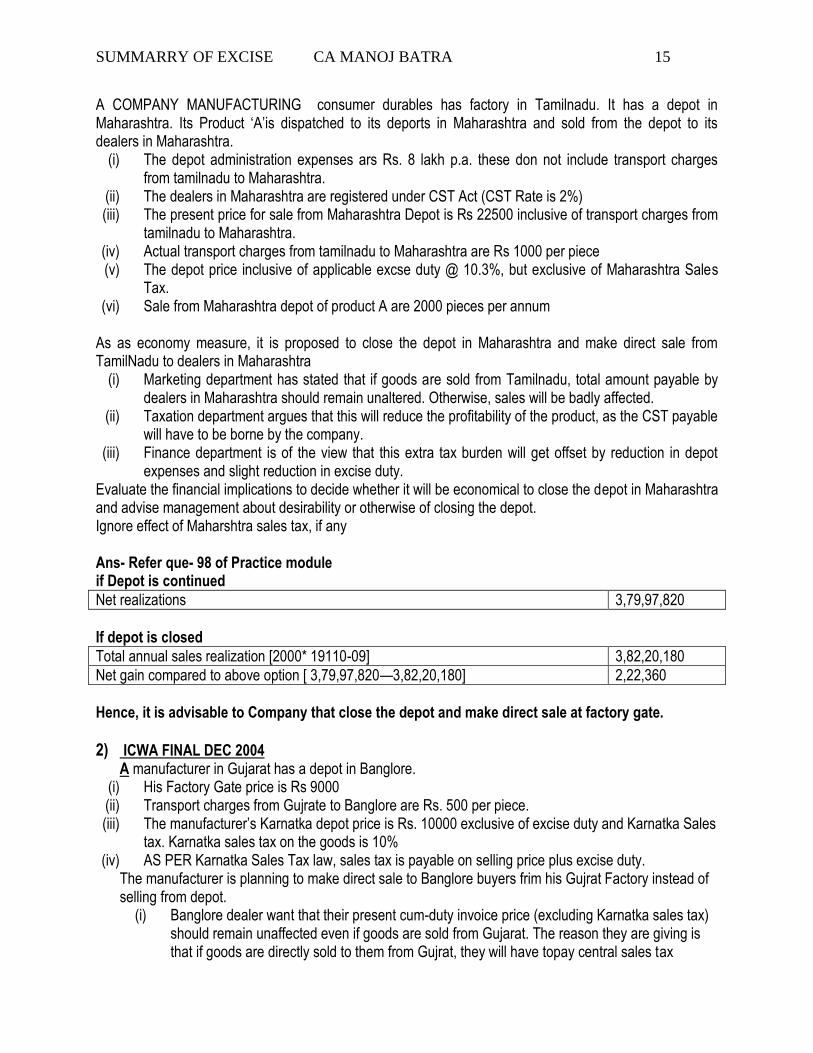

A COMPANY MANUFACTURING consumer durables has factory in Tamilnadu. It has a depot in Maharashtra. Its Product ‘A’is dispatched to its deports in Maharashtra and sold from the depot to its dealers in Maharashtra.

(i) The depot administration expenses ars Rs. 8 lakh p.a. these don not include transport charges from tamilnadu to Maharashtra.

(ii) The dealers in Maharashtra are registered under CST Act (CST Rate is 2%) (iii) The present price for sale from Maharashtra Depot is Rs 22500 inclusive of transport charges from

tamilnadu to Maharashtra. (iv) Actual transport charges from tamilnadu to Maharashtra are Rs 1000 per piece (v) The depot price inclusive of applicable excse duty @ 10.3%, but exclusive of Maharashtra Sales

Tax. (vi) Sale from Maharashtra depot of product A are 2000 pieces per annum

As as economy measure, it is proposed to close the depot in Maharashtra and make direct sale from TamilNadu to dealers in Maharashtra

(i) Marketing department has stated that if goods are sold from Tamilnadu, total amount payable by dealers in Maharashtra should remain unaltered. Otherwise, sales will be badly affected.

