jyoti paryani

TRANSCRIPT

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 1/77

A

PROJECT REPORT

On

Portfolio Management Services

FOR

“INDIA INFOLINE LTD”.

SUBMITTED TO UNIVERSITY OF PUNE

BY

Jyoti Paryani

IN PARTIAL FULFILLMENT OF 2 YEARS FULL TIME COURSE

MASTERS IN BUSINESS ADMINISTRATION (M.B.A. )

Batch (2009-2010)

K.K.W.I.E.E.R , Nashik

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 2/77

ACKNOWLEDGEME NT

I hereby take the opportunity to express my gratitude towards those who have made

great contribution in completion of this project work. I feel immense pleasure to

thanks Mr.Amit Thakre , Head of Branch, India Infoline, Pune who very kindly

helped me in providing necessary information and guidance from time to time.

I would specially thank Mr. Kuzema Jinwala (Team Leader) for being my project

guide.

The success of any task lies in the effective input, but this cannot be obtained without

proper guidance of the concern authorities and their co-operation. I would like to

thank Prof.Ajinkya Joshi for guiding me throughout the project. I wish to

acknowledge those many people whose feedback has enable me to satisfactorily

complete my summer training.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 3/77

. INDEX

Sr. No. Topic Page No.

1) Executive Summary 4

2) Company Profile 6

3) Objective of Project 21

4) Research Methodology 23

5) Introduction to Investments 27

6) Portfolio Management 31

7) Investment Avenues 44

8) Virtual Portfolio

64

9) Findings 67

10) Suggestions 69

11) Limitations 71

12) Conclusion 74

13) Bibliography 77

14) Annexure 79

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 4/77

CHAPTER 1:

EXECUTIVE SUMMARY

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 5/77

Executive summary

As the title suggest the project report has been prepared regarding the growthand development of online trading in India. Online trading was initiated by NSE inIndia and soon after the other exchanges also followed it.

• There was a major boom in yr. 2000 when lots of online trading companies

came with a bang but only few were survived because of lack of computer knowledge

and low internet penetration. There are two types of online trading companies, one is

the banking online trading companies and the other is non-banking trading. A few

examples of banking online trading companies are HDFC securities, ICICI

direct.com, UTI securities etc.

• On the other hand non -banking trading companies are India Infoline ltd.

IL&FS investsmart, Religare securities Angel Broking, Reliance Money etc. A study

was undertaken to determine the growth of various online trading companies in India

in terms of trade done by them through online trading portal and services provided by

them.

• Major findings indicates that out of a survey of 100 respondents it was seen

that most of the investors prefer online trading because of few major factors such as

time saving, convenience, protection through Freudian brokers etc. although during

my research project I’ve seen that most of the respondents feel online trading, a

secure way of investing into stock market still a few of them feel that it’s unsafe and

a bit complicated but they posses information about online trading.

• Today the online trading companies are having cut-throat competition in their

offerings regarding the brokerage ,discounts ,lower margin money and zero balance

accounts. Due to the rising education awareness and use of internet there is a huge

potential for online trading in future and companies must come up with innovative

offerings to capture the untapped market.

•

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 6/77

CHAPTER 2:

COMPANY & Product PROFILE

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 7/77

India Infoline Ltd. (IIL) is a financial services holding company engaged in the

brokerage and financial services business. The company provides securities related

products, broking, investment management, insurance, banking and institutional

brokerage products to retail and institutional customers. The company operates in six

business segments including Broking, Credit and Finance, Asset Management,

Wealth Management, Insurance Distribution and Investment Banking through its

operating subsidiaries. IIL provides online services through two Internet portals,

indiainfoline.com and 5paisa.com, which are information resource centers with an

analysis of Indian business, finance, and investments. The company provides its

services through a network of 758 business locations including 607 branches and 151

franchisees in 346 cities in India. The company’s key area of operations includes

India, Singapore, New York and Dubai. The company is headquartered in Mumbai,

India.

The company reported revenues of (Rupee) INR 9,624.40 million during the fiscal

year ended March 2009, a decrease of 5.97% from 2008. The operating profit of the

company was INR 2,194.90 million during the fiscal year 2009, a decrease of 13.49%

from 2008. The net profit of the company was INR 1,448.19 million during the fiscal

year 2009, a decrease of 9.42% from 2008.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 8/77

Performance of the company:

1995

Incorporated as an equity research and Consulting firm with a client base that

included leading FIIs, banks, consulting firms and corporate.

1999

Restructured the business model to embrace the internet; launched

www.indiainfoline.com ; Mobilized capital from reputed private equity investors.

2000Commenced the distribution of personal financial products; launched online equity

trading; entered life insurance distribution as a corporate agent. Acknowledged by

Forbes as ‘Best of the Web’ and‘..must read for Investors’.

2004

Acquired commodities broking license; launched Portfolio Management Service.

2005

Listed on the Indian stock Markets.2006

Acquired Membership Of DGCX; launched investment banking Services.

2007

Launched a proprietary trading platform; inducted an institutional equities team;

formed a Singapore subsidiary; raised over USD 300mn in the

group;launchedconsumerfinance business under the ‘Money line’Brand.

2008

Launched wealth management services under the ‘IIFL Wealth’brand; set up India

Info line Private Equity fund; received the Insurance broking license from

IRDA;received the venture capital license; received in principle approval to sponsor a

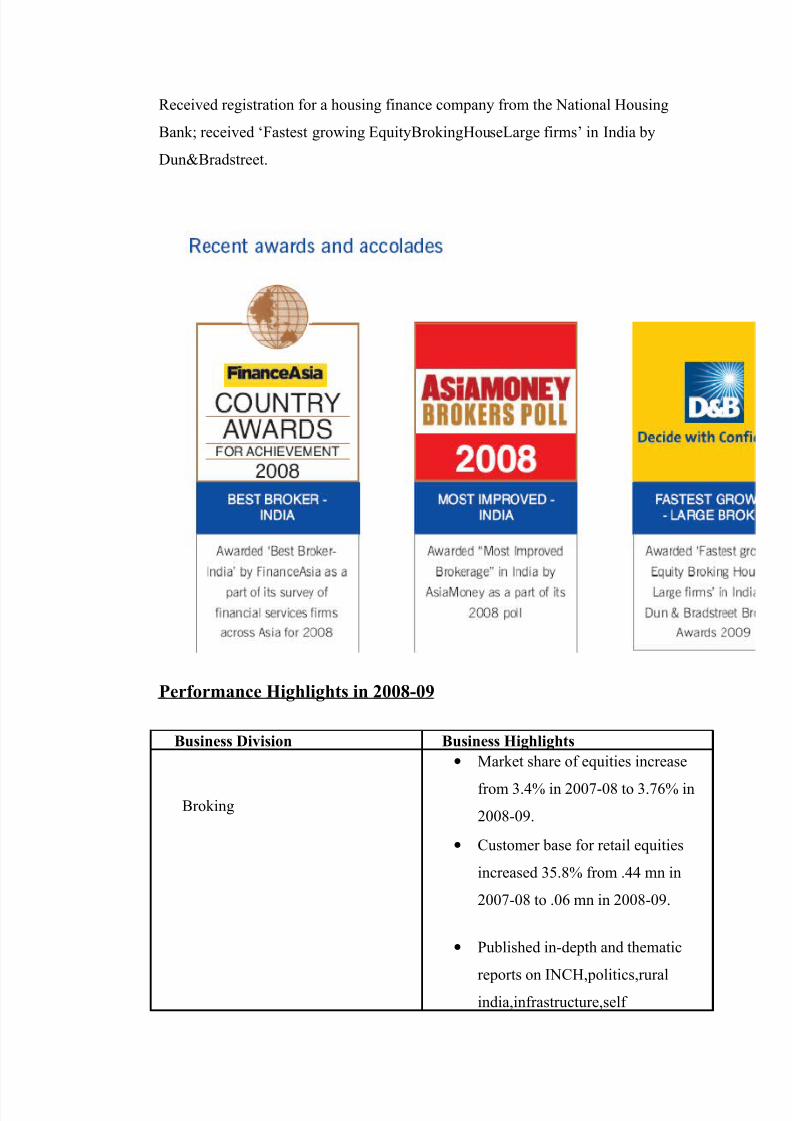

mutual fund;received ‘Best broker- India’ award from FinanceAsia ; ‘Most Improved

Brokerage- India’ award from Asiamoney.

2009

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 9/77

Received registration for a housing finance company from the National Housing

Bank; received ‘Fastest growing EquityBrokingHouseLarge firms’ in India by

Dun&Bradstreet.

Performance Highlights in 2008-09

Business Division Business Highlights

Broking

• Market share of equities increase

from 3.4% in 2007-08 to 3.76% in

2008-09.

• Customer base for retail equities

increased 35.8% from .44 mn in

2007-08 to .06 mn in 2008-09.

• Published in-depth and thematic

reports on INCH,politics,ruralindia,infrastructure,self

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 10/77

commodities, utilities and India

worming.

Wealth and asset Management • Introduce the family office

platform.

• Raised around Rs.1.8 bn in the

largest single day debenture listing

of its kind.

• Establish the infrastructre and

knowledge capital for Office Store

Asset Management Services..

Credit and Finance

• Proactively suspended personal

loans and mortgages business from

September 2008, while the personal

loan business is still suspended, the

mortgages business has been Re-

Started.

• Revenue at Rs.2654.1 mn in 2008-

09 against Rs.1937.5 mn in 2007-

08.

• Registered the Housing FinanceSubsidiary with NHB.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 11/77

PRODUCTS

Equity

India Infoline provided the prospect of researched investing to its clients,

which was hitherto restricted only to the institutions. Research for the retail

investor did not exist prior to India Infoline. India Infoline leveraged

technology to bring the convenience of trading to the investor’s location of

preference (residence or office) through computerized access. India Infoline

made it possible for clients to view transaction costs and ledger updates in real

time.

Portfolio management services

Our Portfolio Management Service is a product wherein an equity investment

portfolio is created to suit the investment objectives of a client. We at India Infoline

invest your resources into stocks from different sectors, depending on your risk-return

profile. This service is particularly advisable for investors who cannot afford to givetime or don't have that expertise for day-to-day management of their equity portfolio.

It is all about your money, being managed by the experts, while you continue with

your routine life. Isn't it simple and totally hassle free.

What's more, you can keep track of your dividends / bonus / rights issues with

paperless tracking. So you always know how fast your investment is growing. It

basically means assigning the right job to the right person.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 12/77

Salient Features of India Infoline PMS:

• Expert team of Research Analysts• Stock Picking done by the Investment Committee

• Dedicated Relationship Manager

• Technology and Service driven Back-Office

Wealth Management Services

The key to achieving a successful Investment Portfolio is to have a carefully

planned financial strategy based on a thorough understanding of the client's

investment needs and risk appetite. The IIFL Private Wealth Management Team of

financial experts will recommend an appropriate financial strategy to effectively

meet your investment requirements.

Our Financial Advisor will analyze:

• Your cash-flow requirements

• Your risk appetite

• Desired investment horizon

• Long-term goals

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 13/77

DEMAT SERVICE

Dematerialization and trading in the demat mode is the safer and faster alternative to

the physical existence of securities. Demat as a parallel solution offers freedom from

delays, thefts, forgeries, settlement risks and paper work. This system works through

depository participants (DPs) who offer demat services and the securities are held in

the electronic form for the investor directly by the Depository.

India Infoline Services offers dematerialization services to individual and corporate

investors. They have a team of professionals and the latest technological expertise

dedicated exclusively to our demat department, apart from a national network of

franchisee, making their services quick, convenient and efficient.

At India Infoline , their commitment is to provide a complete demat solution which is

simple, safe and secure.

Here mainly two types of services provided by the company to the

customer for Demat A/C that is (1) Online A/C and (2) Offline A/C.

1. Online Account: Nowadays online A/C is more popular than offline A/C. In

online A/C what company will do, they simply provide terminal to the customer

and customer can do trading himself/herself when he/she wants. The online A/C

will charge 750/- Rs. (*It varies from company to company). In these there 3 types

of facility company will provide to the customer as per the customer’s

requirement.

2. Offline Account: This is the traditional way of buying or selling shares. In

this, customer can place the order via telephone or directly by sitting in the

company. The customers who are busy in their jobs or businesses, they can place the

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 14/77

order via telephone and the customers who are not that much of busy, they can come

to the office and by sitting there whole day they can place the order.

India Infoline offers trading on a vast platform; National Stock Exchange, Bombay

Stock Exchange. More importantly, they make safe to the maximum possible extent,

by accounting for several risk factors and planning accordingly. They assisted in this

task by their in-depth research, constant feedback and sound advisory facilities. Their

highly skilled research team, comprising of technical analysts as well as fundamental

specialists, secure result oriented information on market trends, market analysis and

market predictions. This crucial information is given as a constant feed back to the

customers, through daily reports delivered along with their updated portfolio. Besides

this they are also offer special portfolio analysis packages that provide daily technical

advice on scrip’s for successful portfolio management and provide customize

advisory services to help customer make the right financial moves that are

specifically suited to their portfolio.

Factors such as their success in the electronics custody business has helped build on

our trading of trust even more. Consequently their retail client base expanded very

fast. To empower the investor further they have made serious efforts to ensure that

their research calls are disseminated systematically to all their stock broking clients

through various delivery channels like e-mail, chat, SMS, phone calls etc.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 15/77

MUTUAL FUNDS

India Infoline is glad to announce that customers will now be able to invest in Mutual

Funds through India Infoline. They have started this service for online mutual funds,

and in the near future will be expanding our scope to include a whole lot more.

