dr shah april 2006

TRANSCRIPT

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 1/48

PRESENTATION ON

The Present Economic Outlookfor Pakistan

By

Ministry of Finance

Government of Pakistan

April, 2006

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 2/48

2

Outline of Presentation

Key Macroeconomic Challenges of the 1990s

How did we address those challenges

Where Are We Now?

Where do we want to see Pakistan in the next five years

Key Macroeconomic targets for the next five years

New Challenges

How to address new challenges

Concluding remarks

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 3/48

3

Overcoming macroeconomic challenges

• 1990s Macroeconomic Scenario – Macroeconomic imbalances leading to buildup of public debt,

deceleration of growth and investment, and stagnation in exports• Challenges of the 90s

– Improve macroeconomic environment

– Bring debt situation under control – Restore investor confidence – Revive economic growth – Restore financial sovereignty

• 2000-onwards: Two-pronged Strategy followed – Policies pursued to strengthen macroeconomic environment – Introducing wide-ranging structural reforms

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 4/48

4

Policies pursued to strengthen macroeconomicenvironment

•

Reducing “Twin Deficits”• Keeping inflation low• Building foreign exchange reserves• Maintaining stability in exchange rate•

Maintaining consistency and continuity in policies

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 5/48

5

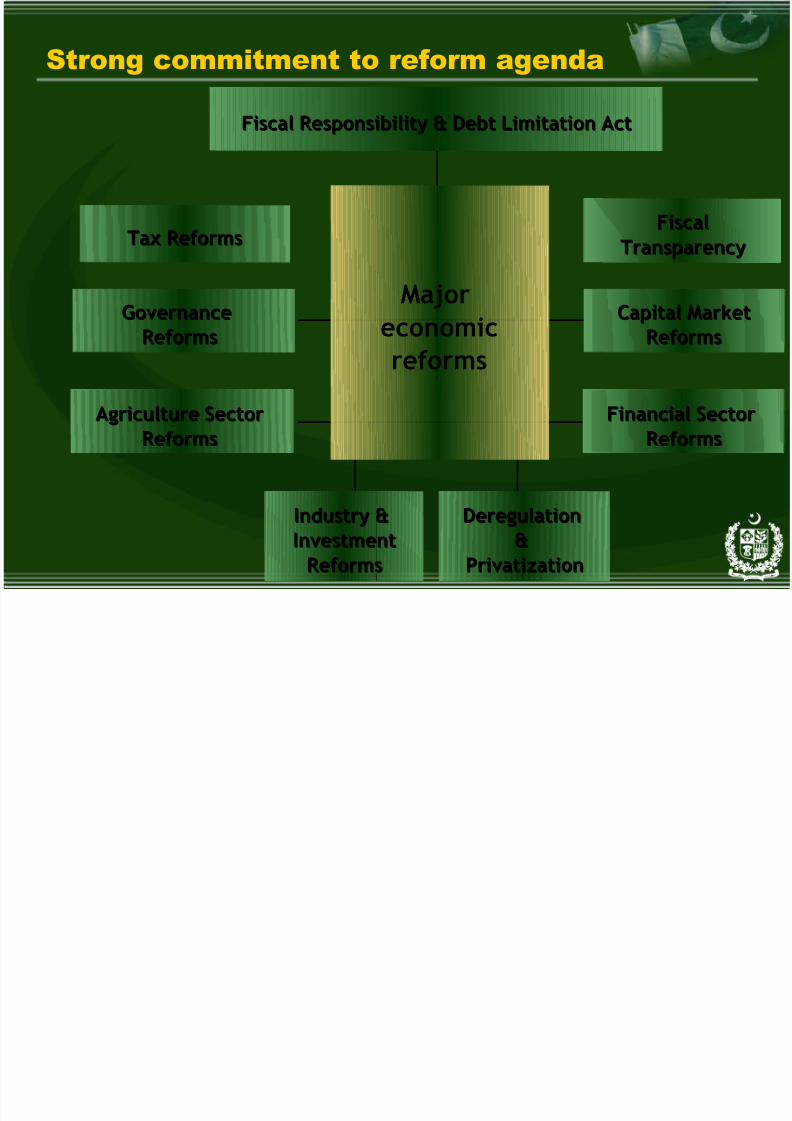

Strong commitment to reform agenda

Majoreconomicreforms

Tax ReformsTax Reforms

GovernanceGovernanceReformsReforms

Capital MarketCapital MarketReformsReforms

Industry &Industry &InvestmentInvestment

ReformsReforms

FiscalFiscalTransparencyTransparency

Agriculture SectorAgriculture SectorReformsReforms

Financial SectorFinancial SectorReformsReforms

DeregulationDeregulation&&

PrivatizationPrivatization

Fiscal Responsibility & Debt Limitation ActFiscal Responsibility & Debt Limitation Act

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 6/48

6

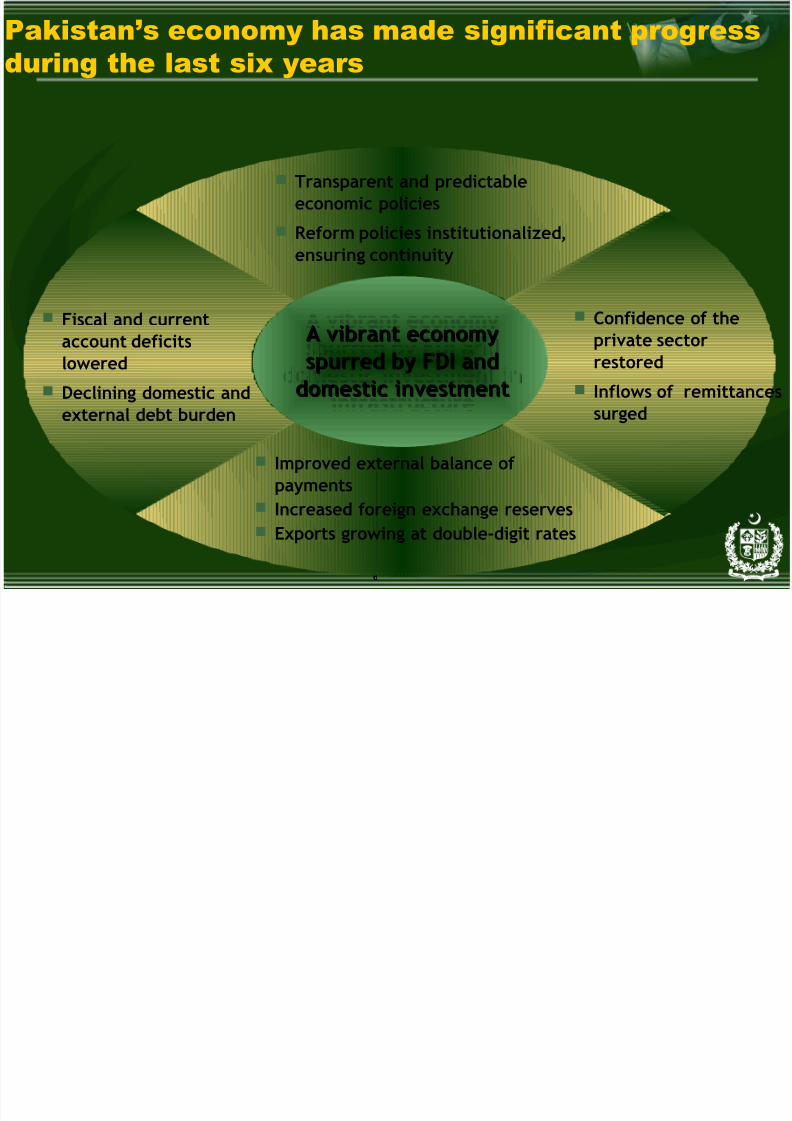

Improved external balance of paymentsIncreased foreign exchange reservesExports growing at double-digit rates

Pakistan’s economy has made significant progressduring the last six years

A vibrant economyA vibrant economyspurred by FDI andspurred by FDI and

domestic investment indomestic investment in

infrastructureinfrastructure

Transparent and predictableeconomic policies

Reform policies institutionalized,ensuring continuity

Confidence of theprivate sectorrestored

Inflows of remittances

surged

Fiscal and currentaccount deficitslowered

Declining domestic and

external debt burden

A vibrant economyA vibrant economyspurred by FDI andspurred by FDI and

domestic investmentdomestic investment

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 7/48

Where Are We Now ?

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 8/488

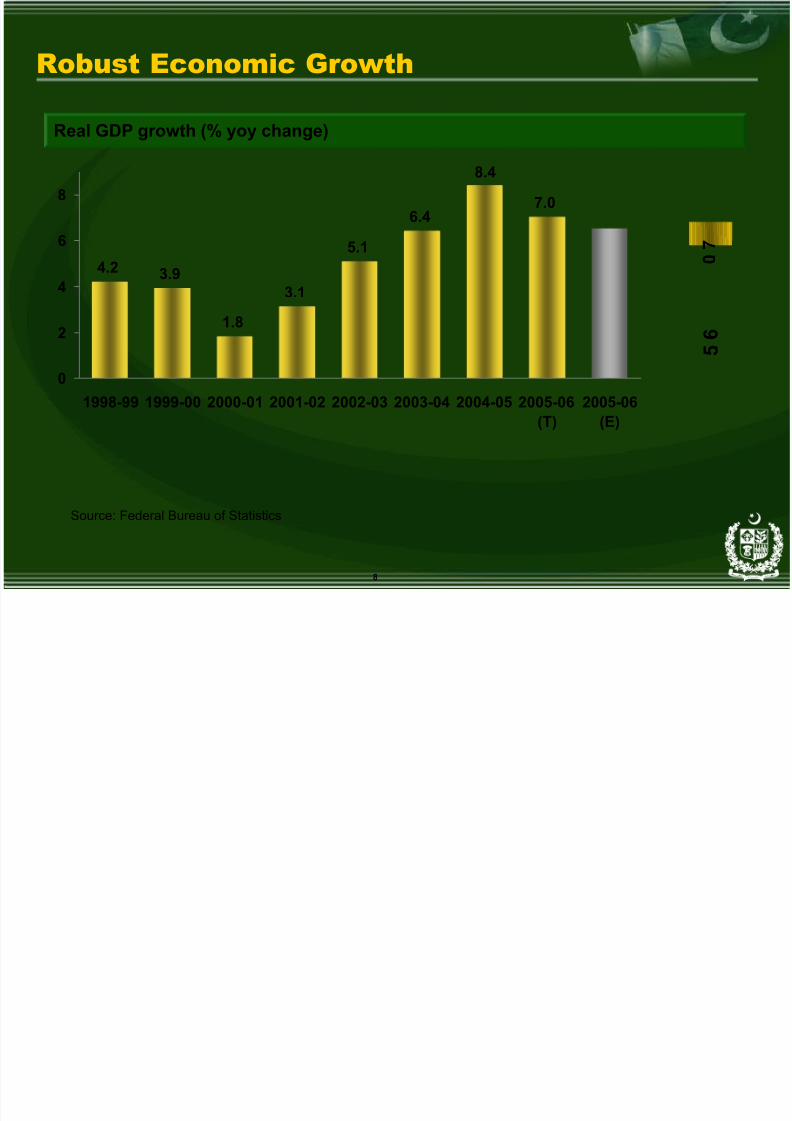

Robust Economic Growth

Real GDP growth (% yoy change)

4.23.9

1.8

3.1

5.1

6.47.0

8.4

0

2

4

6

8

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06(T)

2005-06(E)

Source: Federal Bureau of Statistics

6 . 5

7 . 0

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 9/489

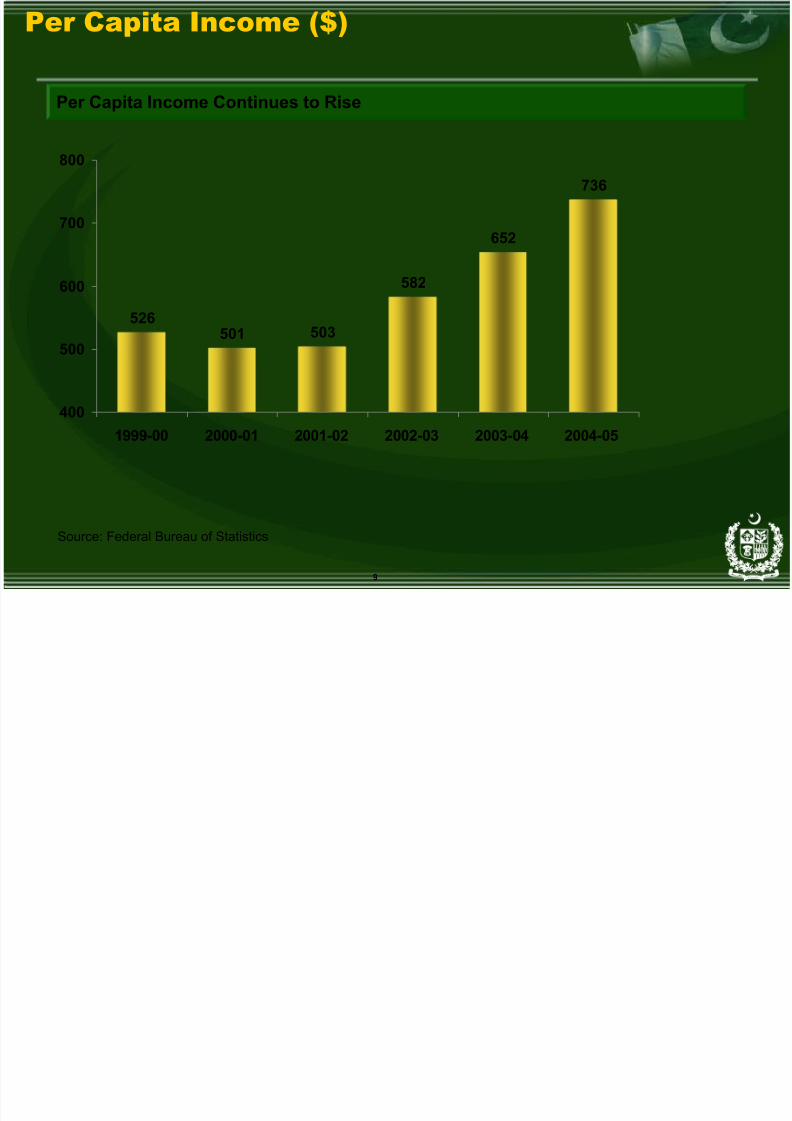

Per Capita Income ($)