(ii) Taxation department argues that this will reduce the profitability of the product, as the CST payable will have to be borne by the company.

(iii) Finance department is of the view that this extra tax burden will get offset by reduction in depot expenses and slight reduction in excise duty.

Evaluate the financial implications to decide whether it will be economical to close the depot in Maharashtra and advise management about desirability or otherwise of closing the depot. Ignore effect of Maharshtra sales tax, if any Ans- Refer que- 98 of Practice module if Depot is continued

Net realizations 3,79,97,820

If depot is closed

Total annual sales realization [2000* 19110-09] 3,82,20,180

Net gain compared to above option [ 3,79,97,820—3,82,20,180] 2,22,360

Hence, it is advisable to Company that close the depot and make direct sale at factory gate.

2) ICWA FINAL DEC 2004 A manufacturer in Gujarat has a depot in Banglore.

(i) His Factory Gate price is Rs 9000 (ii) Transport charges from Gujrate to Banglore are Rs. 500 per piece. (iii) The manufacturer’s Karnatka depot price is Rs. 10000 exclusive of excise duty and Karnatka Sales

tax. Karnatka sales tax on the goods is 10% (iv) AS PER Karnatka Sales Tax law, sales tax is payable on selling price plus excise duty.

The manufacturer is planning to make direct sale to Banglore buyers frim his Gujrat Factory instead of selling from depot.

(i) Banglore dealer want that their present cum-duty invoice price (excluding Karnatka sales tax) should remain unaffected even if goods are sold from Gujarat. The reason they are giving is that if goods are directly sold to them from Gujrat, they will have topay central sales tax

SUMMARRY OF EXCISE CA MANOJ BATRA 16

(ii) The banglore dealer are registered under CST Act and CsT rate is 2% (iii) The manufacturer has agreed to the request of the dealers.

You are required to calculate the assessable value and excise duty and CST Payable if goods are sold directly from Gujrat assuming that dealer request is accepted. The product is leviable to excise duty @ 10% plus EC and SHEC as applicable. If the product is sold in gujrat state, the sales tax rate is 8% Ans- Refer que- 99 of Practice module