Applying for a mutual fund through them is open to everybody, regardless of whether

you are a India Infoline India Infoline customer or not. For investing in mutual funds

through India Infoline you have to just download the form from internet, fill it and

submit it in any India Infoline office.

CORNER STONES OF STRAREGY

1) It focuses on retail segment.

2) It builds a strong Pan-India network managed by experienced professionals,

build presence across both metros and Class A/B town.

3) It builds full-service capabilities leveraging the network-offer the entire gamut

of financial services, backed by strong transaction processing and high

volume handling capability.

4) It has established a high degree of customer ownership and top-of-mind recall

in the local markets- ensures steady customer traffic and repeat business.5) It builds a trusted brand; ensure high visibility

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 16/77

CHAPTER 3:

OBJECTIVE OF THE STUDY

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 17/77

OBJECTIVE OF THE STUDY

My project on “ Portfolio Management Services ” is meant to study the nature of

different investment instruments available in the market and then finally suggest the

same to the clients in the form of a structured product. I do this by suggesting the

investor as to go for which all investments that can fetch out real good returns to them

in future, as per their risk appetite regarding the investments and their needs. I

suggest them the investments that they can opt for and the one’s which can bring a

huge value addition to their portfolio. Few objectives are given below:

To guide clients to determine the level of investment risk they are willing to

take and then suggest them an appropriate asset allocation.

To study and compare various investment instruments available in the market.

To advise High Net-worth Individuals (HNI’s) on different investment avenues

like mutual funds, insurance, real estate, stock broking etc.

To know the investment pattern of the individuals & hence creating a better

portfolio of investment for these individual clients.

To advise them on tax planning, so as to minimize their tax liability.

To provide the client with an appropriate asset allocation mix based on certain

factors time horizon and risk tolerance.

Understanding consumer behavior towards various investment options

available.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 18/77

CHAPTER 4:

METHODOLOGY OF STUDY

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 19/77

Research can be defined as a systemized effort to gain new knowledge. A

research is carried out by different methodologies which have their own pros and

cons. Research methodology is a way to solve research in study and solving research

problems along with logic behind them are defined through research methodology.

Thus while talking about research methodologies we are not only talking of research

methods but also consider the logic behind the methods. We are in context of our research studies and explain why it is being used a particular method or technique and

why the others are not used. So that research result is capable of being evaluated

either by researcher himself or by others.

RESEARCH METHODOLOGY

Research has its special significance in solving various operational and

planning problems of business and industry. Research methodology is a way to

systematically analyze the research problem.

I have executed the project after prior discussion with our guide and structured in the

following steps:

a. Preparation of a questionnaire

b. The focal point of the designing the questionnaire was to comprehend the

current investment scenario with respect to tax planning part.

c. This questionnaire was primarily aimed to respondents who belong to the

service and business class people

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 20/77

The questionnaires were discussed through personal interface with the

respondents.

ASSUMPTIONS:

1. It has been assumed that sample of hundred represents the whole population.

2. The information given by the customer is unbiased.

Development of Working Hypothesis

The hypothesis could be developed by discussing with the consulting

department heads and guides about this exploratory research and reach to the

conclusion that the data is to be collected by personal interaction with the clients,

asking them about their investment planning and their need for financial advisory

service from India Infoline.

First of all, are they aware of tax and investment planning or not and then

analyzing the findings to reach to the objectives of research.

Sources of Data:

PRIMARY DATA

This research is solely based on primary research done by means of

questionnaires targeted to respondents who primarily belong to the business and

service sector.

It is very essential in the research process to know the accuracy of the finding’s which

depends on how systematically the study has been carried out so that it can make

sense.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 21/77

The data required for the project was about the customers and therefore this data was

a confidential for the company.

SECONDARY DATA

Secondary data is a data that has been collected earlier for some purpose other than

the purpose of the present study. I have collected data by referring book and websites

for carrying out my project.

Also, secondary data can be a useful benchmark against which the findings of

the study can be tested. This study is highly dependent on the secondary data for

various facts and figures.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 22/77

CHAPTER 5

INTRODUCTION TO

INVESTMENTS

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 23/77

INVESTORS DESK

Today an investor is interested in tracking the value of his investments, whether to

invest directly in the market or through some funds which play in the market. This

dynamic change has taken place because of a number of reasons. With globalization

and the growing competition in the investments opportunity available, investor would

have to make guided and have to make rational decisions on whether they get an

acceptable return on the current investments, or if there is needs to switch to another

investments plan.

It is of paramount importance to keep in mind the risk involved in any investment.

Before making any investment plans for any client, firstly we need to know his/her

risk taking ability . “Investments that have the greatest return potential tend to

give the greatest risk potential.”

On the other side of the coin, investments with conservative return are the least risky.

So for successful and stress free investment, a balance between the financial objective

and the ability to tolerate risk is the best. This overall balance can be obtained by

diversifying money across low, medium and high-risk investments so that both short

term and long term goals are met.

MEANING:

The money earn is partly spent and the rest saved for meeting future expenses.

Instead of keeping the savings idle person may like to use savings in order to get

return on it in the future. This is called Investment.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 24/77

NEEDS OF INVESTMENT :

One needs to invest:

• To earn return on idle resources.

• To generate a specified sum of money for a specific goal in life

• To make a provision for an uncertain future.

One of the important reasons why one needs to invest wisely is to meet the cost of

Inflation . Inflation is the rate at which the cost of living increases. The cost of

living is simply what it costs to buy the goods and services you need to live.

Inflation causes money to lose value because it will not buy the same amount of a

good or a service in the future as it does now or did in the past. For example, if

there was a 6% inflation rate for the next 20 years, the aim of investments should

be to provide a return above the inflation rate to ensure that the investment does

not decrease in value.

RIGHT TIME FOR INVESTMENT

The sooner one starts investing the better. By investing early investor allow his

investments more time to grow, whereby the concept of compounding increases

income, by accumulating the principal and the interest or dividend earned on it,

year after year. The three golden rules for all investors are:

• To Invest early,

• To Invest regularly,

• To Invest for long term and not short term.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 25/77

OPTIONS AVAILABLE FOR INVESTMENT

One may invest in:

• Physical assets like Real Estate, Gold/ Jewellery, Commodities etc.

and/or

• Financial assets such as Fixed Deposits with Banks, Small Saving

Instruments with Post Offices, Insurance/Provident/Pension Fund, Mutual

Fund etc. or Securities market related instruments like Shares, Bonds, and

Debentures etc.

VALUE ADDITION TO THE ORGANIZATION

Through this project I can bring in long term clients for my organization by

offering “Portfolio Management Services” to them.

Through this project I am not only bringing long term clients for my

organization but also creating a word of mouth publicity of my organization

by offering the best services to the clients so that a chain of more consumers is

created through these services.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 26/77

CHAPTER 6

INVESTMENTS AVENUES

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 27/77

VARIOUS AVAENUES FOR INVESTMENT

BONDS

Individuals have surplus funds in the form of savings which they want to invest.

Companies need funds to undertake good projects with high returns. Companies

provide individuals with instruments to invest their savings in.

One such instrument is corporate bonds. Similarly, governments also need funds for

various developmental projects. Further, the government also needs to raise money to

finance the fiscal deficit. They too tap the savings by issuing various kinds of bonds.

Characteristics of a bond:

A bond, whether issued by a government or a corporation, has a specific maturity

date, which can range from a few days to 20-30 years or even more. Based on the

maturity period, bonds are referred to as bills or short-term bonds and long-term

bonds.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 28/77

Bonds have a fixed face value, which is the amount to be returned to the investor

upon maturity of the bond. During this period, the investors receive a regular

payment of interest, semi-annually or annually, which is calculated as a certain

percentage of the face value and know as a 'coupon payment.'

A story goes that in the old days, bond certificates used to come with coupons to

claim interest from the issuer of the bond; hence, the name coupon payments.

However, nowadays, with paperless issues of scripts (demat), coupons are no longer

in use, but the name has stuck and the interest payments are still known as coupon

payments.

Issuing a bond :

The government, public sector units and corporate are the dominant issuers in the

bond market. The central government raises funds through the issue of dated

securities (securities with maturity period ranging from two years to 30 years, long-

term) and treasury bills (securities with maturity periods of 91 or 364 days, short-

term).

The central government securities are issued for a minimum amount of Rs 10,000

(face value). Thereafter they are issued in multiples of Rs 10,000. They are issued

through an auction carried out by the Reserve Bank of India.

State governments go about raising money through state development loans. Local

bodies of various states like municipalities also tap the bond market from time to

time. Bonds are also issued by public sector banks and PSUs. Corporate on the other

hands raise funds by issuing commercial paper (short-term) and bonds (long-term).

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 29/77

Bonds can be issued at par, which means that the price at which one unit of the bond

is being sold is same as the face value. Alternatively, they can be issued at a discount

(less than the face value) or a premium (more than the face value).

For e.g. , a bond with a face value of Rs 100, if issued at Rs 100, is said to be issued

at par. If it is issued at, say, Rs 95, it will be said to have been issued at a discount and

conversely, if issued for, say, Rs 110, at a premium.

Investors:

Banks are the largest investors in the bond market. In the low-interest scenario that prevailed, it made more sense for banks to invest in government bonds than to give

out loans. Mutual funds, in order capitalize on low interest rates, started a good

number of debt funds that mobilized a significant amount of money from the

investors.

Thus, mutual funds emerged as important players in the bond markets. However, in

the recent past with the interest rates on their way up, the performance of debt funds

has not been good and so the presence of mutual funds in the bond market has been

limited.

Foreign institutional investors are also allowed to invest in the bond market, though

within certain limits. Also, regulations mandate provident funds and pension funds to

invest a significant proportion of their funds mobilized in government securities and

PSU bonds.

Hence, they continue to remain large investors in the bond market in India. The same

holds true for charitable institutions, societies and trusts.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 30/77

Since January 2002, individuals categorized by RBI as retail investors can participate

in the auction carried out by RBI. They can submit bids through banks or primary

dealers to invest in these securities on a non-competitive basis.

The minimum bid has to be for an amount of Rs 10,000 (and there on in multiples of

Rs 10,000) and a single bid cannot exceed Rs 1 crore (Rs 10 million). Hence,

company X must ensure that the price, at which they are offering their Bond, is

competitive with similar bonds in the market, and should provide similar yield to the

investors.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 31/77

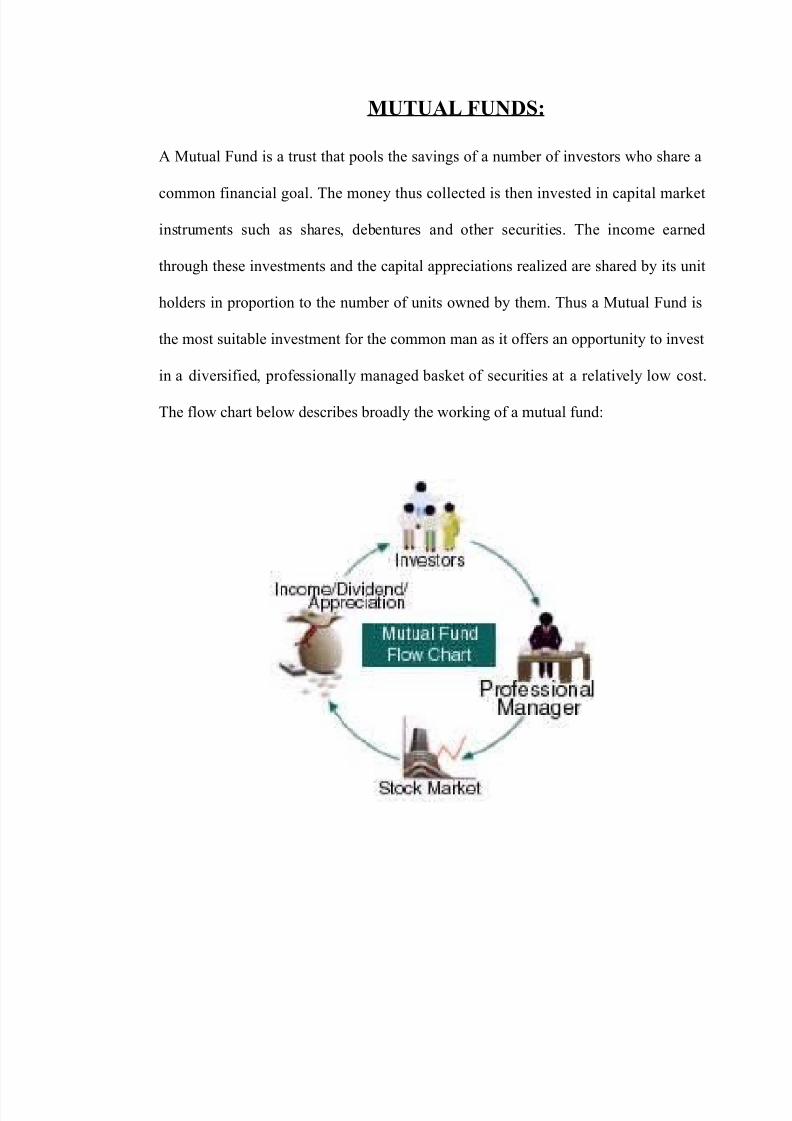

MUTUAL FUNDS:

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is then invested in capital market

instruments such as shares, debentures and other securities. The income earned

through these investments and the capital appreciations realized are shared by its unit

holders in proportion to the number of units owned by them. Thus a Mutual Fund is

the most suitable investment for the common man as it offers an opportunity to invest

in a diversified, professionally managed basket of securities at a relatively low cost.