526501 503

582

652

736

400

500

600

700

800

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05

Per Capita Income Continues to Rise

Source: Federal Bureau of Statistics

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 10/4810

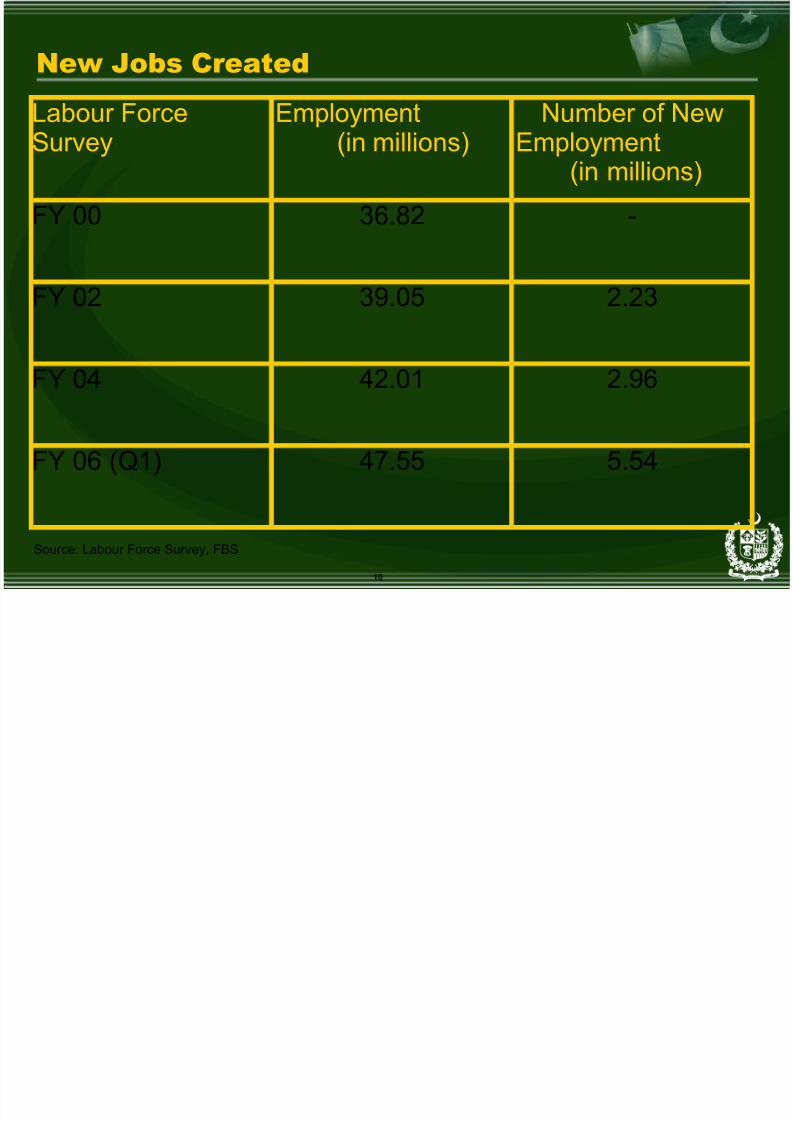

New Jobs Created

Labour ForceSurvey

Employment(in millions)

Number of NewEmployment

(in millions)

FY 00 36.82 -

FY 02 39.05 2.23

FY 04 42.01 2.96

FY 06 (Q1) 47.55 5.54

Source: Labour Force Survey, FBS

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 11/4811

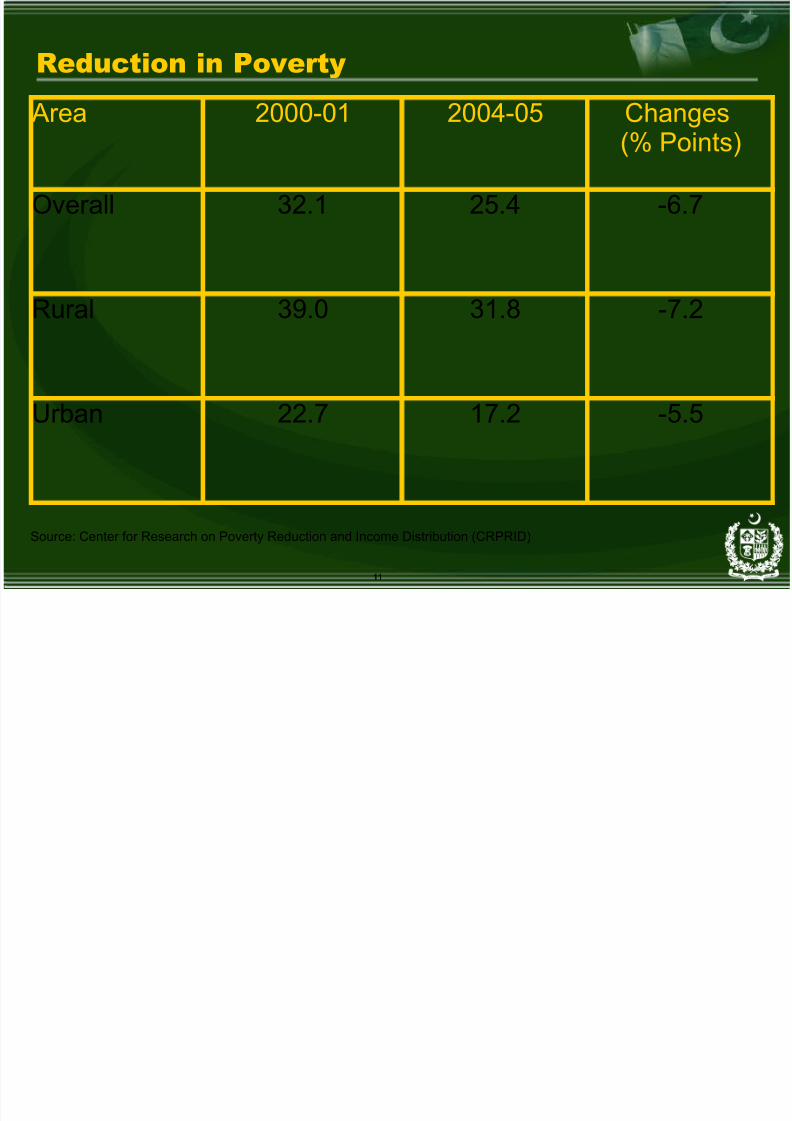

Reduction in Poverty

Area 2000-01 2004-05 Changes(% Points)

Overall 32.1 25.4 -6.7

Rural 39.0 31.8 -7.2

Urban 22.7 17.2 -5.5

Source: Center for Research on Poverty Reduction and Income Distribution (CRPRID)

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 12/4812

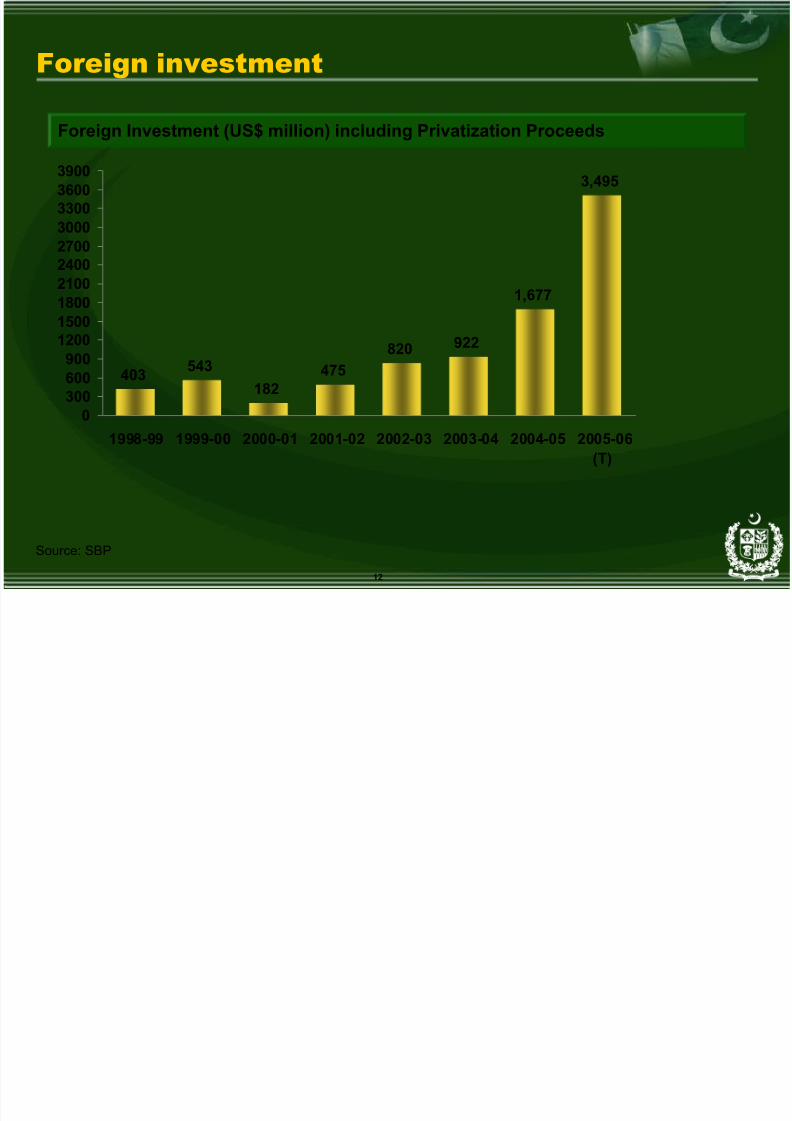

Foreign investment

Foreign Investment (US$ million) including Privatization Proceeds

Source: SBP

403 543182

475820 922

1,677

3,495

0

300600900

1200150018002100240027003000330036003900

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06(T)

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 13/4813

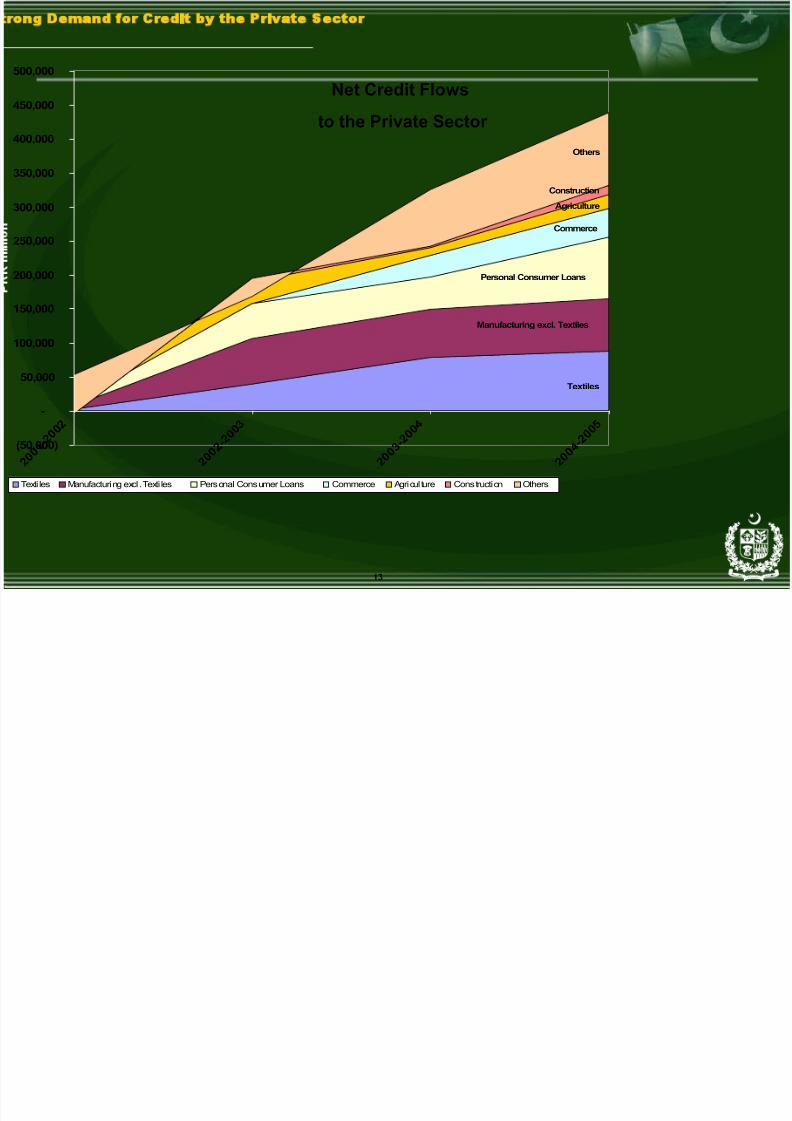

rong Demand for Credit by the Private Sector

Textiles

Manufacturing excl. Textiles

Personal Consumer Loans

Commerce

Agriculture

Construction

Others

(50,000)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2 0 0 1

- 2 0 0 2

2 0 0 2

- 2 0 0 3

2 0 0 3

- 2 0 0 4

2 0 0 4

- 2 0 0 5

Texti les Manufacturing excl . Texti les Personal Consumer Loans Commerce Agricul ture Construction Others