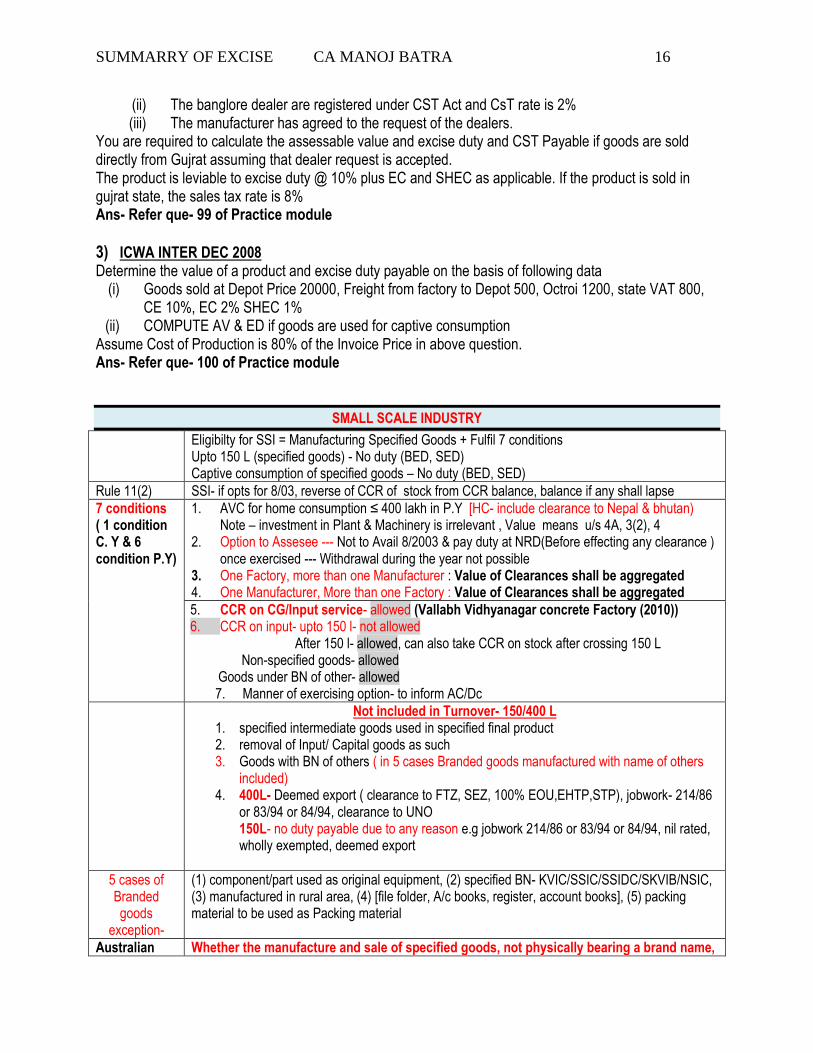

3) ICWA INTER DEC 2008 Determine the value of a product and excise duty payable on the basis of following data

(i) Goods sold at Depot Price 20000, Freight from factory to Depot 500, Octroi 1200, state VAT 800, CE 10%, EC 2% SHEC 1%

(ii) COMPUTE AV & ED if goods are used for captive consumption Assume Cost of Production is 80% of the Invoice Price in above question. Ans- Refer que- 100 of Practice module

SMALL SCALE INDUSTRY

Eligibilty for SSI = Manufacturing Specified Goods + Fulfil 7 conditions Upto 150 L (specified goods) - No duty (BED, SED) Captive consumption of specified goods – No duty (BED, SED)

Rule 11(2) SSI- if opts for 8/03, reverse of CCR of stock from CCR balance, balance if any shall lapse

7 conditions ( 1 condition C. Y & 6 condition P.Y)

1. AVC for home consumption ≤ 400 lakh in P.Y [HC- include clearance to Nepal & bhutan) Note – investment in Plant & Machinery is irrelevant , Value means u/s 4A, 3(2), 4

2. Option to Assesee --- Not to Avail 8/2003 & pay duty at NRD(Before effecting any clearance ) once exercised --- Withdrawal during the year not possible

3. One Factory, more than one Manufacturer : Value of Clearances shall be aggregated 4. One Manufacturer, More than one Factory : Value of Clearances shall be aggregated

5. CCR on CG/Input service- allowed (Vallabh Vidhyanagar concrete Factory (2010)) 6. CCR on input- upto 150 l- not allowed After 150 l- allowed, can also take CCR on stock after crossing 150 L Non-specified goods- allowed Goods under BN of other- allowed

7. Manner of exercising option- to inform AC/Dc

Not included in Turnover- 150/400 L 1. specified intermediate goods used in specified final product 2. removal of Input/ Capital goods as such 3. Goods with BN of others ( in 5 cases Branded goods manufactured with name of others

included) 4. 400L- Deemed export ( clearance to FTZ, SEZ, 100% EOU,EHTP,STP), jobwork- 214/86

or 83/94 or 84/94, clearance to UNO 150L- no duty payable due to any reason e.g jobwork 214/86 or 83/94 or 84/94, nil rated, wholly exempted, deemed export

5 cases of Branded goods

exception-

(1) component/part used as original equipment, (2) specified BN- KVIC/SSIC/SSIDC/SKVIB/NSIC, (3) manufactured in rural area, (4) [file folder, A/c books, register, account books], (5) packing material to be used as Packing material

Australian Whether the manufacture and sale of specified goods, not physically bearing a brand name,