The flow chart below describes broadly the working of a mutual fund:

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 32/77

TYPES OF MUTUAL FUNDS

Mutual Funds have specific investment objectives such as growth of capital, safety of

principal current income or tax exempt income, one can select one fund or any

number of different funds to help one meets ones specific goals. In general mutual

fund fall under 3 general categories: -

Equity fund invest in shares of common stocks.

Fixed income funds invest in government or corporate securities which offer fixed

ROR

Balanced fund invest in a combination of both stocks and bonds.

Open-Ended Schemes:

These funds are sold at the NAV based prices, generally calculated on every business

day. These schemes have unlimited capitalization, open-ended schemes do not have a

fixed maturity - i.e. there is no cap on the amount you can buy from the fund and the

unit capital can keep growing. These funds are not generally listed on any exchange.

Open-ended funds are bringing in a revival of the mutual fund industry owing to

increased liquidity, transparency and performance in the new open-ended funds

promoted by the private sector and foreign players. Open-ended funds score over

close-ended ones on several counts. Some of these are listed below:

a) Any time exit option : The issuing company directly takes the responsibility of

providing an entry and an exit. This provides ready liquidity to the investors and

avoids reliance on transfer deeds, signature verifications and bad deliveries.

b) Any time entry option : An open-ended fund allows one to enter the fund at

any time and even to invest at regular intervals (a systematic investment plan).

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 33/77

The open ended funds offered by SCMF Classic Equity Fund, Premier Equity Fund,

Imperial Equity Fund Super Saver income Fund, Dynamic Bond, Cash Fund,

Liquidity manager, Floating Rate Fund, Govt. Securities Fund etc.

Close-Ended Schemes

Schemes that have a stipulated maturity period, limited capitalization and the units

are listed on the stock exchange are called close-ended schemes.

These schemes have historically seen a lot of subscription. This popularity is

estimated to be on account of firstly, public sector MFs having floated a lot of close-

ended income schemes with guaranteed returns and secondly easy liquidity on

account of listing on the stock exchanges. The closed-ended funds managed by

SCMF are Enterprise Equity Fund, Fixed Maturity Plan,

Tri-Star Series etc.

CLASSIFICATION ACCORDING TO INVESTMENT

OBJECTIVESi) Growth Funds:

These funds seek to provide growth of capital with secondary emphasis on dividend.

They invest in shares with a potential for growth and capital appreciation. Because

they invest in well-established companies where the company itself and the industry

in which it operates are thought to have good long-term growth potential, growth

funds provide low current income.

Growth funds generally incur higher risks than income funds in an effort to secure

more pronounced growth. These funds may invest in a broad range of industries or

concentrate on one or more industry sectors. Growth funds are suitable for investors

who can afford to assume the risk of potential loss in value of their investment in the

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 34/77

hope of achieving substantial and rapid gains. They are not suitable for investors who

must conserve their principal or who must maximize current income.

ii) Growth and Income Funds:

Growth and income funds seek long-term growth of capital as well as current income.

The investment strategies used to reach these goals vary among funds. Some invest in

a dual portfolio consisting of growth stocks and income stocks, or a combination of

growth stocks, stocks paying high dividends, preferred stocks, convertible securities

or fixed-income securities such as corporate bonds and money market instruments.

Others may invest in growth stocks and earn current income by selling covered call

options on their portfolio stocks. Growth and income funds have low to moderate

stability of principal and moderate potential for current income and growth. They are

suitable for investors who can assume some risk to achieve growth of capital but who

also want to maintain a moderate level of current income.

iii) Fixed-Income Funds:

The goal of fixed income funds is to provide current income consistent with the

preservation of capital. These funds invest in corporate bonds or government-backed

mortgage securities that have a fixed rate of return. Within the fixed-income category,

funds vary greatly in their stability of principal and in their dividend yields. High-

yield funds, which seek to maximize yield by investing in lower-rated bonds of

longer maturities, entail less stability of principal than fixed income funds that invest

in higher-rated but lower-yielding securities. Some fixed-income funds seek to

minimize risk by investing exclusively in securities whose timely payment of interest

and principal is backed by the full faith and credit of the Indian Government. Fixed-

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 35/77

income funds are suitable for investors who want to maximize current income and

who can assume a degree of capital risk in order to do so.

iv) Balanced Funds:

The Balanced fund aims to provide both growth and income. These funds invest in

both shares and fixed income securities in the proportion indicated in their offer

documents. This fund is ideal for investors who are looking for a combination of

income and moderate growth.

v) Money Market Funds/Liquid Funds:

For the cautious investor, these funds provide a very high stability of principal while

seeking a moderate to high current income. They invest in highly liquid, virtually

risk-free, short-term debt securities of agencies of the Indian Government, banks and

corporations and Treasury Bills. Because of their short-term investments, money

market mutual funds are able to keep a virtually constant unit price; only the yield

fluctuates. Therefore, they are an attractive alternative to bank accounts. With yields

that are generally competitive with - and usually higher than -- yields on bank savings

account, they offer several advantages. Money can be withdrawn any time without

penalty. Although not insured, money market funds invest only in highly liquid,

short-term, top-rated money market instruments. Money market funds are suitable for

investors who want high stability of principal and current income with immediate

liquidity.

vi) Specialty/Sector Funds:

These funds invest in securities of a specific industry or sector of the economy such

as health care, technology, leisure, utilities or precious metals. The funds enable

investors to diversify holdings among many companies within an industry, a more

conservative approach than investing directly in one particular company. Sector funds

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 36/77

offer the opportunity for sharp capital gains in cases where the fund's industry is "in

favor" but also entail the risk of capital losses when the industry is out of favor.

While sector funds restrict holdings to a particular industry, other specialty funds

such as index funds give investors a broadly diversified portfolio and attempt to

mirror the performance of various market averages. Index funds generally buy shares

in all the companies composing the BSE Sensex or NSE Nifty or other broad stock

market indices. They are not suitable for investors who must conserve their principal

or maximize current income.

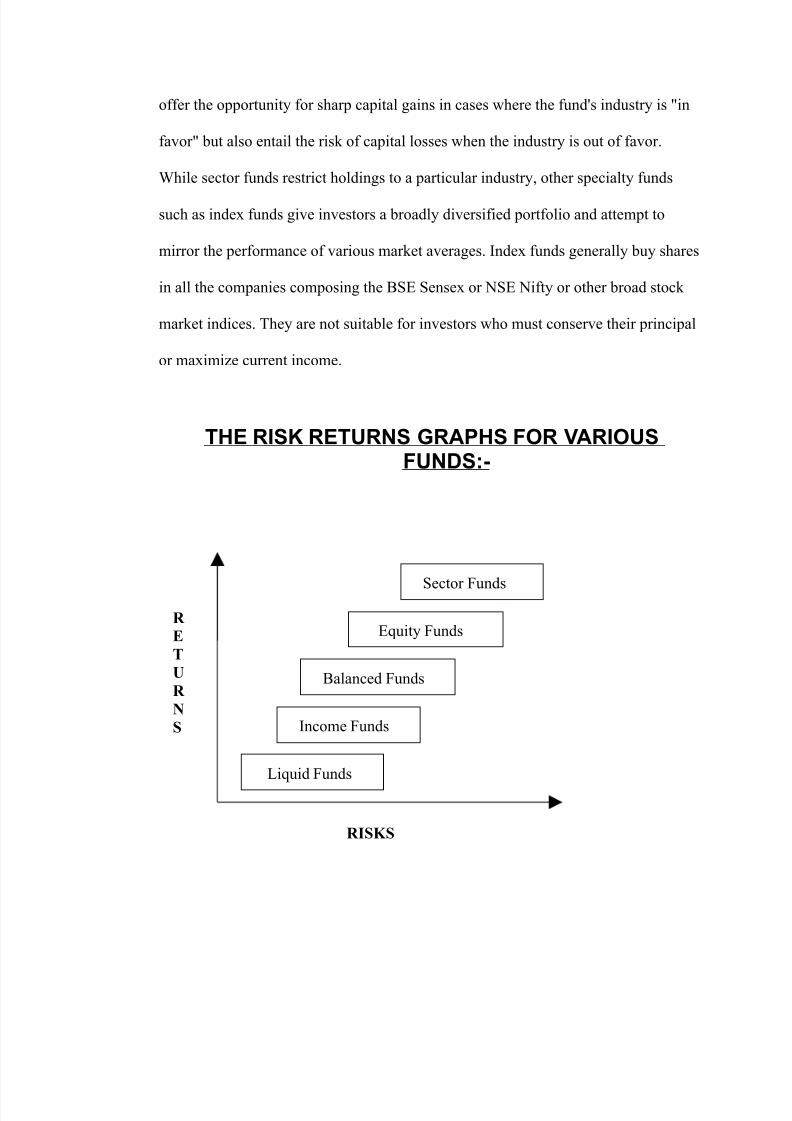

THE RISK RETURNS GRAPHS FOR VARIOUSFUNDS:-

Liquid Funds

Income Funds

Balanced Funds

Equity Funds

Sector Funds

RISKS

R ETUR NS

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 37/77

The above Graph shows the Risk and Returns generated by different Funds. Liquid

Funds are less Risky and also generate less Returns where as Sector Funds are more

Risky but generate more Returns by the example of above two Funds it is clear that

Risk and Returns are directly proportional to each other. Other Funds like Equity

Funds, Balanced Funds and Income Funds are also gives the same percentage of

Returns as the Risk involved.

COMMODITIES:

Commodity Futures are contracts to buy specific quantity of a particular commodity

at a future date. It is similar to the Index futures and Stock Futures but the underlying

happens to be commodities instead of Stocks and Indices.

Major Commodity Exchanges: The Government of India permitted establishment

of National-level Multi-Commodity exchanges in the year 2002 and accordingly three

exchanges come in picture. They are:

• Multi-Commodity Exchange in India Ltd, Mumbai (MCX).

• National Commodity and Derivative Exchange of India, Mumbai (NCDEX).

• National Multi Commodity Exchange, Ahmadabad (NMCE).

However there are regional commodities exchanges functioning all over the country.

India Infoline Commodities Broking Pvt. Ltd has got membership of both the premier

commodity exchanges i.e. MCX and NCDEX.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 38/77

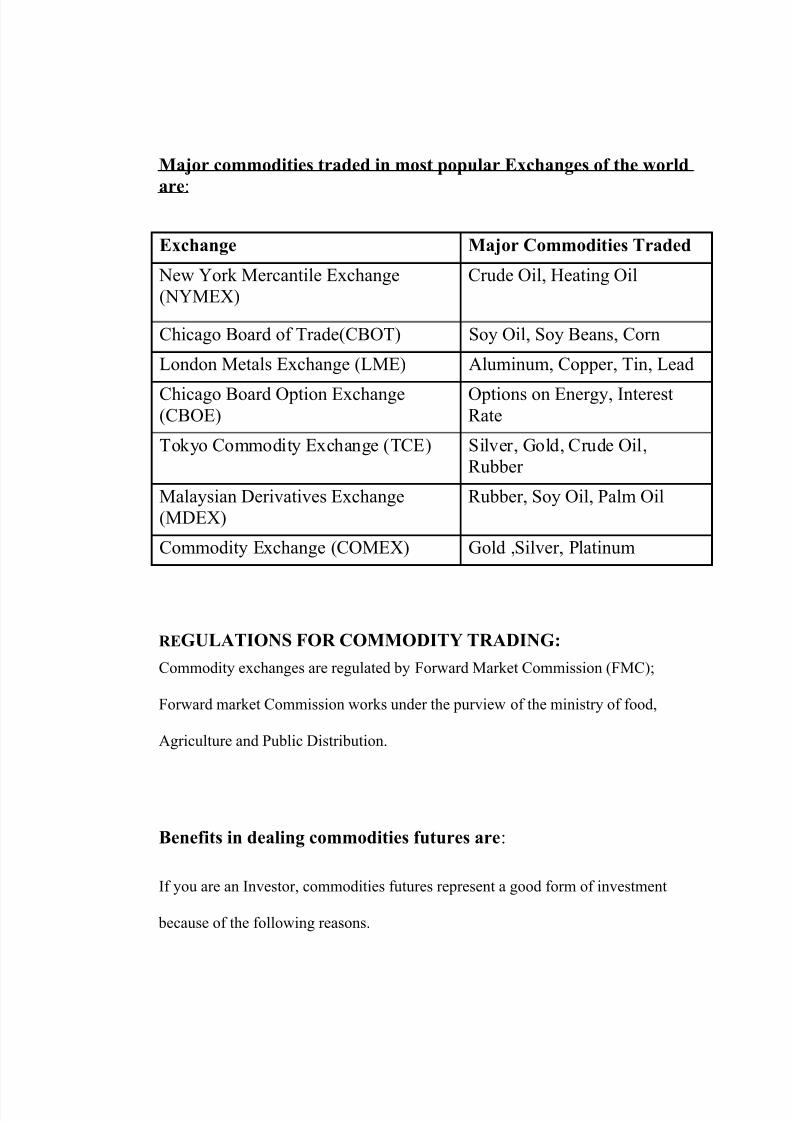

Major commodities traded in most popular Exchanges of the worldare :

Exchange Major Commodities Traded

New York Mercantile Exchange(NYMEX)

Crude Oil, Heating Oil

Chicago Board of Trade(CBOT) Soy Oil, Soy Beans, Corn

London Metals Exchange (LME) Aluminum, Copper, Tin, Lead

Chicago Board Option Exchange(CBOE)

Options on Energy, InterestRate

Tokyo Commodity Exchange (TCE) Silver, Gold, Crude Oil,Rubber

Malaysian Derivatives Exchange(MDEX)

Rubber, Soy Oil, Palm Oil

Commodity Exchange (COMEX) Gold ,Silver, Platinum

RE GULATIONS FOR COMMODITY TRADING:Commodity exchanges are regulated by Forward Market Commission (FMC);

Forward market Commission works under the purview of the ministry of food,

Agriculture and Public Distribution.