Net Credit Flows

to the Private Sector

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 14/4814

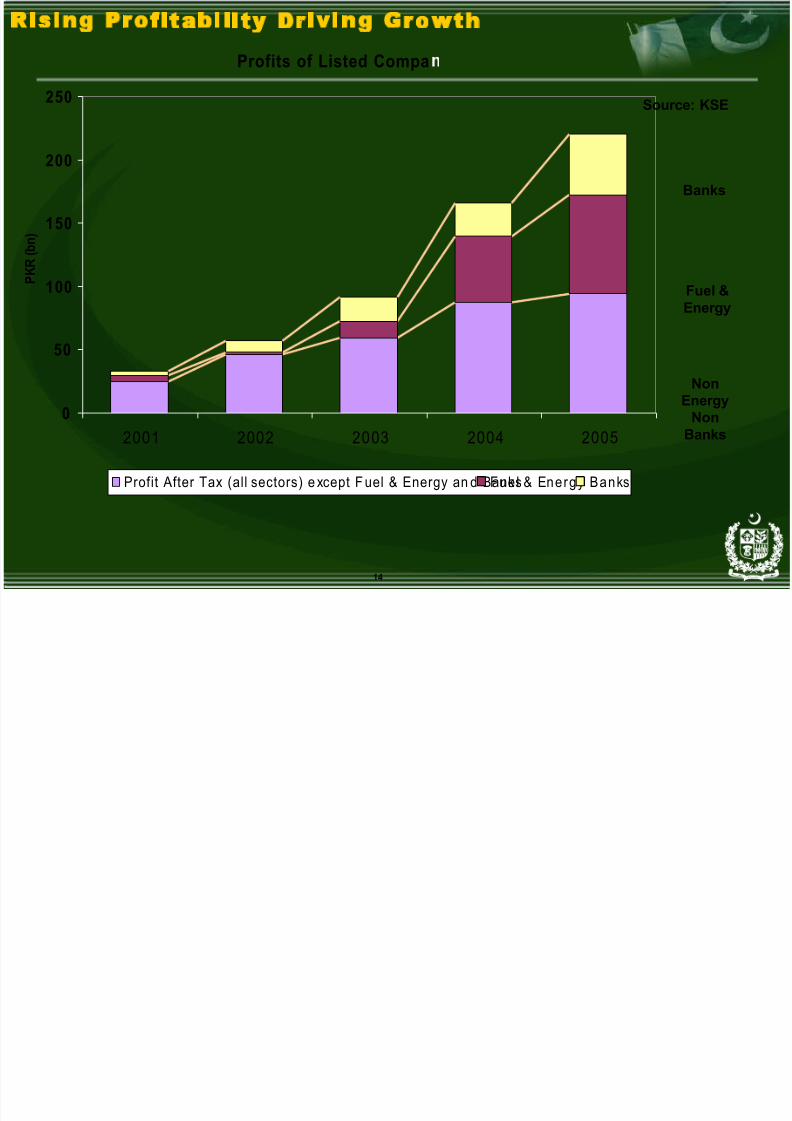

Profits of Listed Compa

0

50

100

150

200

250

2001 2002 2003 2004 2005

P K R ( b n )

Profit After Tax (all sectors) e xcept F uel & Energy an d BanksFuel & Energy Banks

Banks

Fuel &Energy

NonEnergy

NonBanks

Rising Profitability Driving Growth

Source: KSE

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 15/4815

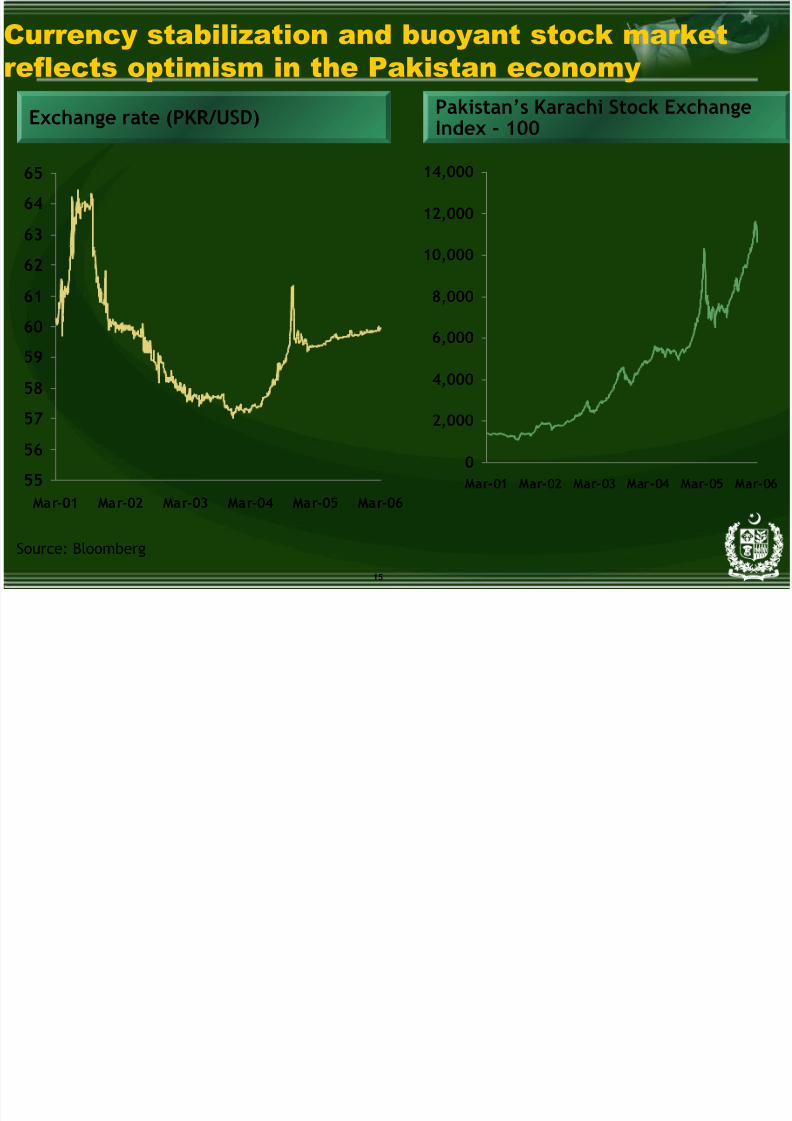

Currency stabilization and buoyant stock marketreflects optimism in the Pakistan economy

Source: Bloomberg

Exchange rate (PKR/USD) Pakistan’s Karachi Stock ExchangeIndex - 100

55

56

57

58

59

60

61

62

63

64

65

Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 16/4816

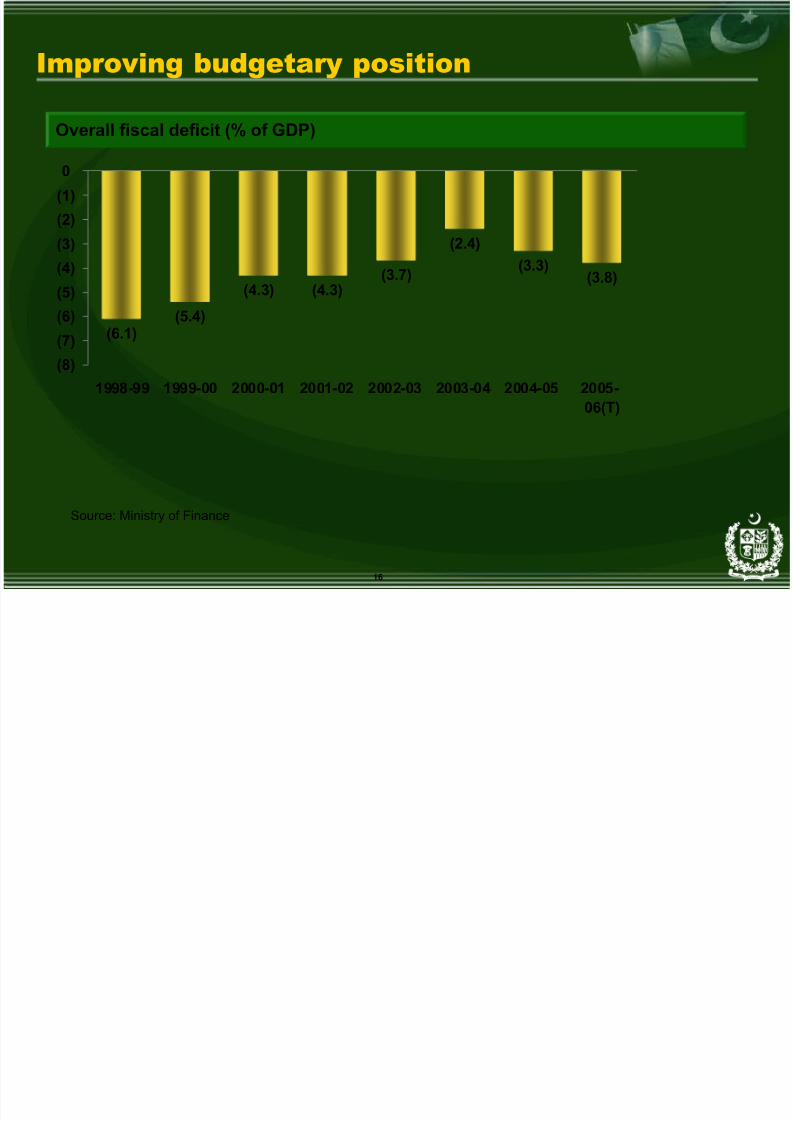

Improving budgetary position

Overall fiscal deficit (% of GDP)

Source: Ministry of Finance

(6.1)(5.4)

(4.3) (4.3) (3.7)

(2.4)(3.3)

(3.8)

(8)

(7)

(6)

(5)

(4)

(3)

(2)

(1)

0

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06(T)

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 17/4817

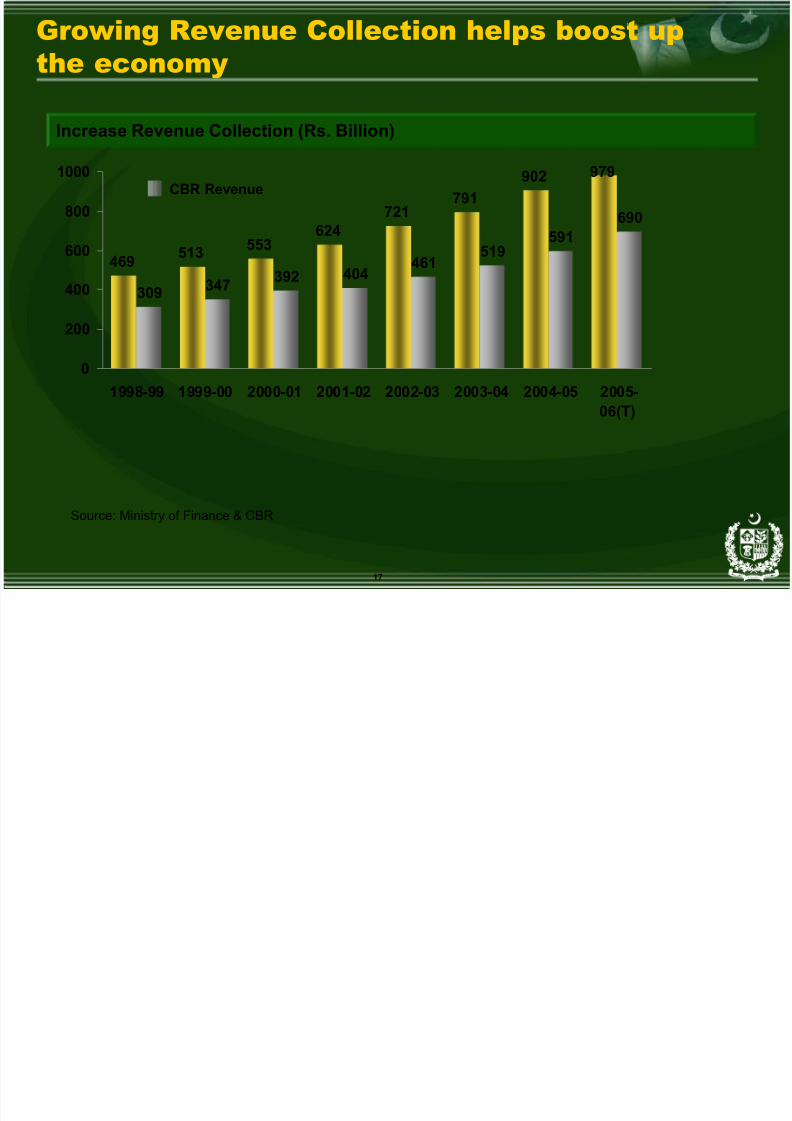

Growing Revenue Collection helps boost upthe economy

Increase Revenue Collection (Rs. Billion)

469 513 553624

721791

902 979

309 347 392 404461

519591

690

0

200

400

600

800

1000

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-

06(T)