SUMMARRY OF EXCISE CA MANOJ BATRA 17

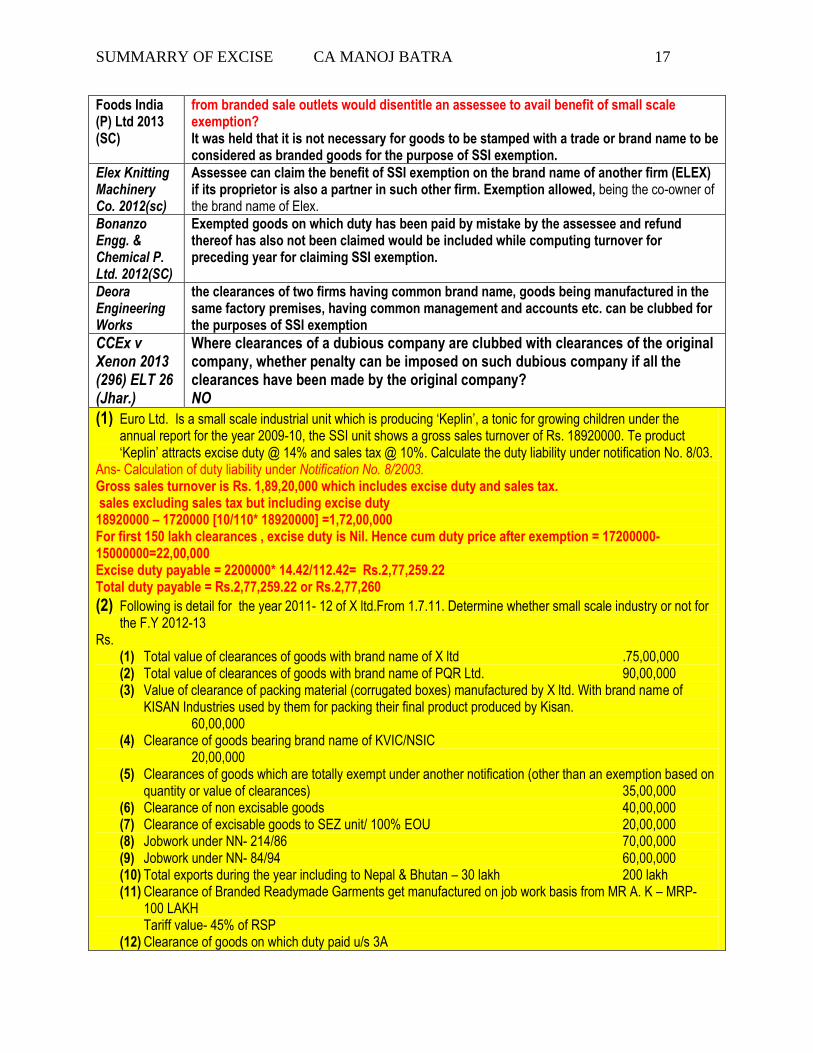

Foods India (P) Ltd 2013 (SC)

from branded sale outlets would disentitle an assessee to avail benefit of small scale exemption? It was held that it is not necessary for goods to be stamped with a trade or brand name to be considered as branded goods for the purpose of SSI exemption.

Elex Knitting Machinery Co. 2012(sc)

Assessee can claim the benefit of SSI exemption on the brand name of another firm (ELEX) if its proprietor is also a partner in such other firm. Exemption allowed, being the co-owner of the brand name of Elex.

Bonanzo Engg. & Chemical P. Ltd. 2012(SC)

Exempted goods on which duty has been paid by mistake by the assessee and refund thereof has also not been claimed would be included while computing turnover for preceding year for claiming SSI exemption.

Deora Engineering Works

the clearances of two firms having common brand name, goods being manufactured in the same factory premises, having common management and accounts etc. can be clubbed for the purposes of SSI exemption

CCEx v Xenon 2013 (296) ELT 26 (Jhar.)

Where clearances of a dubious company are clubbed with clearances of the original company, whether penalty can be imposed on such dubious company if all the clearances have been made by the original company? NO

(1) Euro Ltd. Is a small scale industrial unit which is producing ‘Keplin’, a tonic for growing children under the annual report for the year 2009-10, the SSI unit shows a gross sales turnover of Rs. 18920000. Te product ‘Keplin’ attracts excise duty @ 14% and sales tax @ 10%. Calculate the duty liability under notification No. 8/03.