Benefits in dealing commodities futures are :

If you are an Investor, commodities futures represent a good form of investment

because of the following reasons.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 39/77

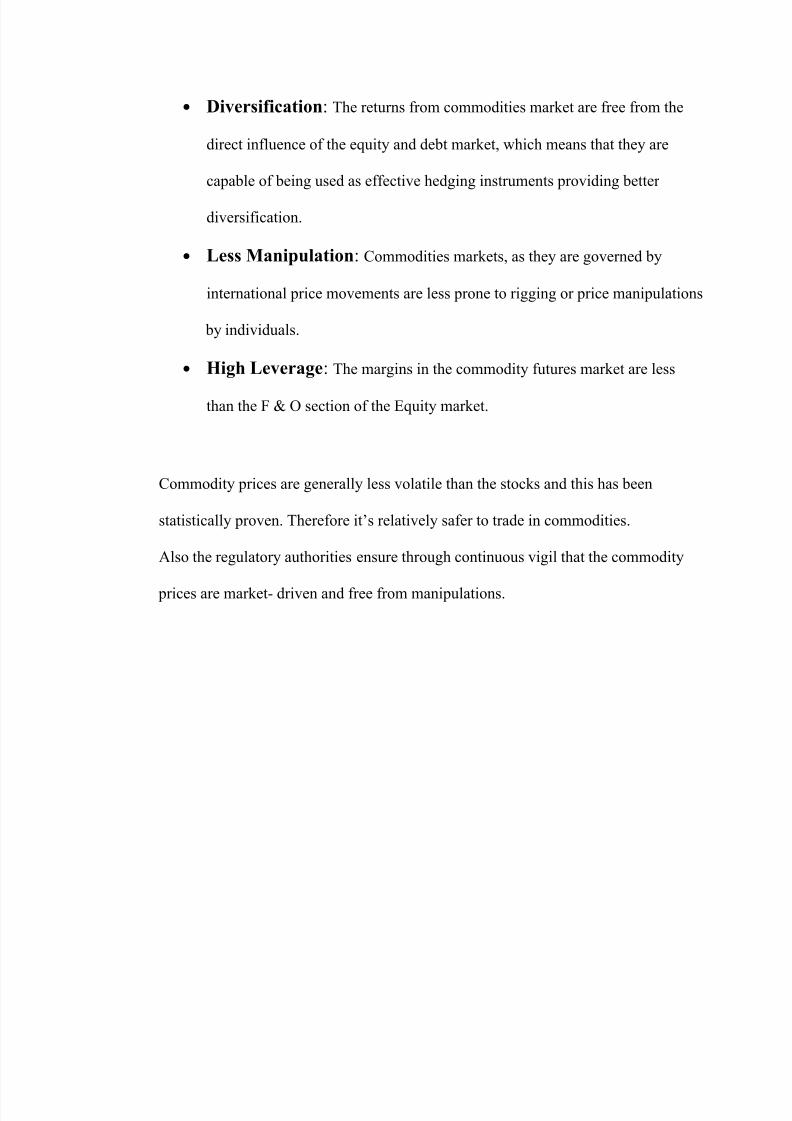

• Diversification : The returns from commodities market are free from the

direct influence of the equity and debt market, which means that they are

capable of being used as effective hedging instruments providing better

diversification.

• Less Manipulation : Commodities markets, as they are governed by

international price movements are less prone to rigging or price manipulations

by individuals.

• High Leverage : The margins in the commodity futures market are less

than the F & O section of the Equity market.

Commodity prices are generally less volatile than the stocks and this has been

statistically proven. Therefore it’s relatively safer to trade in commodities.

Also the regulatory authorities ensure through continuous vigil that the commodity

prices are market- driven and free from manipulations.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 40/77

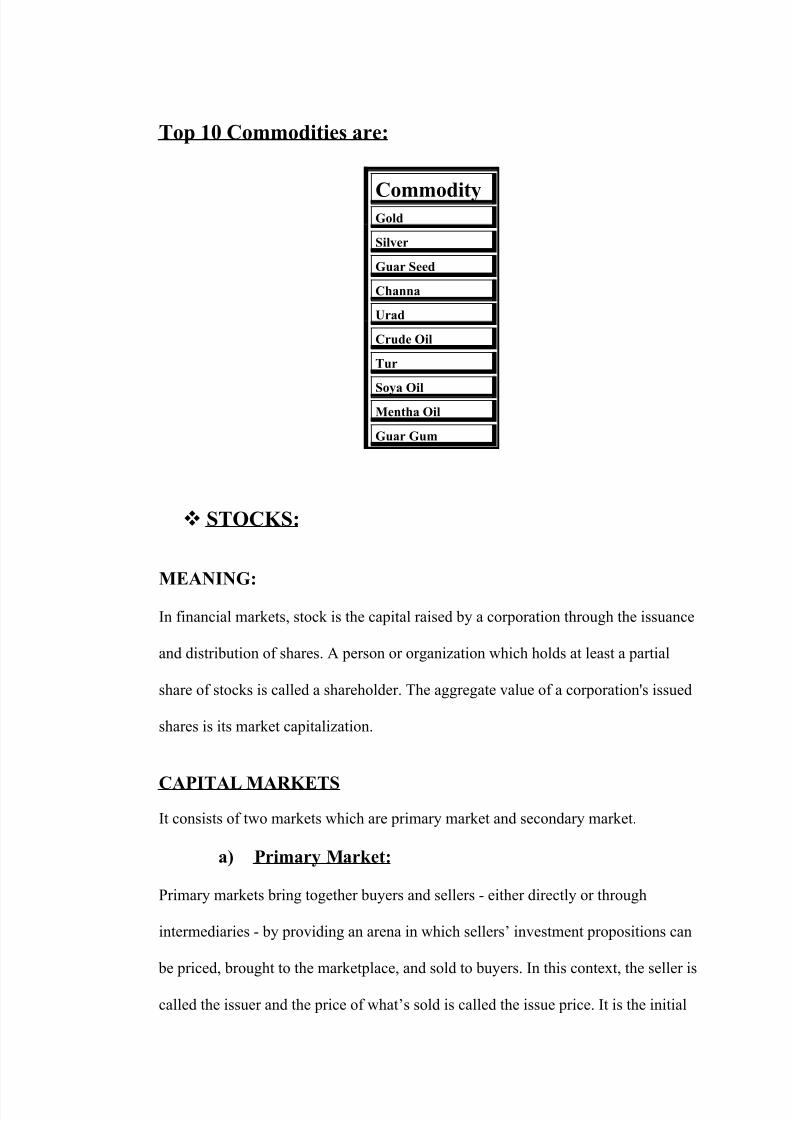

Top 10 Commodities are:

CommodityGold

Silver

Guar Seed

Channa

Urad

Crude Oil

Tur

Soya OilMentha Oil

Guar Gum

STOCKS:

MEANING:

In financial markets, stock is the capital raised by a corporation through the issuance

and distribution of shares. A person or organization which holds at least a partial

share of stocks is called a shareholder. The aggregate value of a corporation's issued

shares is its market capitalization.

CAPITAL MARKETSIt consists of two markets which are primary market and secondary market.

a) Primary Market:

Primary markets bring together buyers and sellers - either directly or through

intermediaries - by providing an arena in which sellers’ investment propositions can

be priced, brought to the marketplace, and sold to buyers. In this context, the seller is

called the issuer and the price of what’s sold is called the issue price. It is the initial

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 41/77

market for any item or service. It also signifies an initial market for a new stock issue.

The jargon also means a firm, trading market held in a security by a trader who

performs the activities of a specialist by being ready to execute orders in that stock.

b) Secondary Markets

Secondary Markets are the stock exchanges and the over-the-counter market.

Securities are first issued as a primary offering to the public. When the securities are

traded from that first holder to another, the issues trade in these secondary markets.

India has 23 stock exchanges that have hubs of financial activities. These stock

exchanges are in following cities: Mumbai, Pune, Ahmadabad, Rajkot, Jaipur, etc.

Stock exchange provides an organized market for transactions in the shares and other

securities. The Bombay Stock Exchange (BSE) and National Stock Exchange

(NSE) together account for nearly 72% of all capital market activity in India.

REAL ESTATE:

Real estate , or immovable property, is a legal term (in some jurisdictions) that

encompasses land along with anything permanently affixed to the land, such as

buildings. Real estate (immovable property) is often considered synonymous with

real property (also sometimes called realty), in contrast with personal property (also

sometimes called chattel or personality). However, for technical purposes, some

people prefer to distinguish real estate, referring to the land and fixtures themselves,

from real property, referring to ownership rights over real estate.

Real estate market is something that is always glowing like the New York City. The

reason being that this market has very rarely seen a downslide. Real estate market in a

common man terms would mean dealing in property which would include purchase

and sale of land and building. It could be both commercial space and residential

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 42/77

property. Commercial space would mean the property that is purchased or occupied

for business purposes by small to large corporate houses. One undeniable reason why

Indian real estate market has been a boom is due to the increasing number of Multi

National Companies thronging the Indian Land. The want for space is always

increasing with government in India giving additional concessions and recognition to

Corporate engaged in building IT parks and commercial complex. The best thing

about real estate business is tha

SOURCES OF RISK

What makes financial asset risky? It is the various sources of risk. The following are

the sources of risk.

1. Interest rate risk:

The risk which arises due to variability in securities returns resulting from

changes in interest rate. This type affects bonds more directly than common

stocks but affects both.

2. Market risk:

The variability in returns resulting from fluctuations in the overall market i.e. the

aggregate stock market is referred to as market risk. All securities are exposed to

market risk, although it has major impact on common stocks.

3. Inflation risk:

A factor which affects all components of a portfolio is purchasing power risk, or

the chance that the purchasing of the invested dollars will decline with uncertain

inflation the real (inflation-adjusted) returns involves risk even if nominal return

is safe.

4. Business risk:

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 43/77

The risk of doing business in a particular industry or environment is called

business risk.

5. Financial risk:

Financial risk is associated with the use of debt financing by companies. Financial

risk involves the concept of financial leverage.

6. Liquidity risk:

Liquidity risk is the risk associated with particular secondary market in which a

security trades. The more uncertainty about the time element and the price

concession, the greater the liquidity risks.

7. Exchanges risk:

It refers to the variability in returns due to currency fluctuations.

8. Country risk:

Country risk is also referred to as political risk. With more investors investing

internationally, both directly and indirectly, the economic stability is to be

considered.Every investor is bound to end up with a sure margin of profit though

the amount of profit may vary based on our bargaining skills and the need of the

buyer. People also engage in speculative business by purchasing barren lands in

under developed areas for a very minimal cost and wait for couple of years till all

necessary infrastructure is developed in that locality and then sell the land at a

huge profit. On the other side residential properties are also on the increase. One

main reason behind this being that the Housing Development Corporation of

India is promoting big Residential Buildings and all banks offer credit to

customers for purchase of property, this way majority of the population will end

up owing a property. And icing on the cake is that the value of the property is

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 44/77

always down to increase and would never decrease as such we would be assured

about our share of profit.

TYPES OF RISK

1) Systematic risk:These are market risks that cannot be diversified away. Interest rates, recessions and

wars are examples of systematic risks.

2) Non systematic risk:

Also known as “specific risk”, this risk is specific to individual stocks and can be

diversified away as you increase the number of stocks in the portfolio. It represents

the component of a stock’s return that not correlated with general market moves.

Total risk = Systematic risk + Non Systematic risk

For minimizing the risk it is necessary to diversify the investments .

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 45/77

CHAPTER 7

PORTFOLIO MANAGEMENT

SERVICES:

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 46/77

PORTFOLIO MANAGEMENT SERVICES

Portfolio management services involve activities that help the investors to arrive at

desired investment goals. A portfolio management service is the process of

organizing and managing businesses or the establishment for the purpose of obtaining

maximum profit. Portfolio management services ensure optimum use of people,

money and other resources. In short, it is the art of optimizing assets and raising the

worth of a portfolio. The major component of the decision process is portfolio

management. After securities have been evaluated an appropriate portfolio should be

selected. It involves managing group of assets (i.e. portfolio) as a unit. The basis of

financial planning process is an asset allocation strategy. Asset allocation is the

distribution of assets among different asset classes, such as stocks, bonds, and cash

equivalent instruments.

The relationship between risk and return is one of the essential concepts to

understand when investing and it is unique for every investor, the personal risk

tolerance could be influenced by current world events, investments experiences- even

your inherited views on saving and investing.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 47/77

ADVANTAGES OF PORTFOLIO MANGEMENTSERVICES

(1) Individually managed accounts: Provides a flexible format for optimizing

returns through effective fund management.