Source: Ministry of Finance & CBR

CBR Revenue

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 18/4818

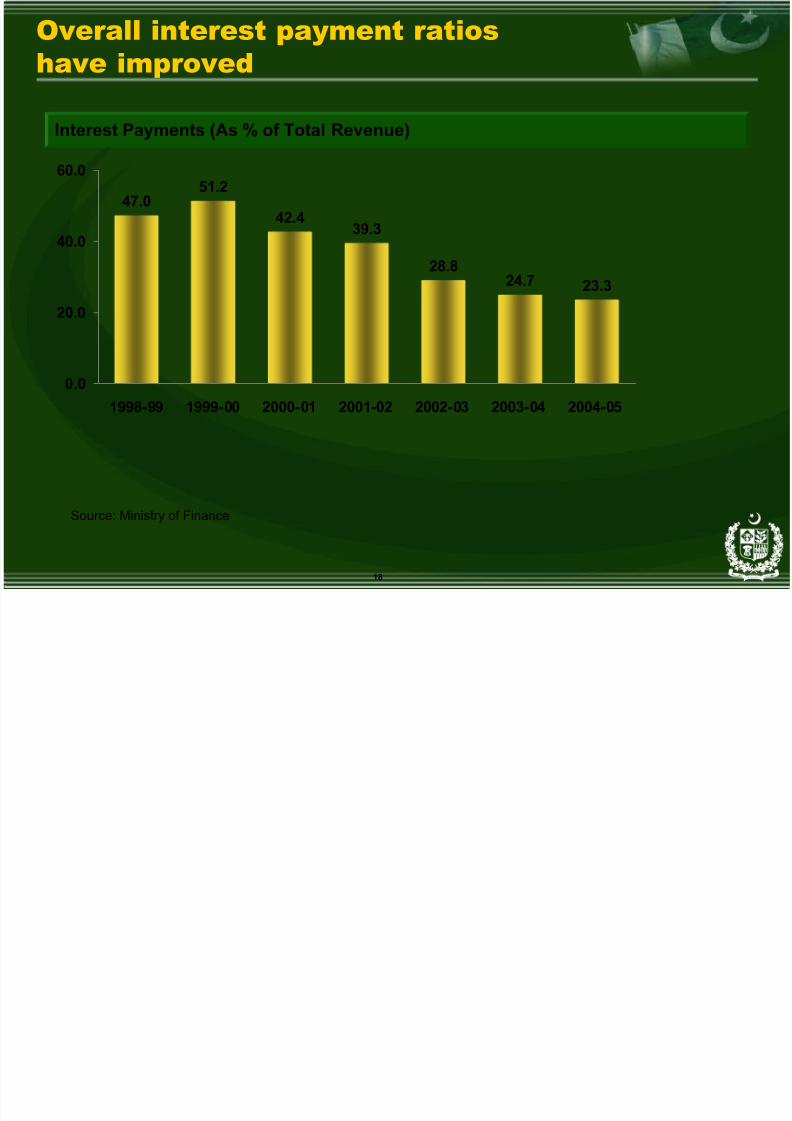

Overall interest payment ratioshave improved

Interest Payments (As % of Total Revenue)

Source: Ministry of Finance

47.051.2

42.439.3

28.824.7 23.3

0.0

20.0

40.0

60.0

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 19/4819

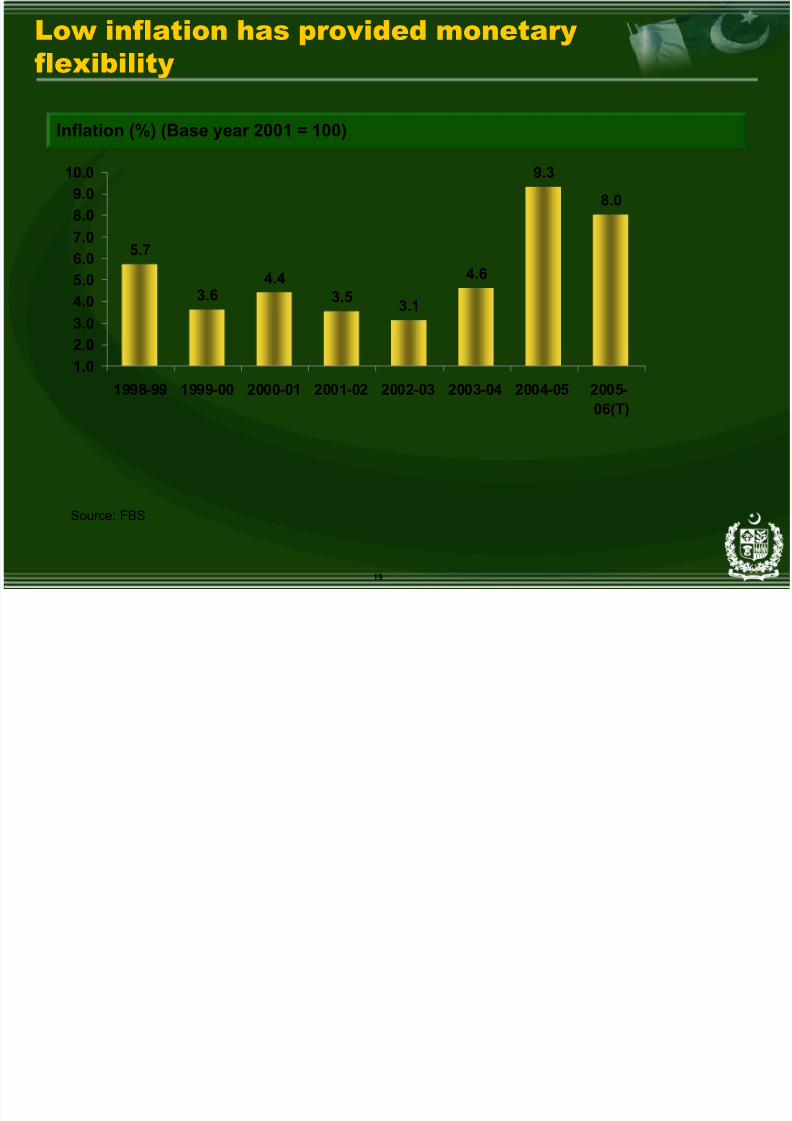

Low inflation has provided monetaryflexibility

Source: FBS

Inflation (%) (Base year 2001 = 100)

5.7

3.64.4

3.5 3.14.6

9.3

8.0

1.02.03.04.05.0

6.07.08.09.0

10.0

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-

06(T)