Ans- Calculation of duty liability under Notification No. 8/2003. Gross sales turnover is Rs. 1,89,20,000 which includes excise duty and sales tax. sales excluding sales tax but including excise duty 18920000 – 1720000 [10/110* 18920000] =1,72,00,000 For first 150 lakh clearances , excise duty is Nil. Hence cum duty price after exemption = 17200000-15000000=22,00,000 Excise duty payable = 2200000* 14.42/112.42= Rs.2,77,259.22 Total duty payable = Rs.2,77,259.22 or Rs.2,77,260

(2) Following is detail for the year 2011- 12 of X ltd.From 1.7.11. Determine whether small scale industry or not for the F.Y 2012-13

Rs. (1) Total value of clearances of goods with brand name of X ltd .75,00,000 (2) Total value of clearances of goods with brand name of PQR Ltd. 90,00,000 (3) Value of clearance of packing material (corrugated boxes) manufactured by X ltd. With brand name of

KISAN Industries used by them for packing their final product produced by Kisan. 60,00,000

(4) Clearance of goods bearing brand name of KVIC/NSIC 20,00,000

(5) Clearances of goods which are totally exempt under another notification (other than an exemption based on quantity or value of clearances) 35,00,000

(6) Clearance of non excisable goods 40,00,000 (7) Clearance of excisable goods to SEZ unit/ 100% EOU 20,00,000 (8) Jobwork under NN- 214/86 70,00,000 (9) Jobwork under NN- 84/94 60,00,000 (10) Total exports during the year including to Nepal & Bhutan – 30 lakh 200 lakh (11) Clearance of Branded Readymade Garments get manufactured on job work basis from MR A. K – MRP-

100 LAKH Tariff value- 45% of RSP

(12) Clearance of goods on which duty paid u/s 3A

SUMMARRY OF EXCISE CA MANOJ BATRA 18

30,00,000 Before 1-7-09 the Factory was occupied by Previous Tenant M/s Raja and cleared goods of value of Rs. 15 lakh Ans- 75,00,000 + 60,00,000 + 20,00,000 + 35,00,000 + 30,00,000 + 45,00,000 + 30,00,000 + 15,00,000 =300 lakh The unit is small scale unit because total value of clearance doesn’t exceed 400 lakh.

1) MNO Ltd. is in the manufacture of both excisable and non-excisable goods in their factorybuilding rented by them from October 1, 2012 and have been occupying the same as a tenant.From the following particulars for the period October 1, 2012 to March 31, 2013, state brieflywith suitable explanations, whether MNO Ltd. could claim the benefit of exemption in terms ofNotification No. 8/2003-CE dated 1-3-2003 for the financial year 2013-14.

` (in lakhs)

(i) Clearances of branded goods 60

(ii) Export Sales to Nepal 80

(iii) Export Sales to USA and Canada 120

(iv) Clearances of goods (duty paid based on Annual capacity of production under section 3A of the Central Excise Act, 1944)

70

(v) Clearances of goods subject to valuation based on retail sale price under section 4A of the Central Excise Act, 1944(said goods are eligible for 30% abatement)

200

(vi) Job work under Notification No. 214/86-CE dated 25-3-86 60

During the period April 1, 2012 to Sept 30, 2012 the previous tenant of the building presentlyoccupied by MNO Ltd. had cleared excisable goods of the aggregate value of` 120 lakhs. ANS- 80 + 70 + 140 + 120 =410, HENCE NON SSI

2) Choti Ltd., which is engaged in the manufacture of excisable goods started its business in May, 2012. It availed small scale exemption in terms of Notification No. 8/2003-C.E. dated 1-3-2003 as amended for the financial year 2012-13. The following details are provided:

` 15,000 kg of inputs purchased @ ` 992.70 per kg 1,48,90,500 (inclusive of Central excise duty @ 12.36%) Capital goods purchased on 28-6-2012 44,12,000 (inclusive of excise duty at 12.36%) Finished goods sold (at uniform transaction 2,50,00,000 value throughout the year) Calculate the amount of excise duty payable by M/s. Choti Ltd. in cash, if any, during the year 2012-13. Rate of duty on finished goods sold may be taken at 12.36% for the year and you may assume that the selling price is exclusive of central excise duty. There is neither any processing loss nor any inventory of input and output. Show your workings and notes with suitable assumptions as required. ANS – EXCISE DUTY PAYABLE IN CASH – 95,461

3) X Ltd. is having a manufacturing unit at Faridabad. In the financial year 2012-13, the value of

total clearances from the unit was ` 850 lakhs as per the following details:

(i) Exports to USA : ` 100 lakhs; to Nepal : ` 50 Lakhs

(ii) Clearances to a 100% export oriented unit : ` 75 lakhs

(iii) Clearances as loan licensee of goods carrying the brand name of another upon full payment of duty: `

200 lakhs

(iv) Clearance exempted vide Notification No. 214/86-C.E. dated 25.3.86: ` 125 lakhs.

(v) Balance clearances of goods in the normal course : ` 300 lakhs.

SUMMARRY OF EXCISE CA MANOJ BATRA 19

You are required to state with reasons whether the unit is entitled to the benefit of exemption under Notification No. 8/2003-C.E. dated 1.3.2003 as amended for the financial year 2013-14. ANS- 850 -100-75-200-125 = 350 LAKH, HENCE SSI

4) Que M/s Pappu ltd. A manufacturer of Papad and other goods provides the following details for the year ending 31st mar 2014 . Whether the company will be eligible for SSI exemption for 2014-15 (1) Clearance of finished goods covered u/s 4A – MRP- 200 lakh, Abatement- 30% (2) Value of clearance of input as such under rule 3(5) – 30 lakh (3) Value of clearance of excisable goods bearing brand name of foreign company which

assigned to Pappu of Rs. 70 lakh (4) Value of clearance of goods under brand name of oeher – 300 lakh (5) Clearance of waste and scrap under exemption – 40 lakh (6) Value of clearance of packing material under Brand name of other – 50 lakh (7) Clearance of other excisable goods – 60 lakh

Ans- (200 – 60) i.e 140 L + 70 L +40 + 50 L + 60 L = 360 lakh Hence the unit is eligible for SSI exemption. Audit

SPECIAL AUDIT

14A 14AA

BASIS Valuation Audit CCR Audit

PRIOR APPROVAL By Chief CCE not required

NOMINATION OF CA/CWA

By Chief CCE By CCE

TIME LIMIT FOR AUDIT REPORT

Original + extended = 180 days No time limit

AUDIT FEES PAID BY WHOM

Department Department

SCN Show cause notice issued on basis of audit report

Show cause notice issued on basis of audit report

EA 2000

EA 2000 is transparent,interactive and systematic form of audit where selection of assesses is based on the track record of the assesses. And the areas where the revenue leakage can be , is determined before conducting the audit.

Amt of duty Frequency of audit

Above Rs 3 Crore once in every year

Between Rs 1 crore AND Rs. 3 Crore Once in 2 years

Between Rs. 50 lakh and Rs 1 Crore Once in 5 years

Less than Rs. 50 Lakh 10% of units in every year Procedure of EA 2000

1) selection of assesse - Selection of the unit is based taking into account the 'risk-factors'. Risk factors under Excise Audit, 2000 means that the assessees who have a bad track record are taken up for audit on priority as opposed to those who enjoy a clean track record. For example: (i) assessee having past duty

SUMMARRY OF EXCISE CA MANOJ BATRA 20

evasion cases, (ii) late payment of duty/late filling returns, (iii) major audit objections against them , (iv) no cash payment of duty (all CENVAT adjustment) (v) past duty dues, etc

2) desk review - the auditor is required to be sufficiently prepared before the visit to the unit Perusal ofassessee’s profile, annual report, trial balance, cost audit report and income-tax audit report is involved in desk review.