(2) Customized portfolios : Tailor-made investment strategies to suit individual

requirements.

(3) Individually managed accounts: Provides a flexible format for optimizing

returns through better information support/client servicing regular investments

disclosures make the investor feel comfortable and in control of his money.

(4) Supportive tax structure: Tax changes support rise in equity, there is a cut in

capital gains tax on listed equities:

i. NIL for holdings greater than 12 months

ii. 10%(from 30%) for holdings less than 12 months

(5) SEBI regulated: A regulated industry makes the investor feel comfortable with

the investments techniques adapted to optimize returns.

OBJECTIVE BEHIND OFFERING PORTFOLIOMANAGEMET SERVICES

This is my objective behind offering the portfolio management services to the clients

so that I can offer them:

1. Safety of Fund: The investment should be preserved, not be lost and remain

in the returnable position in cash or kind.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 48/77

2. Liquidity: Portfolio must consist if such securities which could be en-cashed

without any difficulty or involvement of time to meet urgent need for funds.

3. Reasonable returns: The investment should earn a reasonable return to

upkeep the declining value of money and must be compatible with the

opportunity cost of money in terms of current income in the form of interest or

dividend.

4. Appreciation in capital: The money invested in portfolio must grow and

result in capital gains.

5. Tax planning: Efficiently portfolio management is concerned with composite

tax planning covering income tax, capital gains tax, wealth tax and gift tax.

6. Minimize risk: Risk avoidance and minimization is very important and are

most important objectives of portfolio management. Portfolio managers must

ensure these objectives by effective investment planning and periodical review

of marketing and economy.

7. Marketability: The investment made in securities should me marketable that

means, the securities must be listed and traded in stock exchange so as to avoid

risk and difficulty in their encashment. Marketability ensures liquidity to the

portfolio.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 49/77

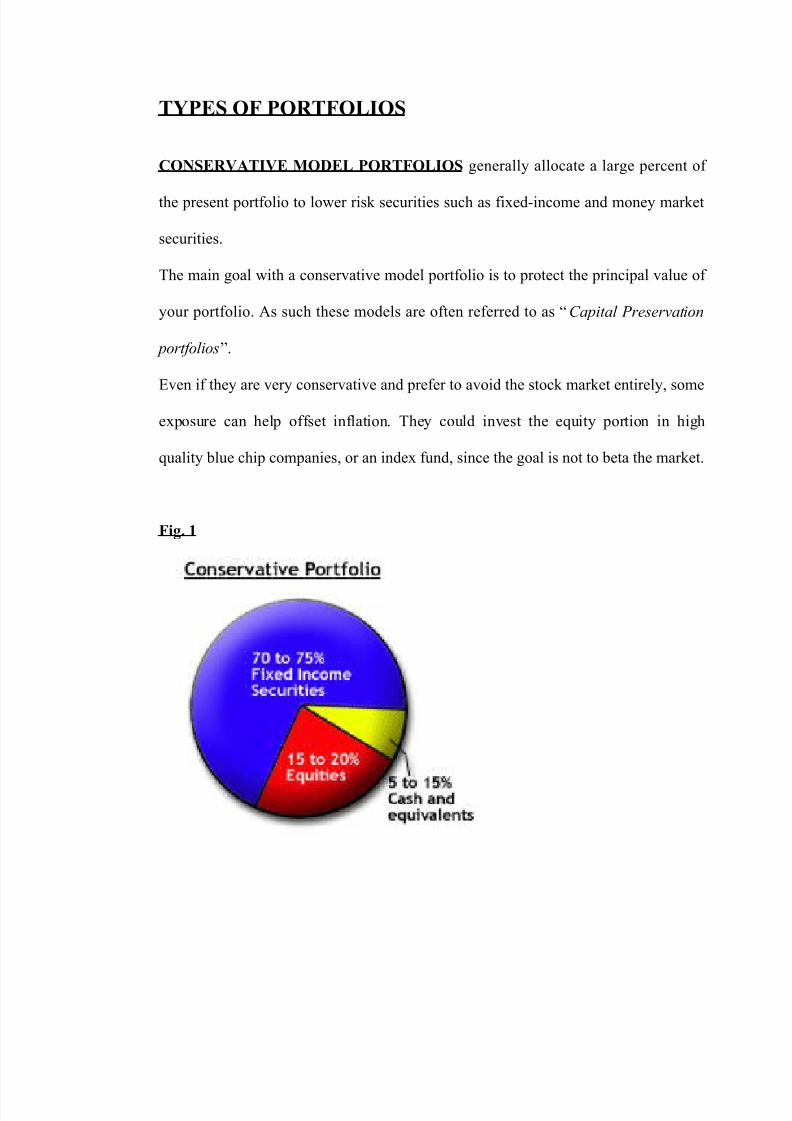

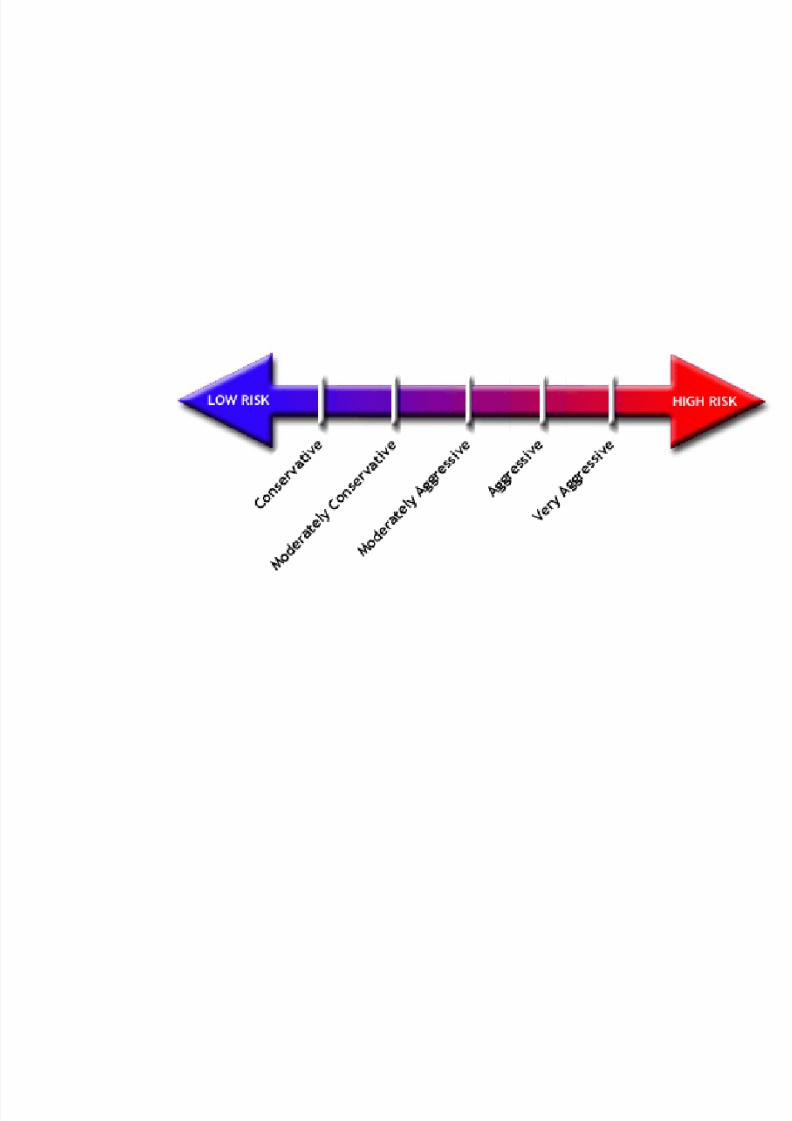

TYPES OF PORTFOLIOS

CONSERVATIVE MODEL PORTFOLIOS generally allocate a large percent of

the present portfolio to lower risk securities such as fixed-income and money market

securities.

The main goal with a conservative model portfolio is to protect the principal value of

your portfolio. As such these models are often referred to as “ Capital Preservation

portfolios ”.

Even if they are very conservative and prefer to avoid the stock market entirely, someexposure can help offset inflation. They could invest the equity portion in high

quality blue chip companies, or an index fund, since the goal is not to beta the market.

Fig. 1

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 50/77

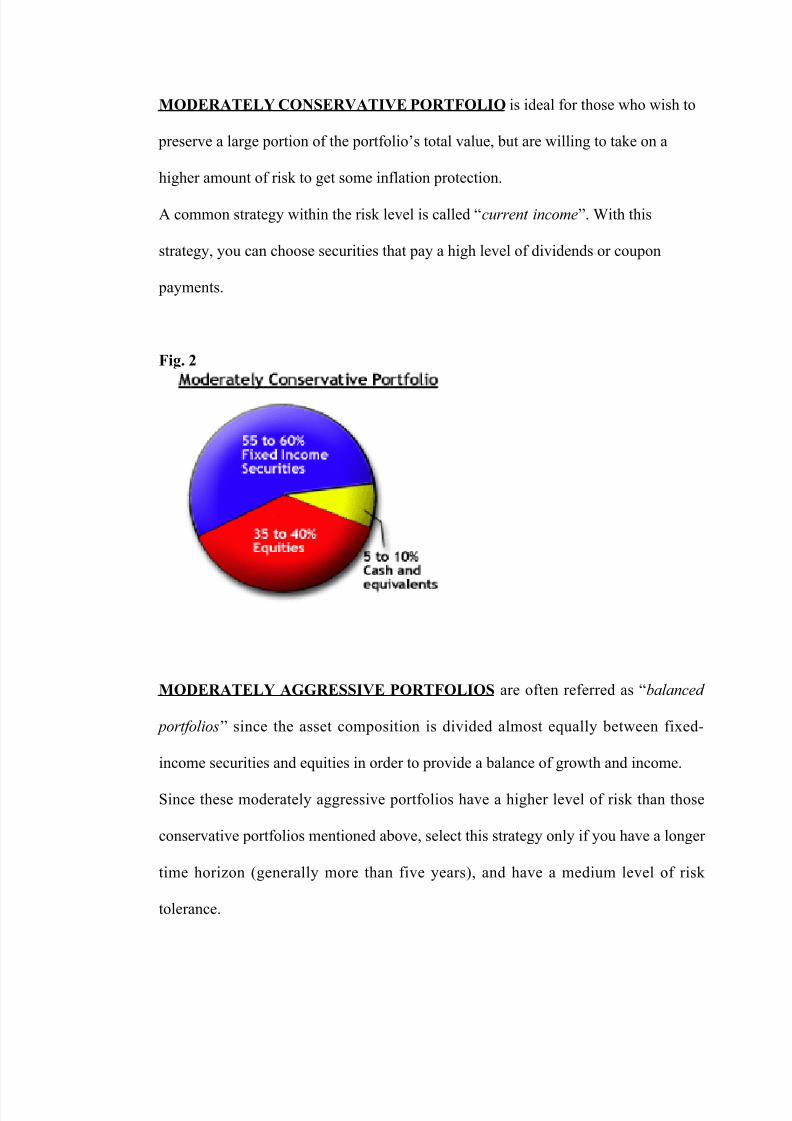

MODERATELY CONSERVATIVE PORTFOLIO is ideal for those who wish to

preserve a large portion of the portfolio’s total value, but are willing to take on a

higher amount of risk to get some inflation protection.

A common strategy within the risk level is called “ current income ”. With this

strategy, you can choose securities that pay a high level of dividends or coupon

payments.

Fig. 2

MODERATELY AGGRESSIVE PORTFOLIOS are often referred as “ balanced

portfolios ” since the asset composition is divided almost equally between fixed-

income securities and equities in order to provide a balance of growth and income.