8/8/2019 Dr Shah April 2006

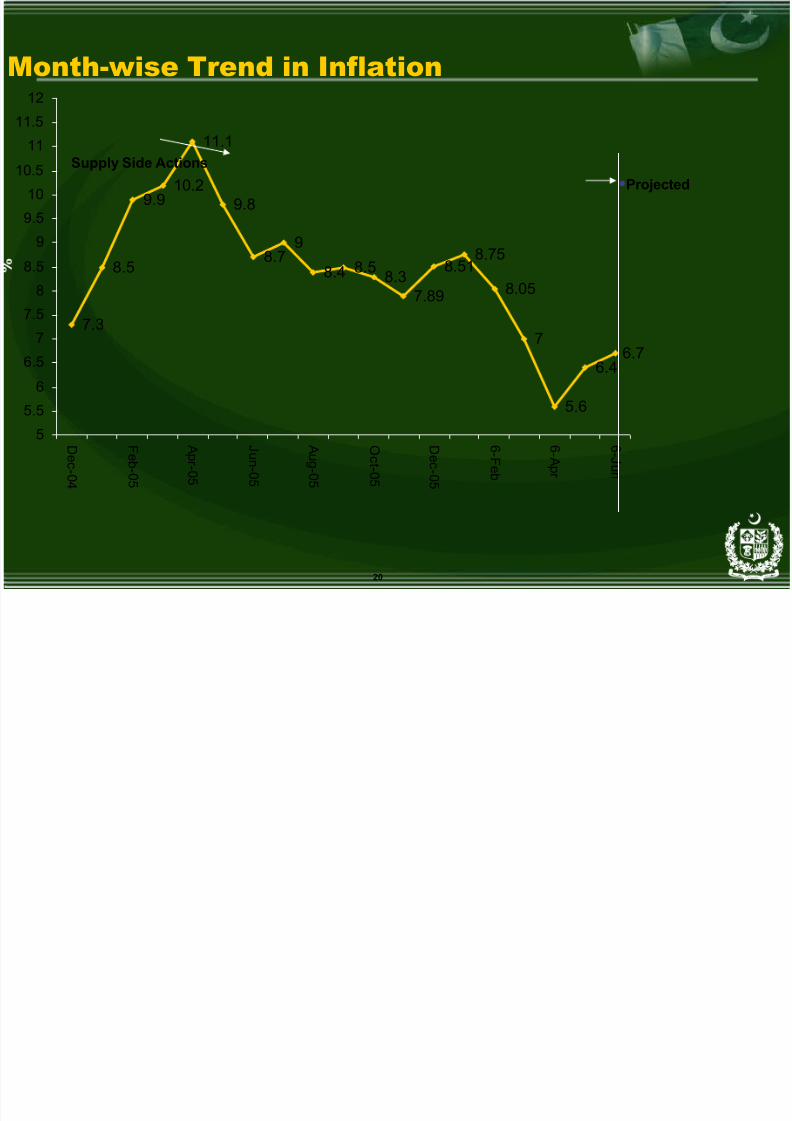

http://slidepdf.com/reader/full/dr-shah-april-2006 20/48

20

7.3

8.5

9.910.2

11.1

9.8

8.79

8.48.5

8.37.89

8.518.75

8.05

7

5.6

6.46.7

55.5

6

6.5

7

7.5

8

8.5

9

9.5

10

10.5

11

11.5

12

D e c - 0 4

F e b - 0 5

A pr - 0 5

J un- 0 5

A u g- 0 5

O c t - 0 5

D e c - 0 5

6 -F e b

6 -A

pr

6 - J un

Month-wise Trend in Inflation

Supply Side Actions

•Projected

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 21/48

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 22/48

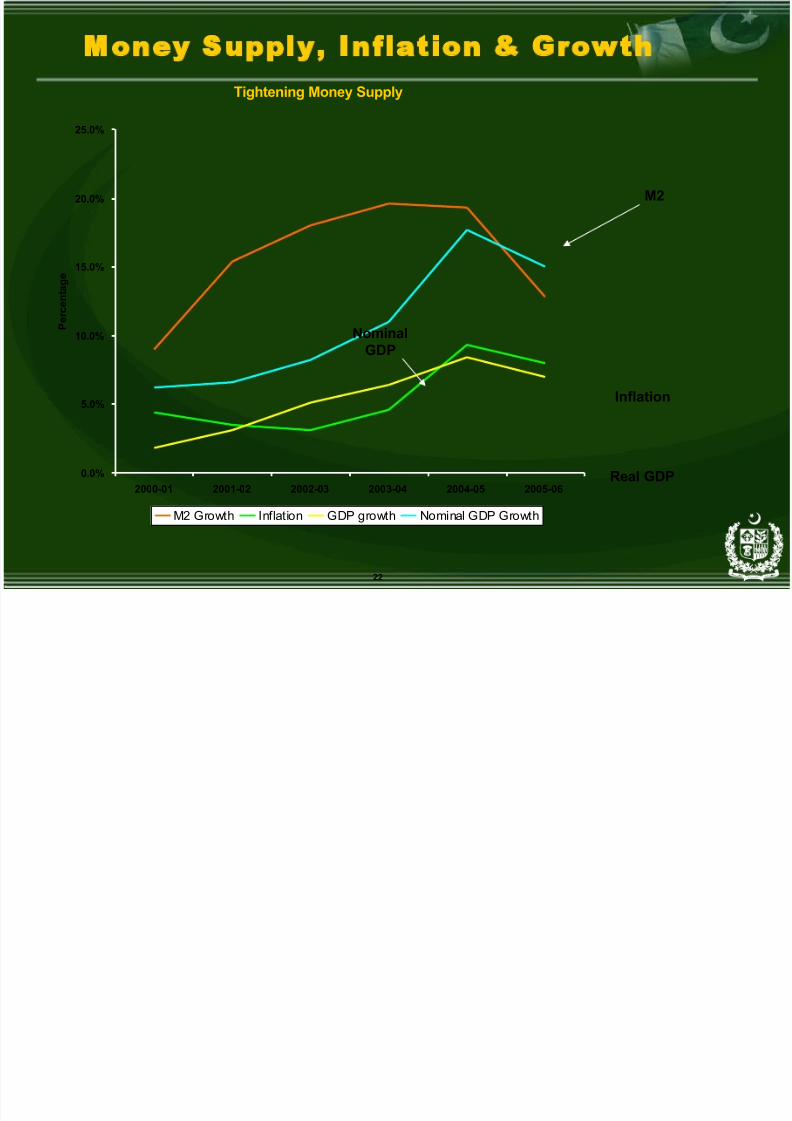

22

Money Supply, Inflation & GrowthTightening Money Supply

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

P e r c e n t a g e

M2 Growth Inflation GDP growth Nominal GDP Growth

M2

NominalGDP

Inflation

Real GDP

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 23/48

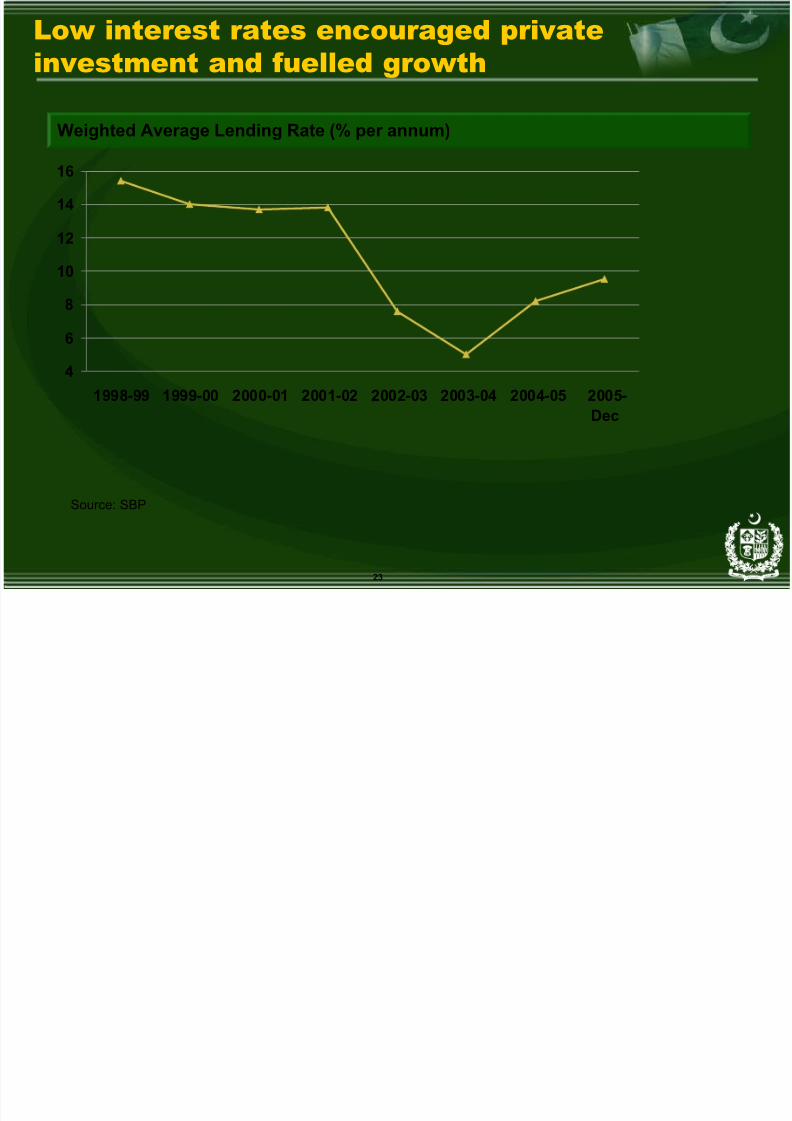

23

Low interest rates encouraged privateinvestment and fuelled growth

Weighted Average Lending Rate (% per annum)

Source: SBP

4

6

810

12

14

16

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-

Dec

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 24/48

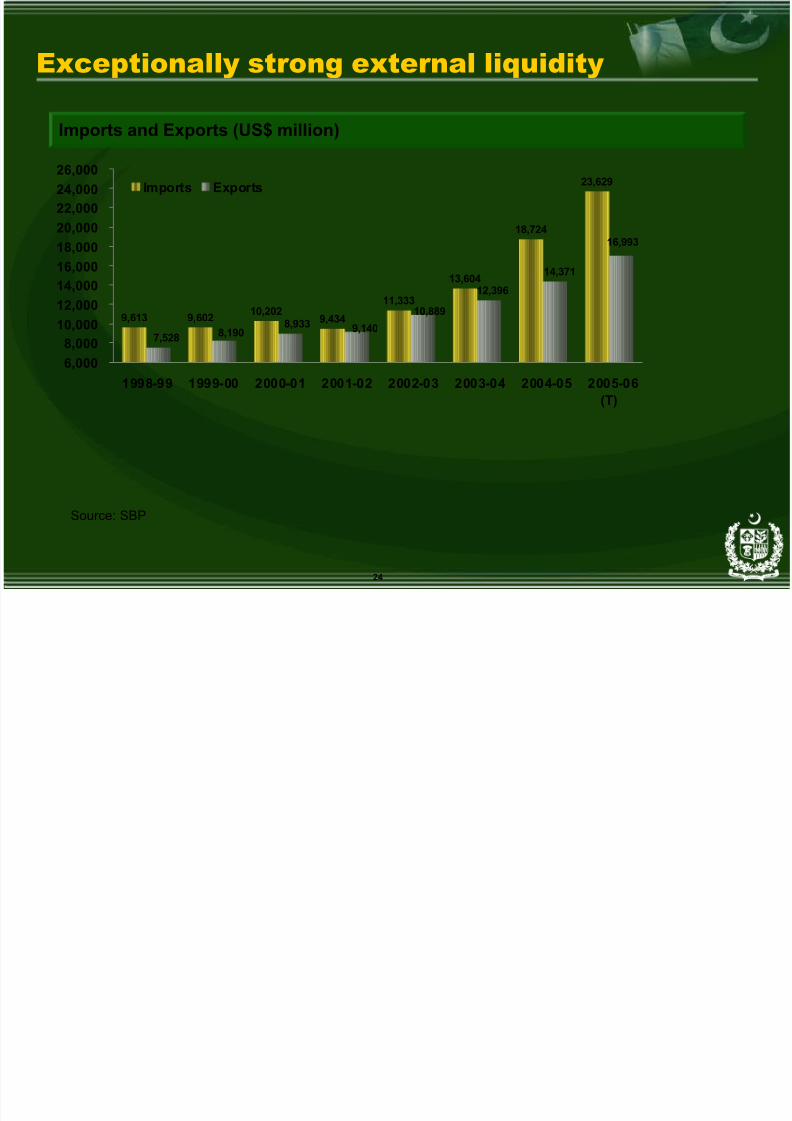

24

Exceptionally strong external liquidity

Source: SBP

Imports and Exports (US$ million)

9,613 9,602 10,2029,434

11,333

13,604

18,724

23,629

14,371

16,993

8,9338,1907,528

12,396

10,889

9,140

6,0008,000

10,00012,00014,00016,00018,00020,00022,00024,00026,000

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06(T)

Imports Exports

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 25/48

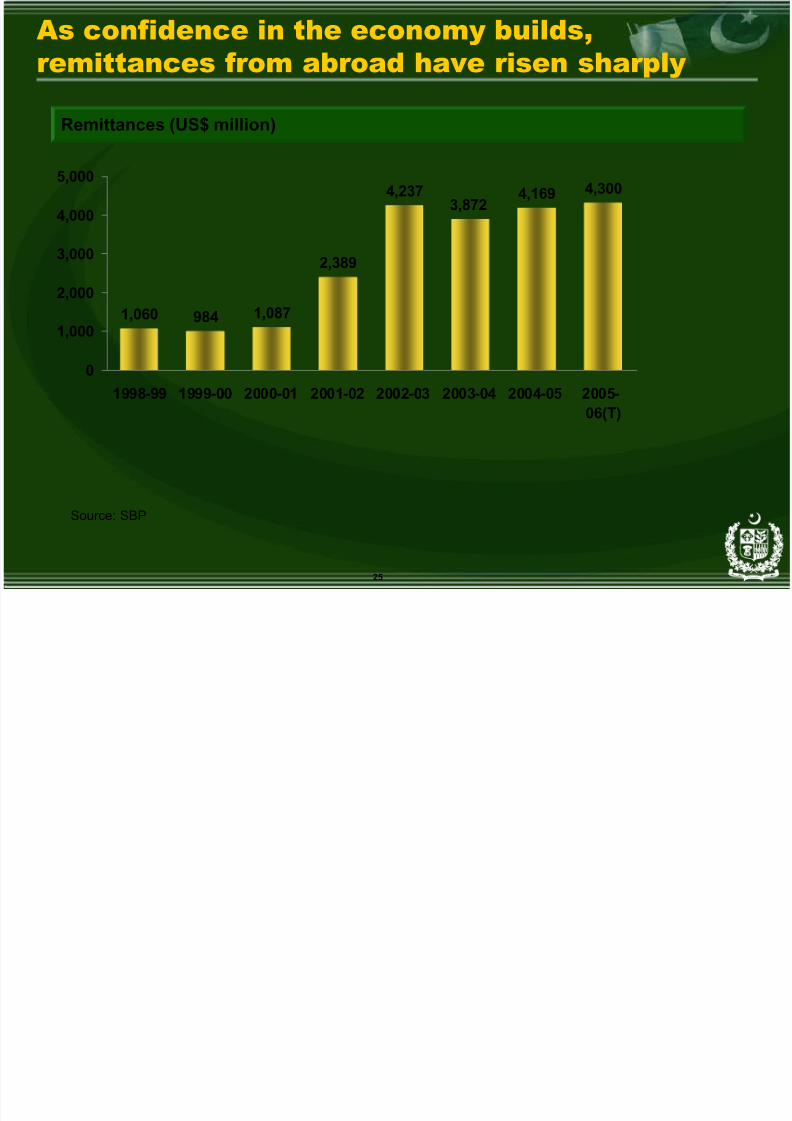

25

As confidence in the economy builds,remittances from abroad have risen sharply

Source: SBP

Remittances (US$ million)

1,060 984 1,087

2,389

4,2373,872

4,169 4,300

0

1,000

2,000

3,000

4,000

5,000

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-

06(T)

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 26/48

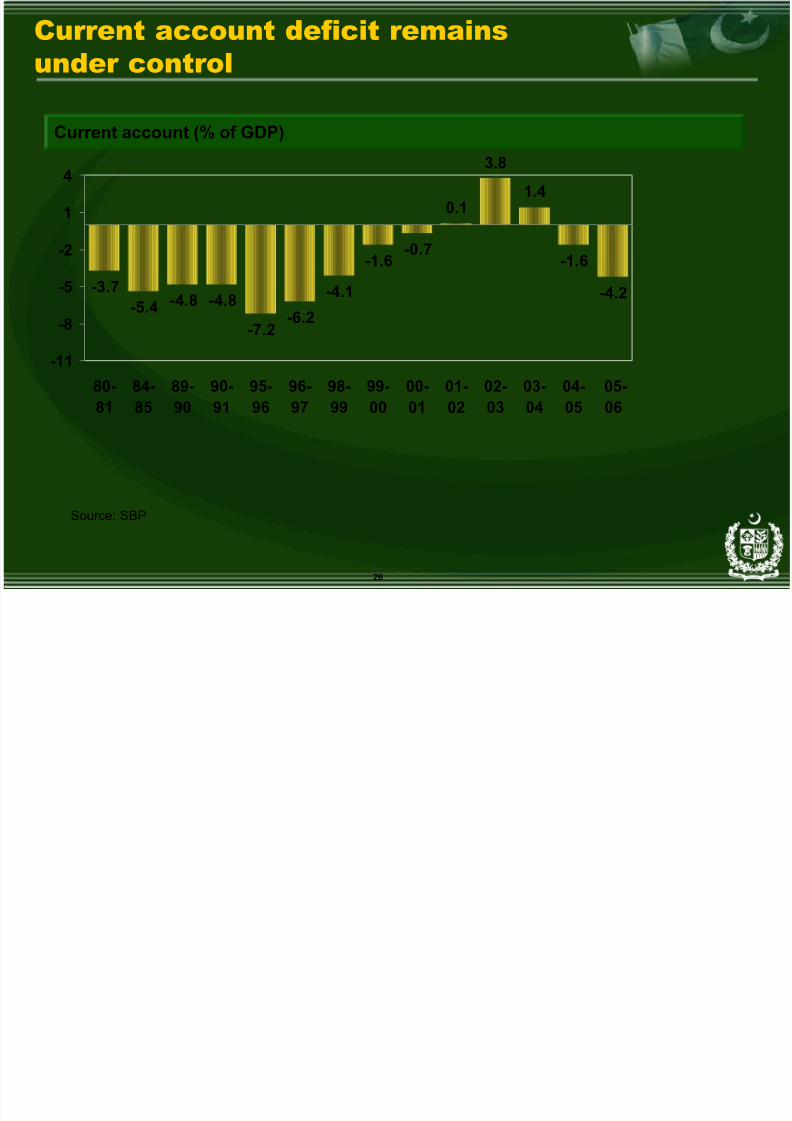

26

Current account (% of GDP)