1) documenting information 2) touring 3) audit plan 4) verification 5) audit para 6) audit report

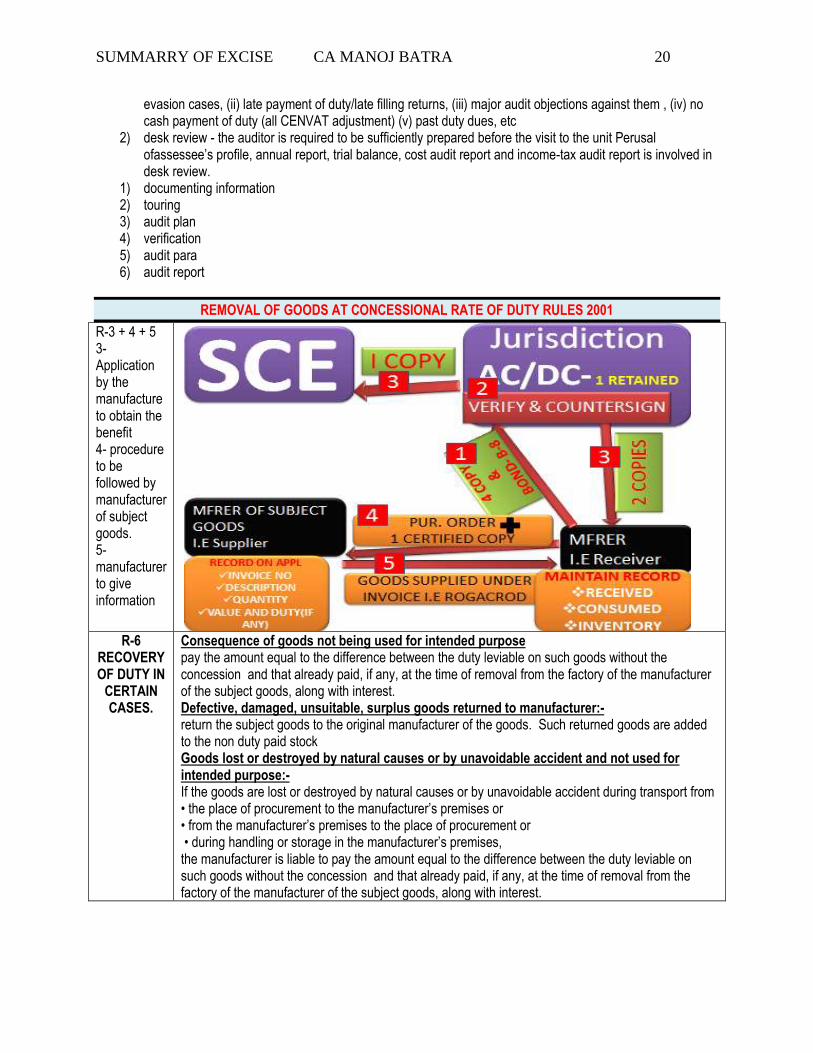

REMOVAL OF GOODS AT CONCESSIONAL RATE OF DUTY RULES 2001

R-3 + 4 + 5 3- Application by the manufacture to obtain the benefit 4- procedure to be followed by manufacturer of subject goods. 5- manufacturer to give information

R-6

RECOVERY OF DUTY IN

CERTAIN CASES.

Consequence of goods not being used for intended purpose pay the amount equal to the difference between the duty leviable on such goods without the concession and that already paid, if any, at the time of removal from the factory of the manufacturer of the subject goods, along with interest. Defective, damaged, unsuitable, surplus goods returned to manufacturer:- return the subject goods to the original manufacturer of the goods. Such returned goods are added to the non duty paid stock Goods lost or destroyed by natural causes or by unavoidable accident and not used for intended purpose:- If the goods are lost or destroyed by natural causes or by unavoidable accident during transport from • the place of procurement to the manufacturer’s premises or • from the manufacturer’s premises to the place of procurement or • during handling or storage in the manufacturer’s premises, the manufacturer is liable to pay the amount equal to the difference between the duty leviable on such goods without the concession and that already paid, if any, at the time of removal from the factory of the manufacturer of the subject goods, along with interest.