Since these moderately aggressive portfolios have a higher level of risk than those

conservative portfolios mentioned above, select this strategy only if you have a longer

time horizon (generally more than five years), and have a medium level of risk

tolerance.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 51/77

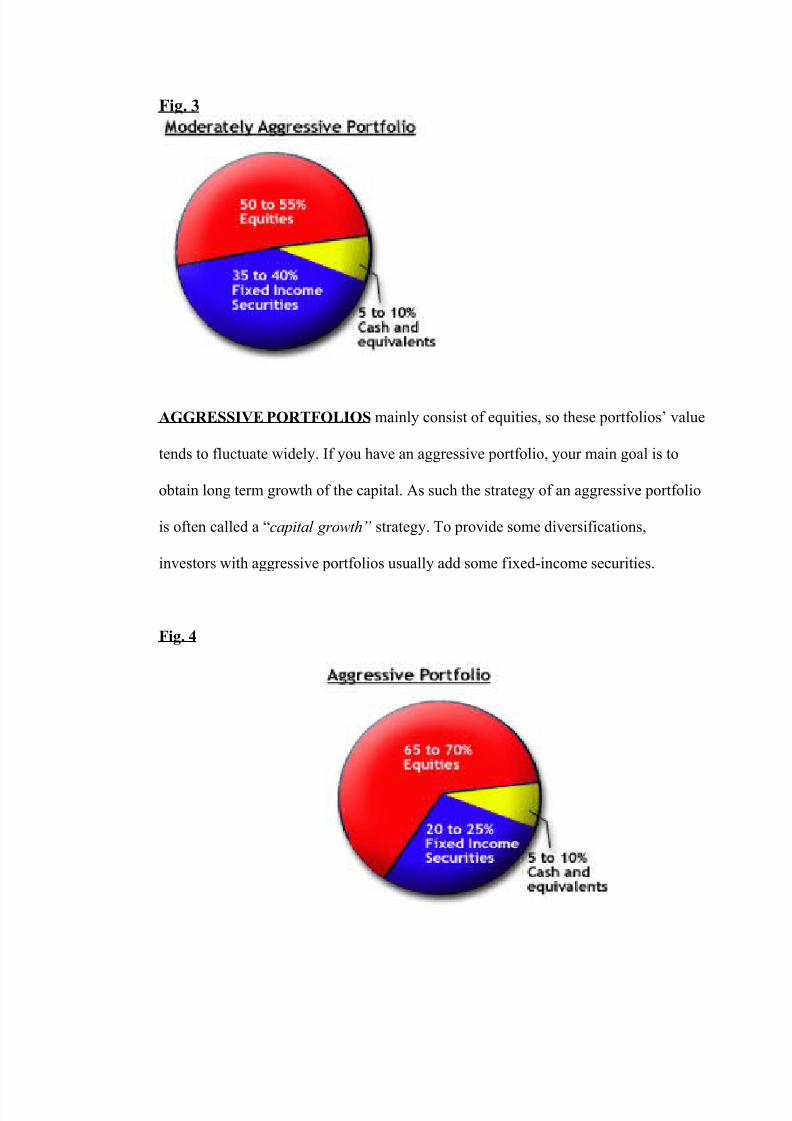

Fig. 3

AGGRESSIVE PORTFOLIOS mainly consist of equities, so these portfolios’ value

tends to fluctuate widely. If you have an aggressive portfolio, your main goal is to

obtain long term growth of the capital. As such the strategy of an aggressive portfolio

is often called a “ capital growth” strategy. To provide some diversifications,

investors with aggressive portfolios usually add some fixed-income securities.

Fig. 4

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 52/77

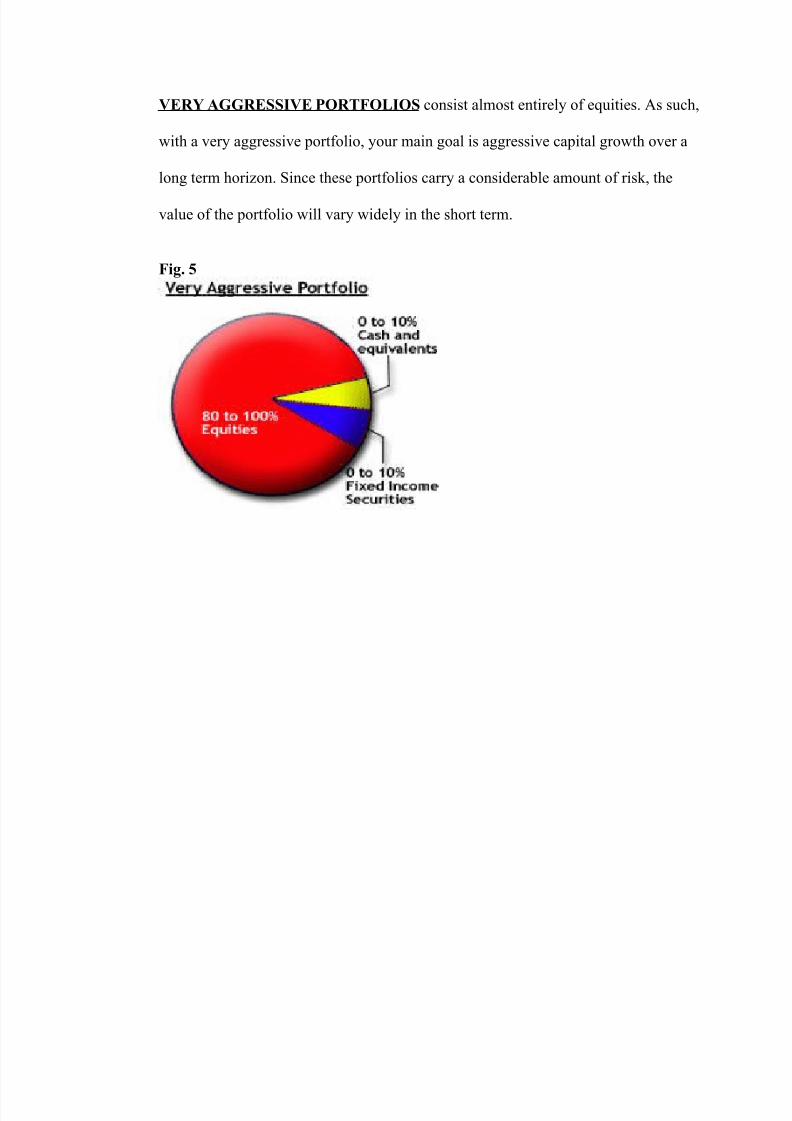

VERY AGGRESSIVE PORTFOLIOS consist almost entirely of equities. As such,

with a very aggressive portfolio, your main goal is aggressive capital growth over a

long term horizon. Since these portfolios carry a considerable amount of risk, the

value of the portfolio will vary widely in the short term.

Fig. 5

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 53/77

RISK APPITITE

Note that the above outline of portfolios and the associated strategies offer only a

loose guideline – Financial advisors modify the above proportions to suit individual

investment needs

Also, the amount of cash and cash equivalents, or money market instruments to be

placed in a portfolio will depend on the amount of liquidity and safety the investor

needs. If they need investments that can be liquidated quickly or they would like to

maintain the current value of your portfolio, they might want to put a larger portion

of their investment portfolio in money market or short-term fixed-income securities.

Those investors who do not have liquidity concerns and have a higher risk tolerance

will have a small portion of their portfolio within these instruments.

As each asset class has varying levels of return for a certain risk, their risk tolerance,

investment objectives, time horizon and available capital will provide the basis for

the asset composition of their portfolio.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 54/77

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 55/77

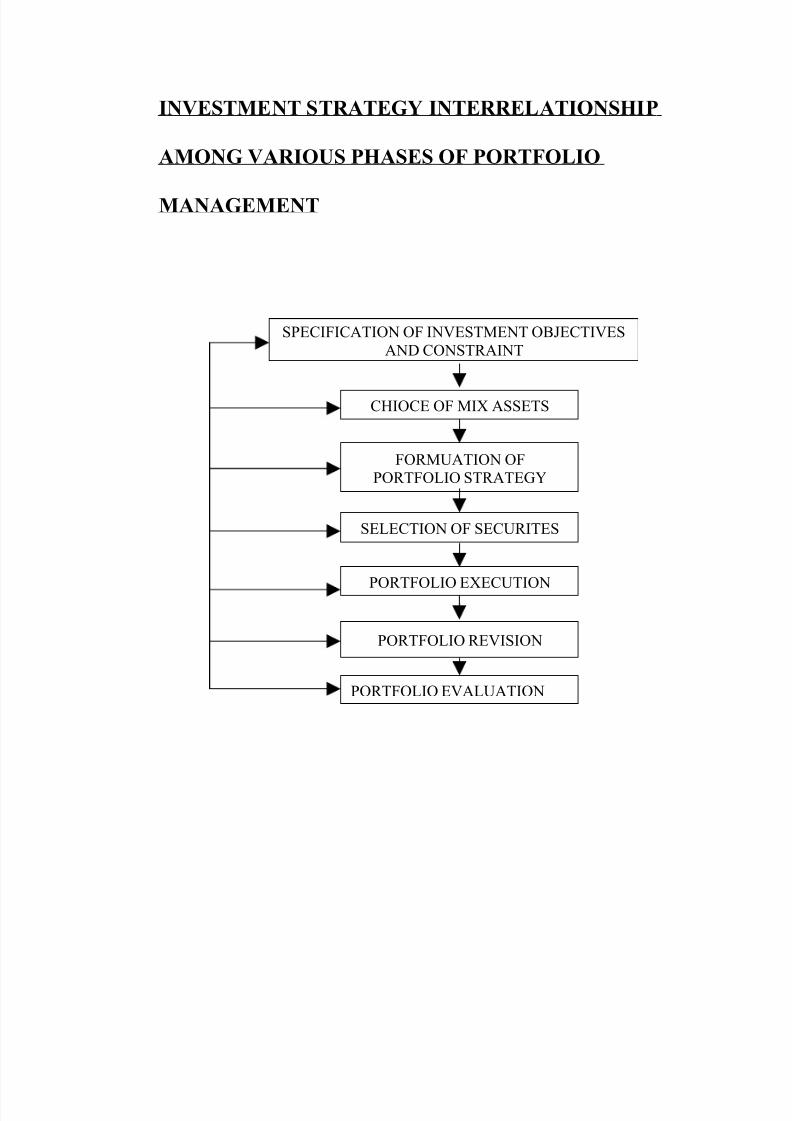

INVESTMENT S TRATEGY INTERRELATIONSHIP

AMONG VARIOUS PHASES OF PORTFOLIO

MANAGEMENT

SPECIFICATION OF INVESTMENT OBJECTIVESAND CONSTRAINT

CHIOCE OF MIX ASSETS

FORMUATION OFPORTFOLIO STRATEGY

SELECTION OF SECURITES

PORTFOLIO EXECUTION

PORTFOLIO REVISION

PORTFOLIO EVALUATION

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 56/77

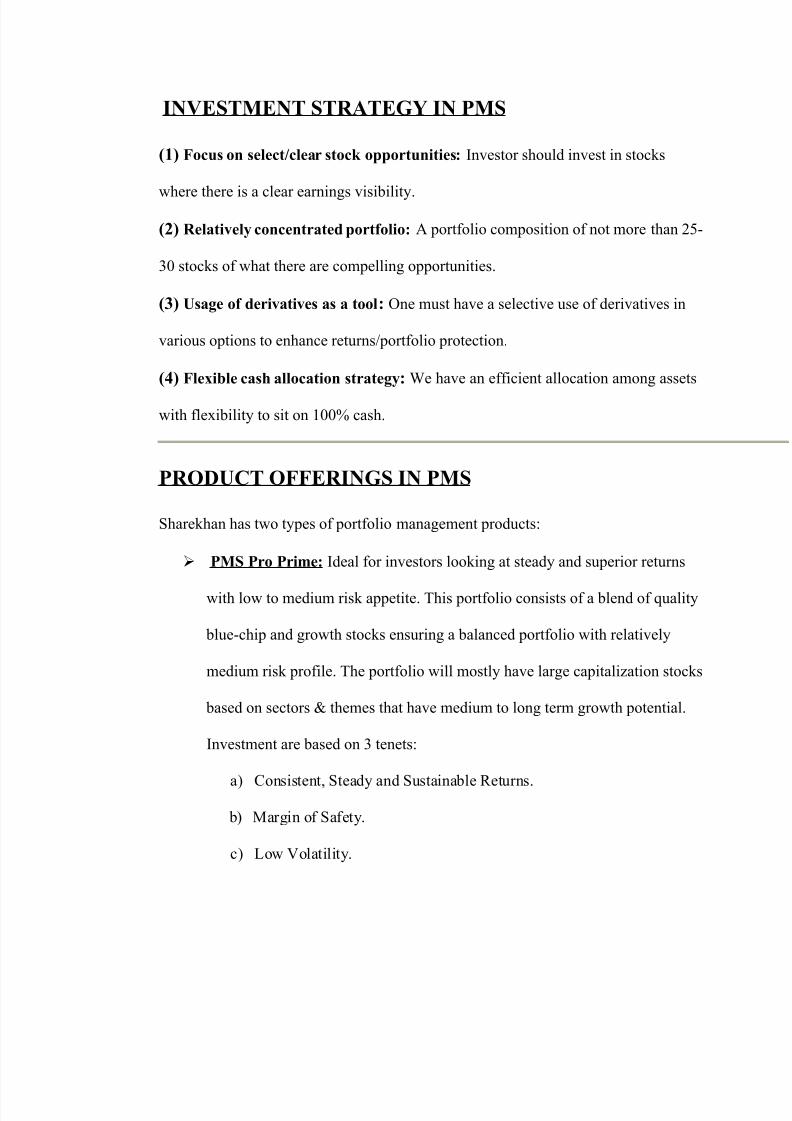

INVESTMENT STRATEGY IN PMS

(1) Focus on select/clear stock opportunities: Investor should invest in stocks

where there is a clear earnings visibility.

(2) Relatively concentrated portfolio: A portfolio composition of not more than 25-

30 stocks of what there are compelling opportunities.

(3) Usage of derivatives as a tool : One must have a selective use of derivatives in

various options to enhance returns/portfolio protection.

(4) Flexible cash allocation strategy : We have an efficient allocation among assets

with flexibility to sit on 100% cash.

PRODUCT OFFERINGS IN PMS

Sharekhan has two types of portfolio management products:

PMS Pro Prime: Ideal for investors looking at steady and superior returns

with low to medium risk appetite. This portfolio consists of a blend of quality

blue-chip and growth stocks ensuring a balanced portfolio with relatively

medium risk profile. The portfolio will mostly have large capitalization stocks

based on sectors & themes that have medium to long term growth potential.

Investment are based on 3 tenets:

a) Consistent, Steady and Sustainable Returns.

b) Margin of Safety.

c) Low Volatility.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 57/77

PMS Pro Tech: These services are for those who want high risk for high

returns.