Current account deficit remainsunder control

-3.7-5.4 -4.8 -4.8

-7.2-6.2

-4.1

-1.6-0.7

0.1

3.8

1.4

-1.6

-4.2

-11

-8

-5

-2

1

4

80-81

84-85

89-90

90-91

95-96

96-97

98-99

99-00

00-01

01-02

02-03

03-04

04-05

05-06

Source: SBP

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 27/48

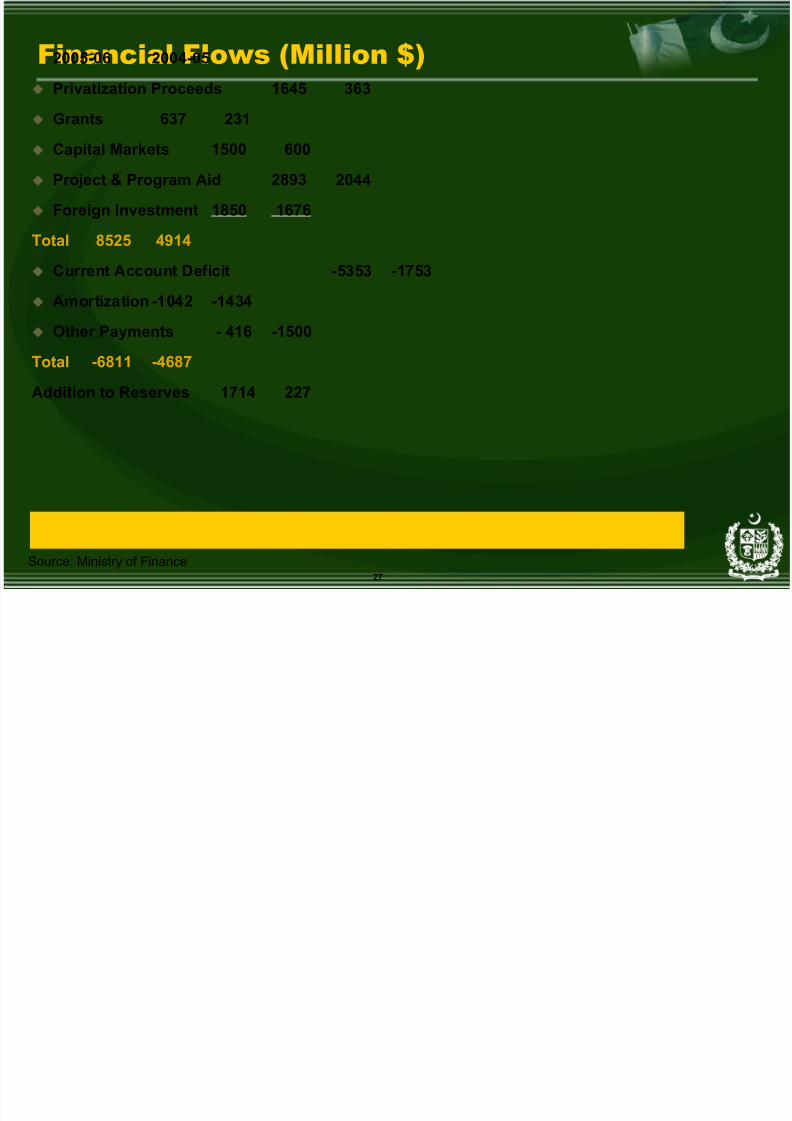

27

Financial Flows (Million $)2005-06 2004-05

Privatization Proceeds 1645 363

Grants 637 231

Capital Markets 1500 600

Project & Program Aid 2893 2044

Foreign Investment 1850 1676

Total 8525 4914

Current Account Deficit -5353 -1753

Amortization -1042 -1434

Other Payments - 416 -1500

Total -6811 -4687

Addition to Reserves 1714 227

Source: Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 28/48

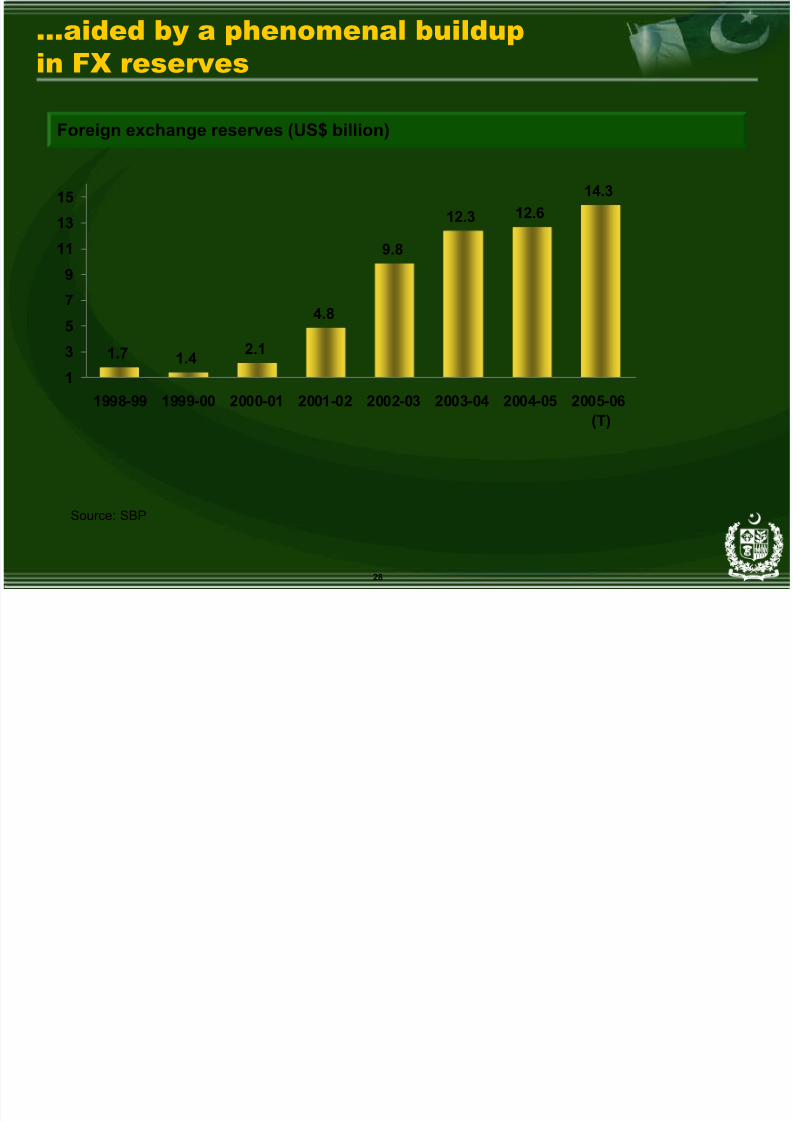

28

...aided by a phenomenal buildupin FX reserves

Source: SBP

Foreign exchange reserves (US$ billion)

1.7 1.42.1

4.8

9.8

12.3 12.614.3

1

3

5

79

11

13

15

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

(T)

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 29/48

Debt Profile of Pakistan

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 30/48

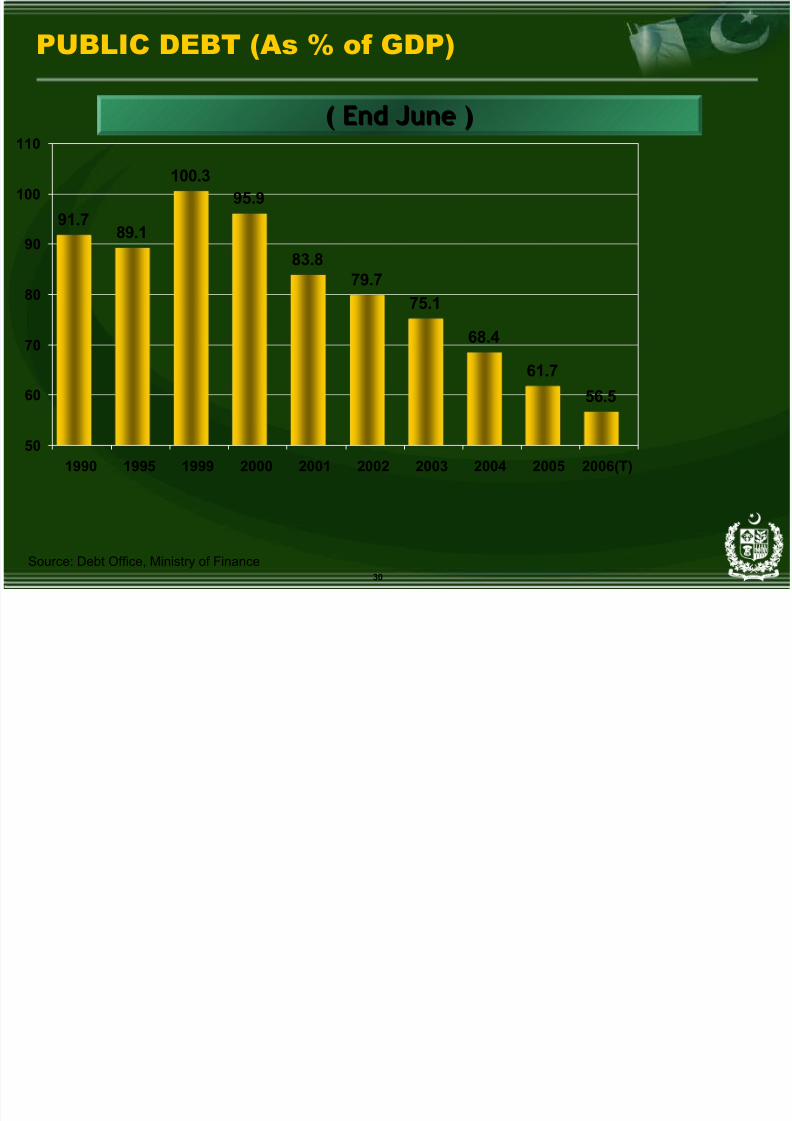

30

PUBLIC DEBT (As % of GDP)

91.789.1

100.3

56.5

61.7

68.4

75.179.7

83.8

95.9

50

60

70

80

90

100

110

1990 1995 1999 2000 2001 2002 2003 2004 2005 2006(T)

( End June )( End June )

Source: Debt Office, Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 31/48

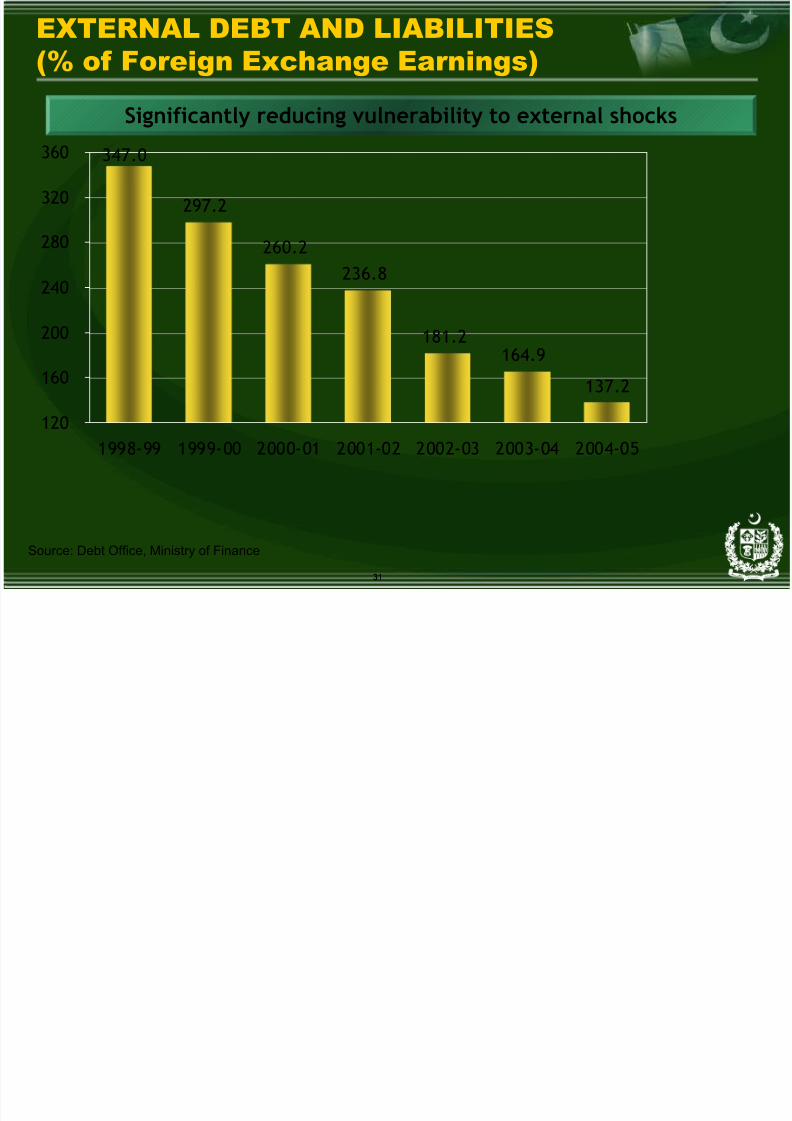

31

EXTERNAL DEBT AND LIABILITIES(% of Foreign Exchange Earnings)

297.2

260.2

236.8

181.2164.9

137.2

347.0

120

160

200

240

280

320

360

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05

Significantly reducing vulnerability to external shocks

Source: Debt Office, Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 32/48

32

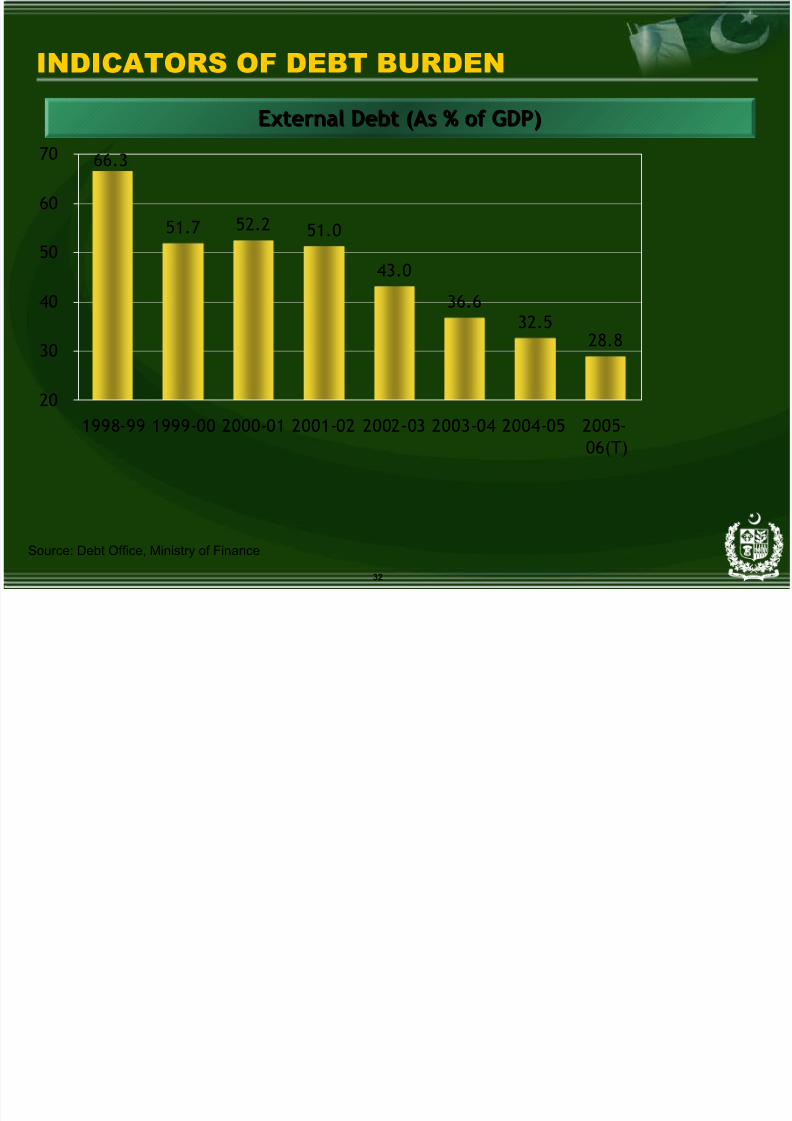

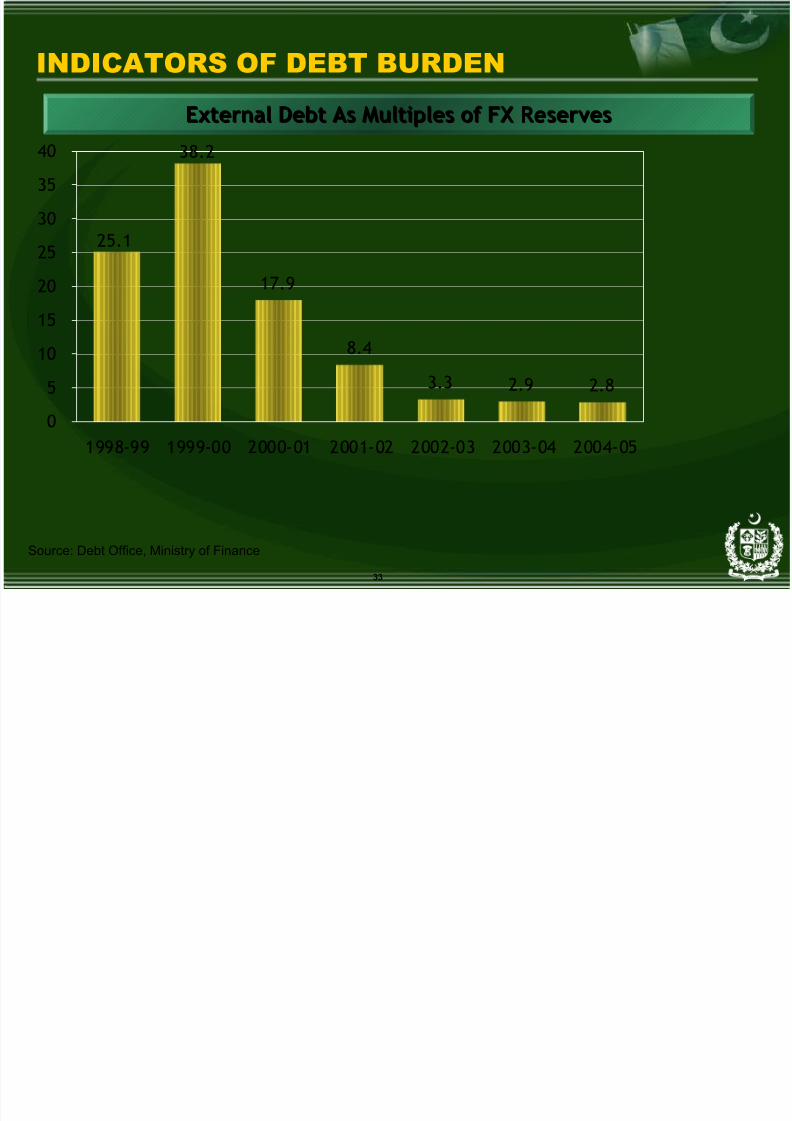

INDICATORS OF DEBT BURDEN

51.7 52.2 51.0

43.0

36.632.5

28.8

66.3

20

30

40

50

60

70

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06(T)

External Debt (As % of GDP)External Debt (As % of GDP)

Source: Debt Office, Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 33/48

33

INDICATORS OF DEBT BURDEN

38.2

17.9

8.4

3.3 2.9 2.8

25.1

0

5

10

15

20

25

30

35

40

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05

External Debt As Multiples of FX ReservesExternal Debt As Multiples of FX Reserves

Source: Debt Office, Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 34/48

Pakistan’s EconomyIn the Next Five Years

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 35/48

35

Pakistan’s Economy in the Next Five Years

Strong Economic Growth Ranging between 6 – 8% p.a.

Stable Macroeconomic Environment

Debt Burden Reaching Sustainable Level

Lives of the Common Man ImprovingSocial Indicators Improving

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 36/48

Key Macroeconomic TargetsFor The Next Five Years

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 37/48

37

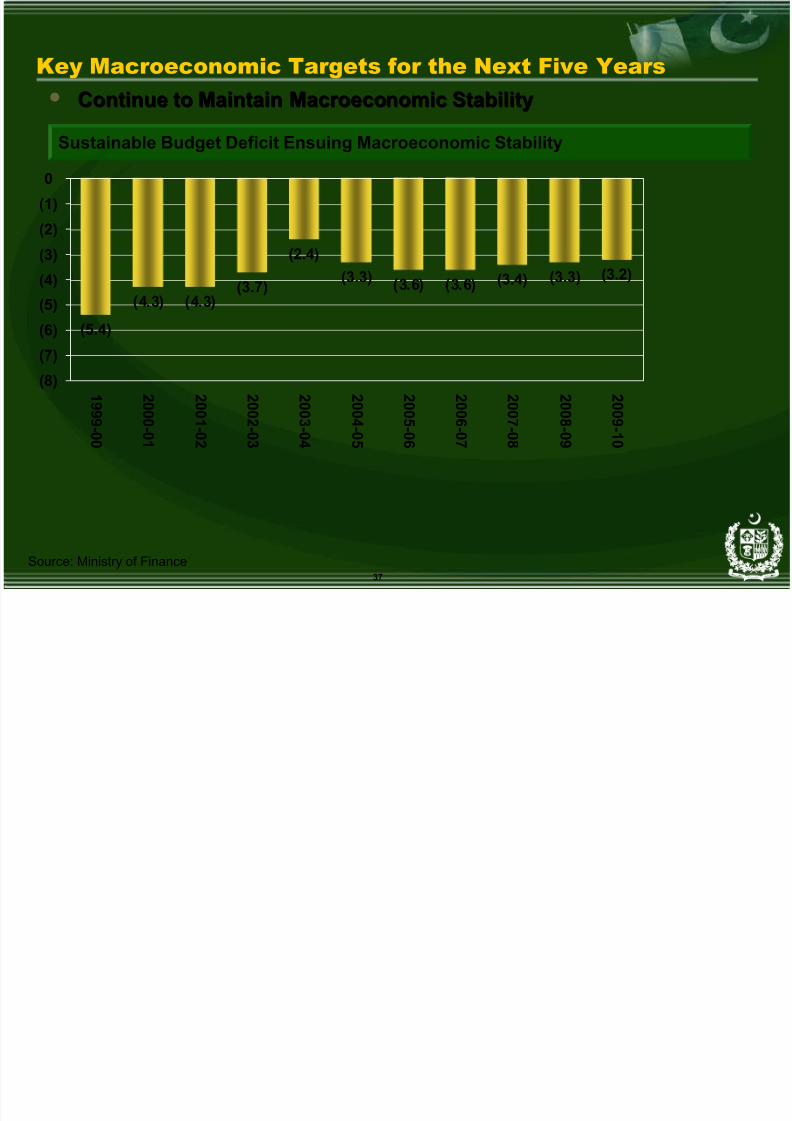

Key Macroeconomic Targets for the Next Five Years

Sustainable Budget Deficit Ensuing Macroeconomic Stability

• Continue to Maintain Macroeconomic StabilityContinue to Maintain Macroeconomic Stability

(5.4)

(4.3) (4.3)(3.7)

(2.4)

(3.3) (3.6) (3.6) (3.4) (3.3) (3.2)

(8)

(7)

(6)

(5)(4)

(3)

(2)

(1)

0

1 9 9 9 - 0 0

2 0 0 0 - 0 1

2 0 0 1 - 0 2

2 0 0 2 - 0 3

2 0 0 3 - 0 4

2 0 0 4 - 0 5

2 0 0 5 - 0 6

2 0 0 6 - 0 7

2 0 0 7 - 0 8

2 0 0 8 - 0 9

2 0 0 9 -1 0

Source: Ministry of Finance

Key Macroeconomic Targets for the Next Five Years

8/8/2019 Dr Shah April 2006

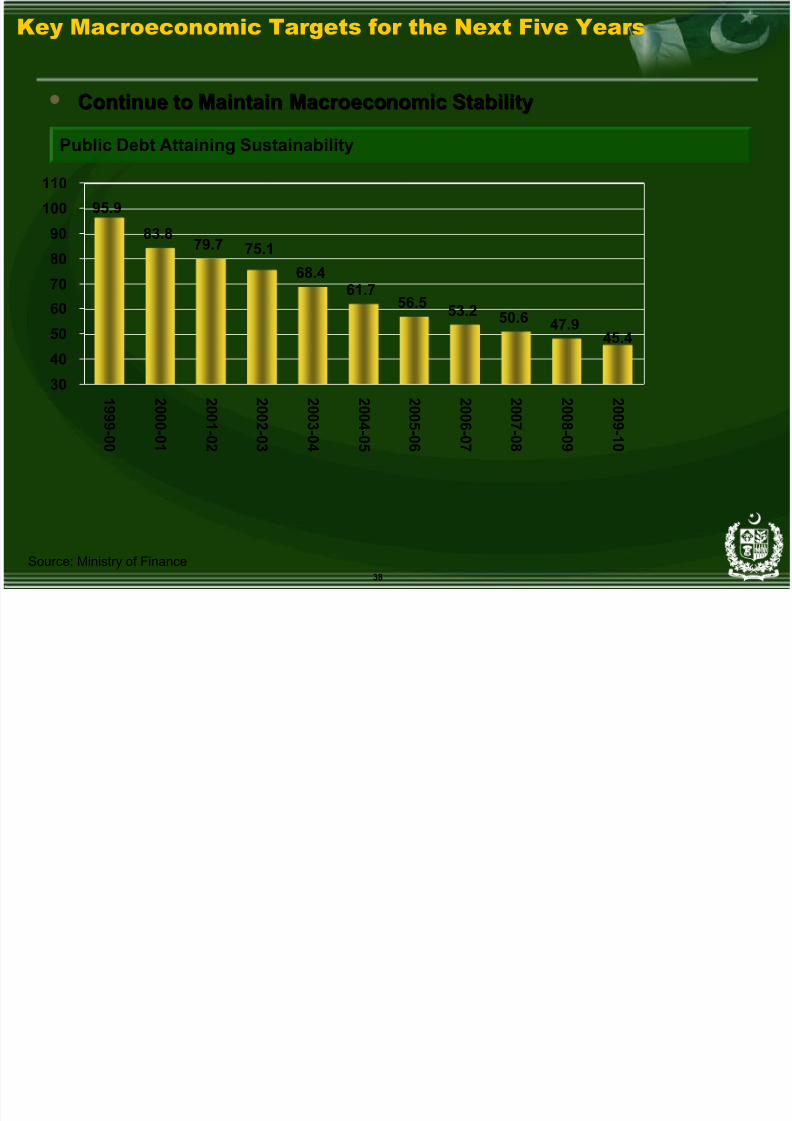

http://slidepdf.com/reader/full/dr-shah-april-2006 38/48

38

Public Debt Attaining Sustainability

• Continue to Maintain Macroeconomic StabilityContinue to Maintain Macroeconomic Stability

83.879.7

68.461.7

56.5 53.2 50.6

75.1

45.447.9

95.9

30

40

50

6070

80

90

100

110

1 9

9 9 - 0 0

2 0

0 0 - 0 1

2 0

0 1 - 0 2

2 0

0 2 - 0 3

2 0

0 3 - 0 4

2 0

0 4 - 0 5

2 0

0 5 - 0 6

2 0

0 6 - 0 7

2 0

0 7 - 0 8

2 0

0 8 - 0 9

2 0

0 9 -1 0

Key Macroeconomic Targets for the Next Five Years

Source: Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 39/48

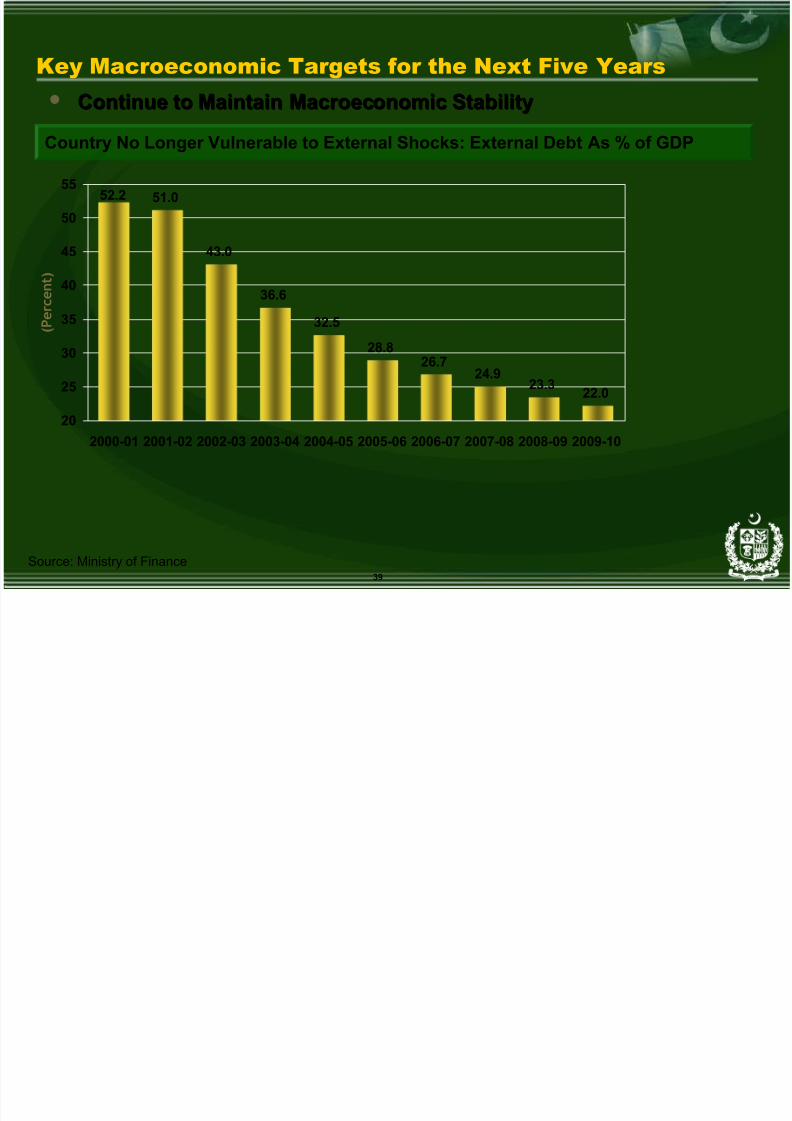

39

Country No Longer Vulnerable to External Shocks: External Debt As % of GDP

• Continue to Maintain Macroeconomic StabilityContinue to Maintain Macroeconomic Stability