Pro-tech uses the knowledge of technical analysis and the power of derivatives

market to identify trading opportunities in the market. The Protech lines of

products are designed around various risk/reward/volatility profiles for different

kinds of investment needs.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 58/77

CHAPTER 8:

VIRTUAL PORTFOLIO

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 59/77

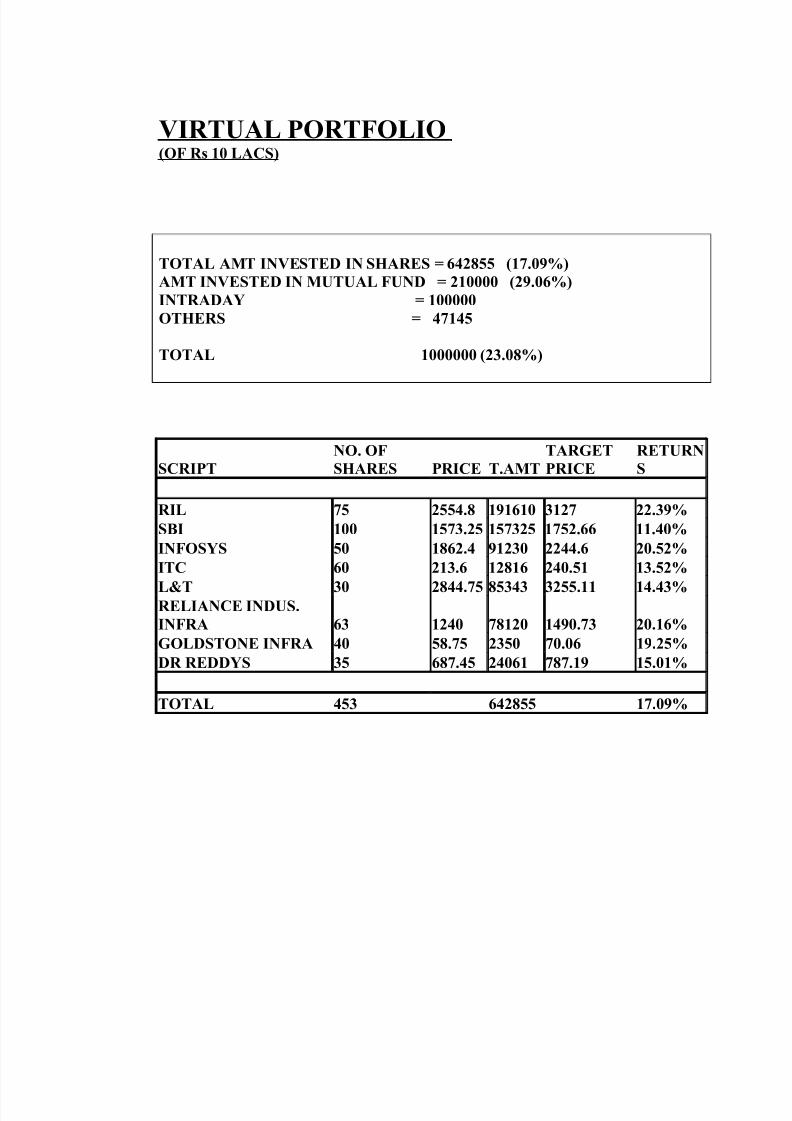

VIRTUAL PORTFOLIO (OF Rs 10 LACS)

TOTAL AMT INVESTED IN SHARES = 642855 (17.09%)AMT INVESTED IN MUTUAL FUND = 210000 (29.06%)INTRADAY = 100000OTHERS = 47145

TOTAL 1000000 (23.08%)

SCRIPTNO. OFSHARES PRICE T.AMT

TARGETPRICE

RETURNS

RIL 75 2554.8 191610 3127 22.39%SBI 100 1573.25 157325 1752.66 11.40%INFOSYS 50 1862.4 91230 2244.6 20.52%ITC 60 213.6 12816 240.51 13.52%

L&T 30 2844.75 85343 3255.11 14.43%RELIANCE INDUS.INFRA 63 1240 78120 1490.73 20.16%GOLDSTONE INFRA 40 58.75 2350 70.06 19.25%DR REDDYS 35 687.45 24061 787.19 15.01% TOTAL 453 642855 17.09%

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 60/77

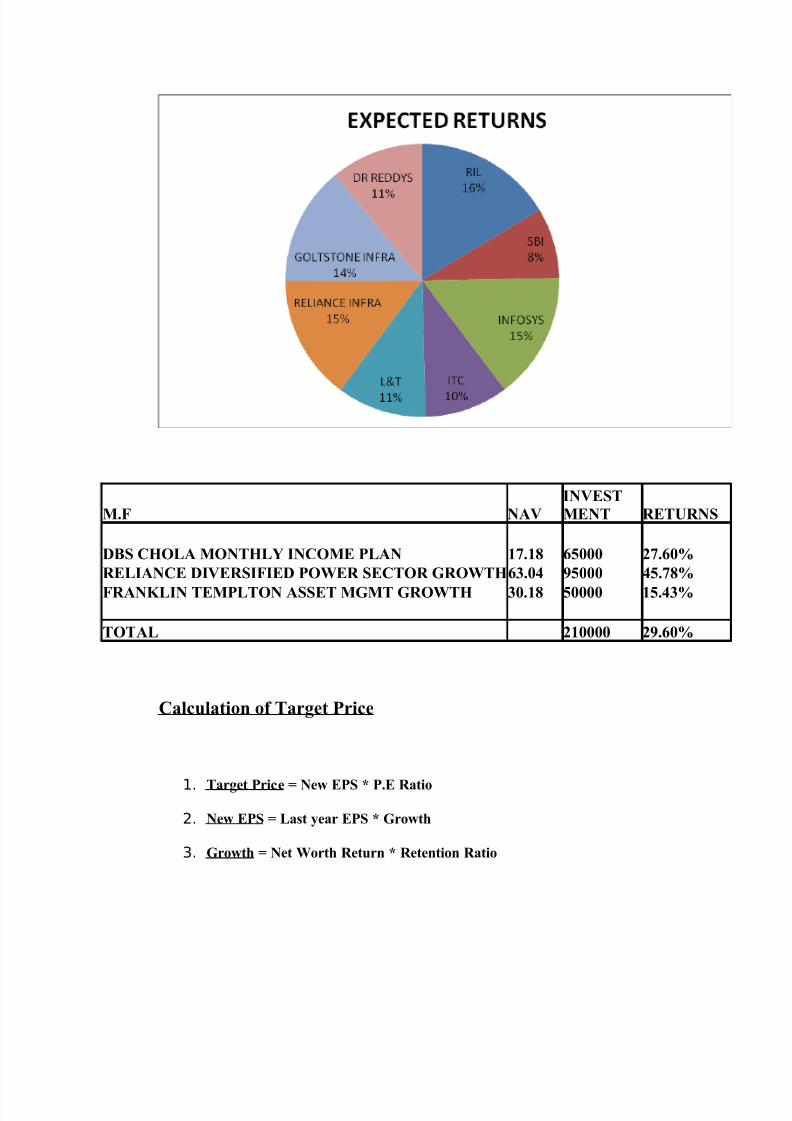

M.F NAVINVESTMENT RETURNS

DBS CHOLA MONTHLY INCOME PLAN 17.18 65000 27.60%RELIANCE DIVERSIFIED POWER SECTOR GROWTH63.04 95000 45.78%FRANKLIN TEMPLTON ASSET MGMT GROWTH 30.18 50000 15.43% TOTAL 210000 29.60%

Calculation of Target Price

1. Target Price = New EPS * P.E Ratio

2. New EPS = Last year EPS * Growth

3. Growth = Net Worth Return * Retention Ratio

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 61/77

CHAPTER 9:

FINDINGS

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 62/77

FINDINGS

A summer project brings the student face to face with the real corporate world. This

is the time when one learns what the industry practices are and do the practices really

follow what is really taught in the classroom. Further it gives an excellent chance to

the students to apply the concepts in the real world.

Application on tools and techniques in the real world

Summer training provided me a good opportunity to apply the concepts, tools and

techniques in the real business-life situations.

Main Learning’s;

Having worked with India Infoline, I have experienced and realized the importance of

operating the Demat account online; trading the shares online; how market operates,

etc. The main thing I learned is that how a portfolio is managed and how the money

should be invested in different assets.

I learned how to study a portfolio and also came to know the difficulties in preparing

and handling a portfolio.

Interaction with superiors and discussing problems, both project based as well as

others, gave me a chance to learn quite a lot. There are many small things which on

the face of it look small but have great value in the long run. I have learnt a lot and I

am confident and sure that this will help me in my future.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 63/77

CHAPTER 10:

SUGGESTIONS

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 64/77

SUGGESTIONS

• India Infoline’s advertising is done mainly through word of mouth and IPO

releases, which attracts only a fraction of the investors and thereby bringing

down its market capitalization. India Infoline, like the other leading brokerage

firms should indulge in a more aggressive form of advertising in both print

and electronic media if it looks to keep pace with the cut throat competition in

the years to come.

• Organize and make accessible a database of customer information.

• Allocating marketing investment according to customer value.

• The portfolio manager has to very carefully analyze the market and then

invest in different assets.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 65/77

CHAPTER 11:

LIMITATIONS

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 66/77

LIMITATIONS OF THE STUDY:

The main limitation of my study is from the investor side, as for providing them

the PMS I need to know their past investments in detail which they hesitate to

disclose as they find it hard to trust anyone regarding their investments, so I have

to first built up the trust & then talk about the investments, as the main limitation

is time so it takes me at least few days for this procedure through regular visits &

follow up’s.

Time period undertaken for the project was also one of the limiting factors as

“Portfolio Management” is such a vast subject which involves in-depth study

analysis. As a portfolio has to be diversified keeping in mind the risk appetite of

the investor as well as keeping a track record of his past investments and then

finally analyzing the portfolio & for this the proposed time period was a limiting

factor.

The sample size taken for drawing a conclusion is too small to get an accurate

result & is only small portion of actual population.

Changing the mentality of people for investing through a particular Advisory

Services.

It’s hard to change the typical psychological mindset of the investor, limiting the

options available, although feasible.

Difficult to overcome investors who wants return in less time & at times it’s

difficult to get the documents required for formalities from investors.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 67/77

Another very important limitation while doing this project which I came across was

that the investors find it hard to trust the products & services offered by the private

companies even though they are performing much better than the government

companies like LIC v/s Private Players (ICICI, Reliance, Met Life…..)

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 68/77

CHAPTER 12:

CONCLUSION

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 69/77

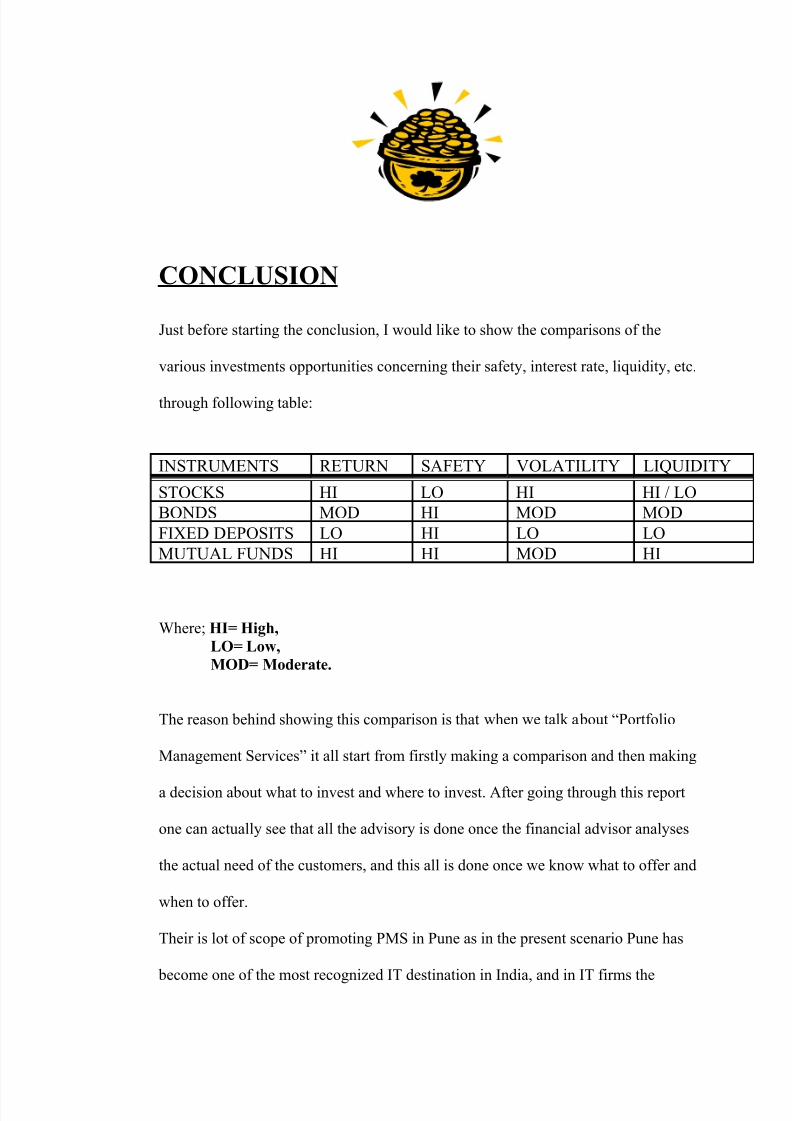

CONCLUSION

Just before starting the conclusion, I would like to show the comparisons of the

various investments opportunities concerning their safety, interest rate, liquidity, etc.

through following table:

Where; HI= High,LO= Low,MOD= Moderate.

The reason behind showing this comparison is that when we talk about “Portfolio

Management Services” it all start from firstly making a comparison and then making

a decision about what to invest and where to invest. After going through this report

one can actually see that all the advisory is done once the financial advisor analyses

the actual need of the customers, and this all is done once we know what to offer and

when to offer.

Their is lot of scope of promoting PMS in Pune as in the present scenario Pune has

become one of the most recognized IT destination in India, and in IT firms the

INSTRUMENTS RETURN SAFETY VOLATILITY LIQUIDITY

STOCKS HI LO HI HI / LOBONDS MOD HI MOD MODFIXED DEPOSITS LO HI LO LOMUTUAL FUNDS HI HI MOD HI

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 70/77

Investors are not well versed with the various investment avenues present in the

market. They always seek for financial help for their “Tax Planning’s” and for good

“Capital Appreciations” as the annual packages offered to them are quite high so they

need to plan accordingly & that is the right time when we come into the picture, with

best of the PMS which we can offer.

There is great opportunity for Mutual Fund companies as there is a rise in number of

people who want to invest in share market but don’t have time and knowledge to do

so, also these people want to take less risk .With booming market and falling interest

rate of bank deposits, people see mutual funds as an attractive financial tool which

provide a high return rate at lower risk as compared to equity market. Young people

these days are particularly more interested in mutual funds because they see mutual

fund as safe bet. Also these people have large disposable incomes and risk taking

capability too. Advertising can also play a major part as it has been seen that people

buy mutual fund looking at the brand name. While offering them the “Portfolio

Management Services” we see that we offer them the best after carrying out the total

analysis on various schemes running in the market we give them what satisfies their

need the most efficiently. As far as the investment sector is considered, a sharp rise in

the no. of woman a/c holders, with almost 21% of its total 6.53 lakh trading a/c held

by woman, the organization have to concentrate on woman segment. According to the

respondents the quality of the service is very important. So the company should

project itself as a brand in the market that gives end user the best quality of service

with handy operations. Also most of the respondents have their personal consultant or

company consultants, India Infoline have to differentiate their services from other

consultant effectively by delivering value added services to its customers. Also

organizations have to concentrate on direct marketing activities. The consultancy

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 71/77

should develop its long term relationship with the customers. The consultancy must

give much more emphasis on creation of customer who make repurchase.

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 72/77

CHAPTER 13:

BIBLIOGRAPHY

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 73/77

BIBLIOGRAPHY:

Books:

Prasana Chandra: P (2004) “Investment analysis & portfoliomanagement”Tata Mc Graw Hill (New Delhi).

Websites:

www.india infoline.com

www.nseindia.com

www.bseindia.com

http://www.amfiindia.com/showhtml.asp?page=mfconcept#B

http://www.moneycontrol.com/bestportfolio/wealth-management-tool/09/58/investments

http://en.wikipedia.org/wiki/Mutual_fund#Types_of_mutual_funds

www.valueresearchonline.com

www.personalfn.com

www.rediffmail.com

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 74/77

CHAPTER 14:

ANNEXURE

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 75/77

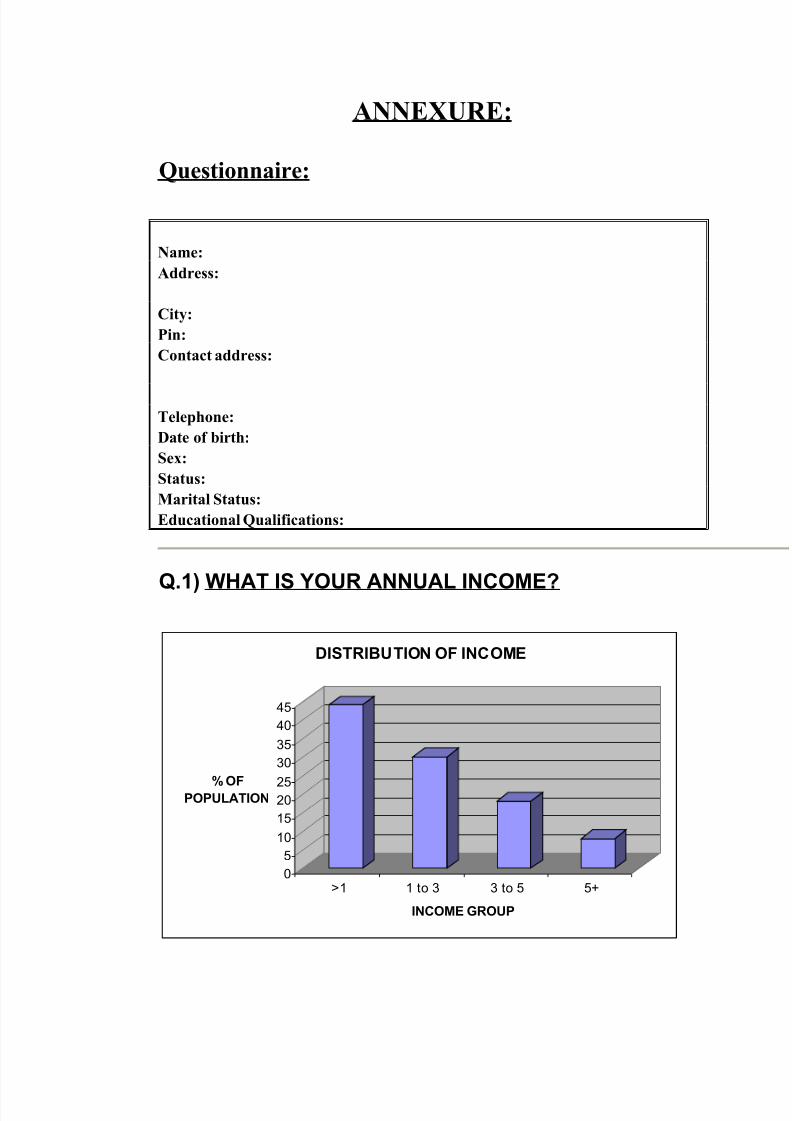

ANNEXURE:

Questionnaire:

Name:Address: City:Pin:Contact address:

Telephone:Date of birth:Sex:Status:Marital Status:Educational Qualifications:

Q.1) WHAT IS YOUR ANNUAL INCOME?

0

5

10

15

2025

30

35

40

45

% OFPOPULATION

>1 1 to 3 3 to 5 5+

INCOME GROUP

DISTRIBUTION OF INCOME

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 76/77

Maximum number of sample population has income below 1 lakh followed by 1- 3

lakh. Normally people having income below 1 lakh do not invest so our target

population is people having income above 1 lakh.

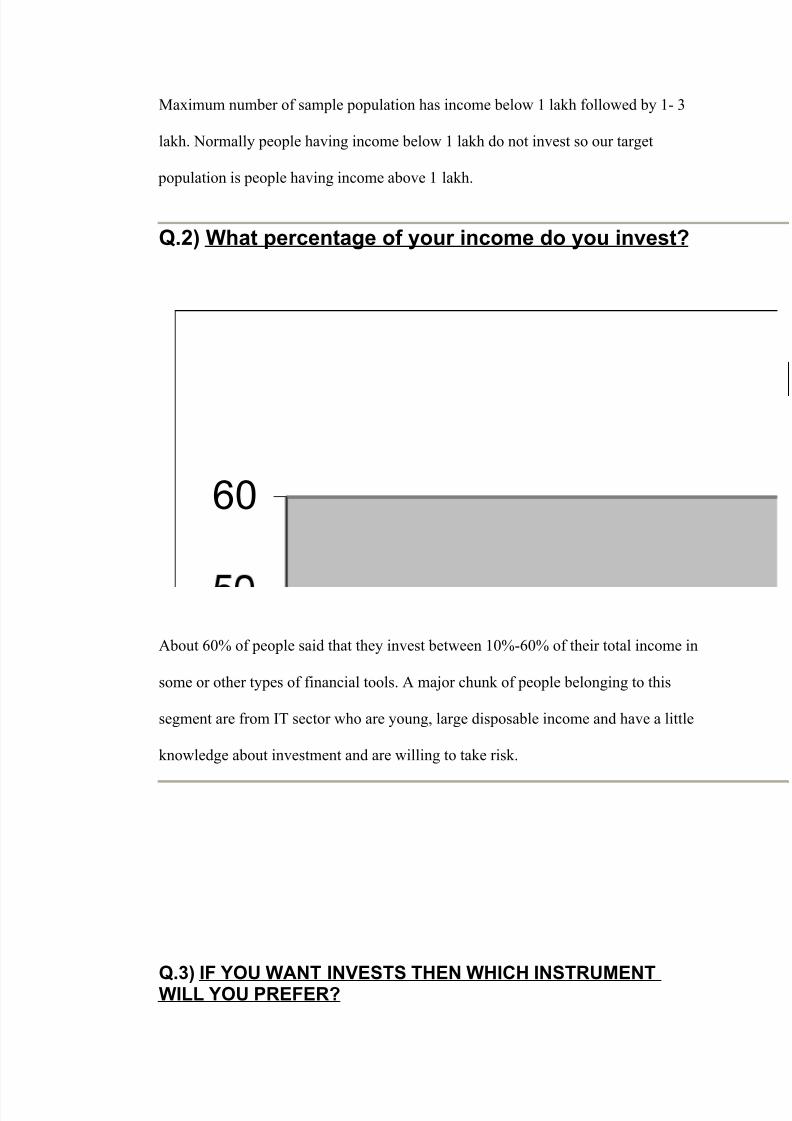

Q.2) What percentage of your income do you invest?

About 60% of people said that they invest between 10%-60% of their total income in

some or other types of financial tools. A major chunk of people belonging to this

segment are from IT sector who are young, large disposable income and have a little

knowledge about investment and are willing to take risk.

Q.3) IF YOU WANT INVESTS THEN WHICH INSTRUMENTWILL YOU PREFER?

60

8/8/2019 jyoti paryani

http://slidepdf.com/reader/full/jyoti-paryani 77/77

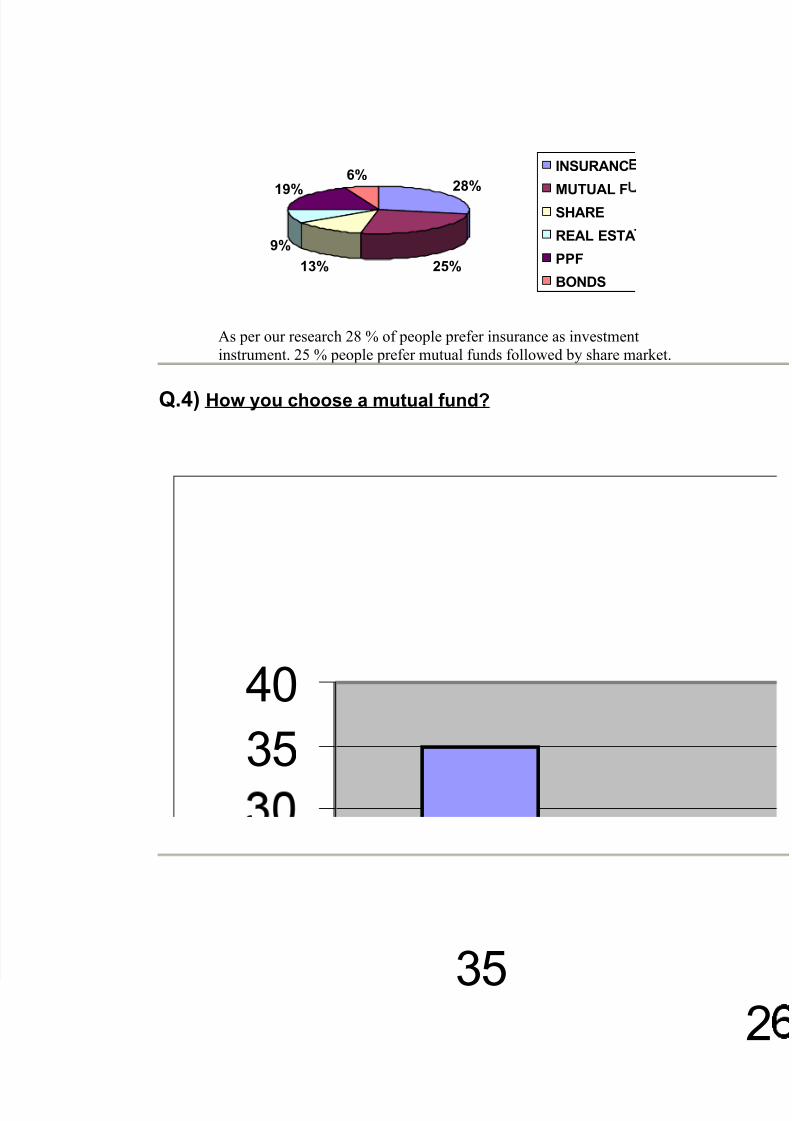

28%

25%13%9%

19%

6%INSURANC

MUTUAL FSHARE

REAL ESTA

PPF

BONDS

As per our research 28 % of people prefer insurance as investmentinstrument. 25 % people prefer mutual funds followed by share market.

Q.4) How you choose a mutual fund?

35

40