51.0

43.0

36.6

32.5

28.826.7

24.923.3

22.0

52.2

20

25

30

35

40

45

50

55

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

( P e r c e n t

)

Key Macroeconomic Targets for the Next Five Years

Source: Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 40/48

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 41/48

41

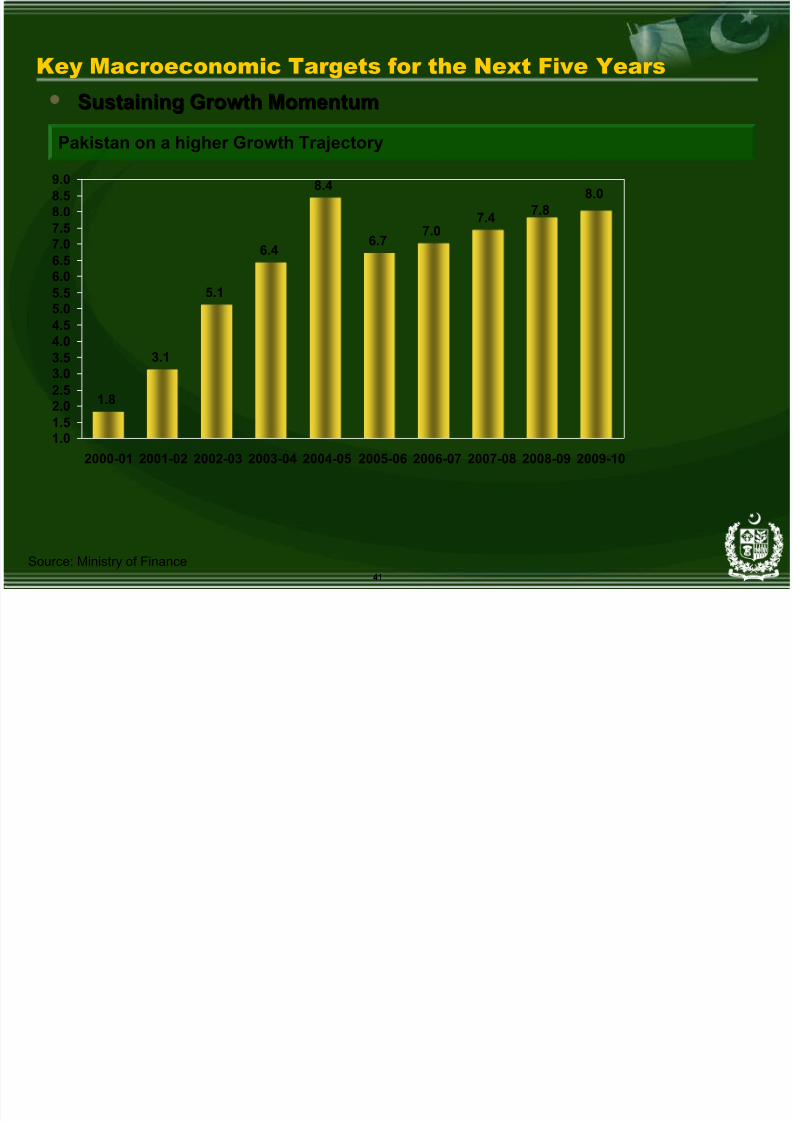

Pakistan on a higher Growth Trajectory

• Sustaining Growth MomentumSustaining Growth Momentum

1.8

3.1

5.1

6.4

8.4

6.77.0

7.4 7.88.0

1.01.52.02.53.03.54.04.55.05.56.0

6.57.07.58.08.59.0

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

Key Macroeconomic Targets for the Next Five Years

Source: Ministry of Finance

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 42/48

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 43/48

43

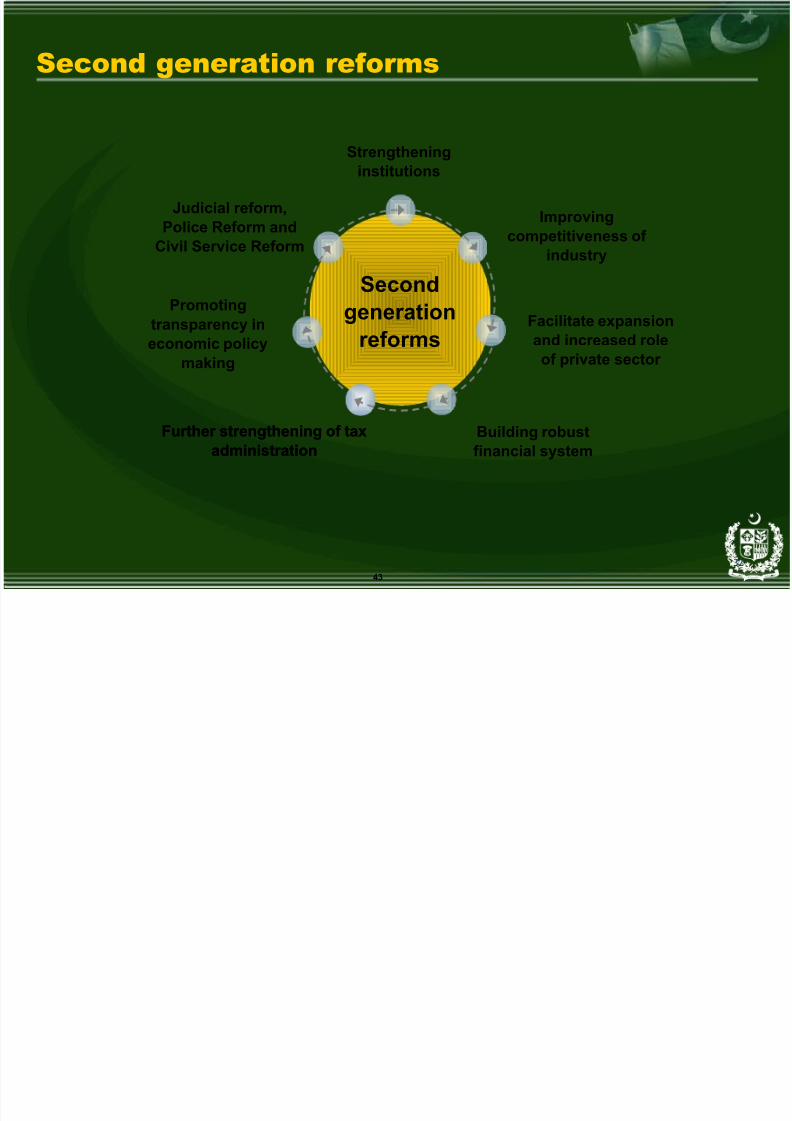

Secondgeneration

reforms

Second generation reforms

Improvingcompetitiveness of

industry

Facilitate expansionand increased role

of private sector

Further strengthening of taxadministration

Promotingtransparency ineconomic policy

making

Judicial reform,Police Reform and

Civil Service Reform

Strengtheninginstitutions

32

Building robustfinancial system

Further strengthening of taxadministration

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 44/48

44

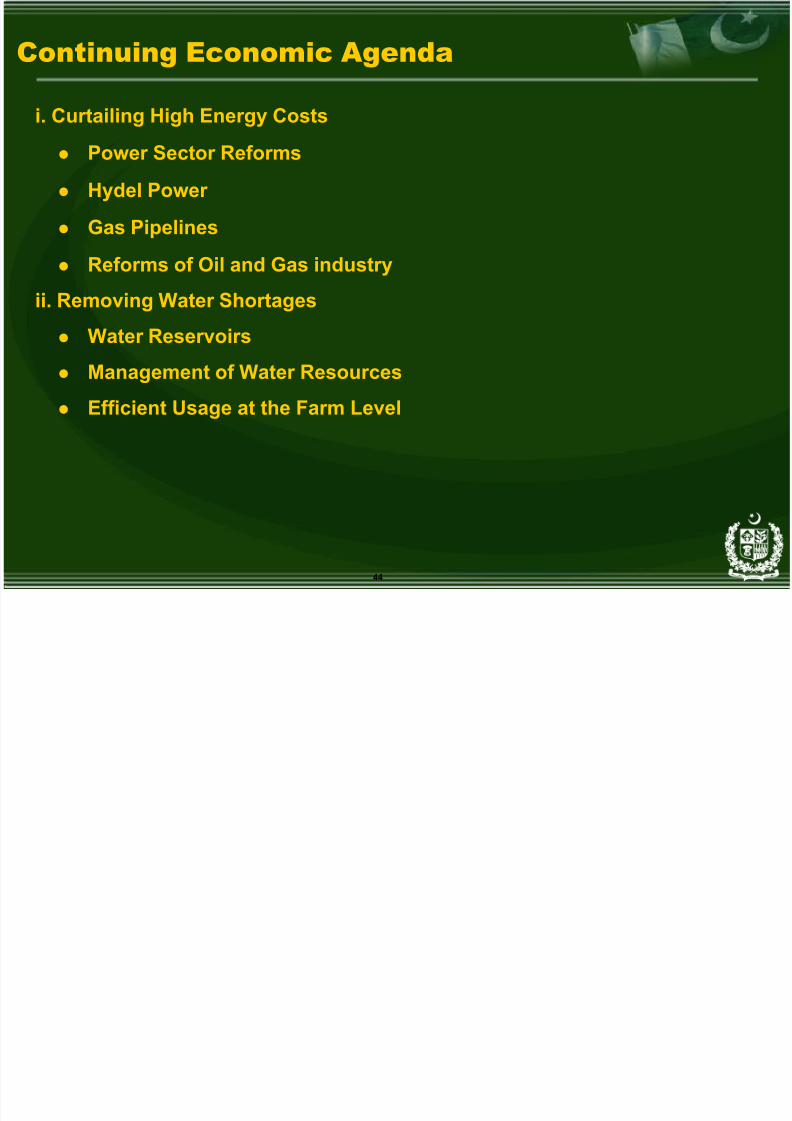

Continuing Economic Agenda

i. Curtailing High Energy Costs

• Power Sector Reforms

• Hydel Power

• Gas Pipelines

• Reforms of Oil and Gas industry

ii. Removing Water Shortages

• Water Reservoirs

• Management of Water Resources

• Efficient Usage at the Farm Level

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 45/48

45

Continuing Economic Agenda

iii. Improving Logistics & Removing Supply Chain Constraints

• National Trade Corridor

• Retail & Wholesale Markets Development

• Ports Modernization

• Modernizing Transport Fleet

iv. Unlocking the Land Bank

• NIPs (National Industrial Parks)

• Release of Government Land ( Defence, Railways, Provincial Governments

etc.)

• Computerization of Land Transactions

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 46/48

46

Continuing Economic Agenda

v. Removing Skills Gap & Enhancing Productivity

•

NTEVTA• 5 New Engineering Universities & HEC Initiatives

• Education Sector Reforms

vi. Boosting Agriculture Sector Development

• Livestock Sector

• Fisheries

• Horticulture & Value Added Agriculture

• Research & Extension Services

• Yield Enhancement

C i i E i A d

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 47/48

47

Continuing Economic Agenda

vii. Tourism & Hotel Industry Expansion

viii. SMEs & One Village One Product

ix. Sustaining Industrial Development Beyond Textiles

x. Developing Knowledge Based Industry &

Outsourcing

xi. Strengthening Growth Prospects of Service Sector

xii. Obtaining Preferential Access to Global Markets

8/8/2019 Dr Shah April 2006

http://slidepdf.com/reader/full/dr-shah-april-2006 48/48

Conclusions

i. Economy Continues to Grow Strongly

ii. Reduction in Unemploymentiii. Growing Profitability of Private Sector

iv. Robust Banking System

v. Strong Growth in Diversified Sectorsvi. Vibrant Telecom Sector

vii. Strong Domestic & External Demand Sustaining Economic

Growthviii. Growing opportunities in Infrastructure

ix. Growing Role of the Private sector