sm presentation_akash sarkar

TRANSCRIPT

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 1/61

Sector : Storage BatteryIndustry

Company : ExideIndustriesSubmitted by :Akash Sarkar(13004)

Surya Narayana Adiga(13048)Nirupam Mandal(13025)

Pathan Javed(13026)Ajvad Rehmani(13003)

Shahab Khan(13040)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 2/61

All market sizes and segments are for organized segment only

Storage BatteryIndustry(Contd..)

•

• The Indian storage battery is in the growth stage. Theindustry has grown more than 125% from 2005-06 to2009-10. Per capita battery market in India is almost1/10th of global average. This is proved from the factthat the battery use per capita in India is around 1.6 $ /per annum as against a world average of 10.1 $ / perannum and US consumption of 48.7 $ / per annum.Therefore, sustained economic growth would drive thebattery demand in India.

•

• Although, domestic production of batteries is growing at ahealthy pace, it is not sufficient to meet the aggregatedemand. India relies heavily on imports. Importsaccounts for nearly 40-50 % of domestic supply. Importshave grown by 20.6 % in 2009-10 and is likely to grow by17.6% in

2010-11.

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 3/61

All market sizes and segments are for organized segment only

Storage Battery Industry•• There are strict pollution control and regulatory norms,

especially with regard to recycling of toxic wastes suchas Lead. There are long approval processes. Theunorganised players in the replacement segment

therefore has to follow these norms to sustain theirbusiness. This also acts as an entry barrier.•

• Exide is the market leader in batteries with a strong brandequity and widest distribution.

•• Production of batteries grew by 18.3% in 2009-10. A

healthy growth in production was driven by higherdemand for batteries from automobile and industrialsegment. This will lead to 15% rise in production of

batteries in 2010-11.

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 4/61

All market sizes and segments are for organized segment only

Storage BatteryIndustry(Contd..)

•• Storage battery industry of India for OEM segment is mostly

organized. For eg Exide and Amara Raja accounts for more than95% market share for automobile OEM segment.

•• The replacement market is fragmented . The unorganized players

make up about 55% of the market, while the organized playersaccount for the remaining 45% of the market. The market share forthe organized players was 30% in this segment 4 years before.

•

Reasons for fragmentation :•

• Low entry barrier in replacement market as law allows recycling of lead. So small players collect used batteries and recycle them tosell in the market.

•• Cost structure in replacement market of unorganized players is 20-

25% less. The reason behind this is that unorganized players don’thave R & D, branding and channel margin expenses.S

•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 5/61

All market sizes and segments are for organized segment only

Storage BatteryIndustry(Contd..)

• Lead accounts for 75 % of all raw material costs. During 2008-09, leadprices peaked at US$2,823 per tonne in April 2008 andUSD 2,368per tonne in January 2010. Lead cost also accounts for 55-65% of sales.

•

• The industry is expected to face pricing pressure from the userindustry during the year 2010. Consequently, companies areunlikely to completely pass on the burden of rise in price of lead(major raw material). This is expected to lead to a faster rise in rawmaterial cost as compared to income. Operating profit margin,therefore, is expected to contract by 1.4 percentage points to 20.7per cent during the year. However, net margin is likely to fall byonly 0.8 percentage points to 11.7 per cent. A slower rise ininterest expense is expected to restrict the fall in net margin duringthe year.

•

• Automobiles and back up power supply equipments are some of thelarge users of wet lead acid batteries. Depending on the type of battery, it has to be replaced almost every 3-4 years. Hence the

replacement market for batteries is bigger than the OE market.Apart from the organised, branded battery manufacturers, the

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 6/61

All market sizes and segments are for organized segment only

Current Market Size

C u rre n t m a rke t size o f th e b a tte ry in d u stry co n sid erin g-un orga nized could be an yw he re arou nd R s 170 00 18 00 0

.cro re

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 7/61

All market sizes and segments are for organized segment only

Future size and growth of industry

• Net sales of storage batteries industry to rise by22.5% in 2010-11.Market size is expected toreach Rs.12,870 crores in 2010-11.

•

• The growth will be mostly driven by automobilesegment and a steady growth in the industrialsegment.

•

•

•

•

•

•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 8/61

All market sizes and segments are for organized segment only

• The growth will be driven by :

•Automobile segment :a) The passenger car market in India is expected to grow by 12%

annually over the next five years which in effect wouldtranslate to more than 100% growth for the domestic batteryindustry during this period.

b)c) India’s low passenger vehicle and two-wheeler penetration per

1,000 people at 11 and 66 represent an opportunity.d)e) The Indian automobile industry expects to invest up to Rs. 80,000

crore in fresh capacity in four years and car manufacturingcapacity is set to rise to 57 lakh units by 2015, according toErnst & Young, as the industry sustains a 10-15% CAGR.

f)

O p p o rtu n itie s o f g ro w th

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 9/61

All market sizes and segments are for organized segment only

Opportunities of growth• Industry segment :•

a) Infrastructure development is a key focus area for theGovernment and in the Union Budget 2010-11 anamount of Rs 1,73,555 crores has been allocated for thissector which is 46% of the total plan allocation. Thishuge spending on infrastructure by the Governmentcoupled with plans for modernization of railways andsetting up of nuclear power plants etc. would augur wellfor the battery industry.

b)c) India’s per capita power consumption was low at 704 kwh in

2008-09 against a global average of 2,800 kwh. Revisedthe incremental power capacity target from 78,577 MWto 92,700 MW during the Eleventh Plan (2007-12) withthe objective of raising per capita consumption to 1,000

kwh by 2012.•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 10/61

All market sizes and segments are for organized segment only

Opportunities of growth

d) The government’s priority is to expand pan-India railwayconnectivity and modernise its facilities with anestimated Rs. 2,000 billion investment in the EleventhPlan.

e) According to Gartner, India’s IT end-user spending isexpected to grow at a CAGR of 14.8% (2007-12),generating USD 110 billion in business potential in2012.

f)g) IT and IT-es industry to reach USD 175 billion in revenue by

2020 and the domestic component could touch USD 50billion by 2020.

h)

i) Mounting power deficits particularly in India will open upthe need for backup batteries in critical equipment and

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 11/61

All market sizes and segments are for organized segment only

Opportunities of growthTelecom Segment :•

§ With the launch of 3G services in India there will lot of investments needed the number of 3G-enabled handsets

will reach 395 million by end of 2013.a)b) Indian’s mobile subscriber base is set to exceed 771 million

connections by 2013, growing at a CAGR of 14.3% in thesame period from 452 million in 2009.

c)d) India currently has around 350,000 telecom towers which

will provide enough replacement demand for batteries.•

•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 12/61

All market sizes and segments are for organized segment only

Threats to storage batteryindustry

§ Volatility in Lead prices- . Prices of Lead, which is a majorconstituent of batteries, are extremely volatile. Thisvolatility not only creates uncertainty on procurement of the material but also has a major impact on themanufacturing cost of the products. During 2008-09, leadprices peaked at US$2,823 per tonne in April 2008andUSD 2,368 per tonne in January 2010

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 13/61

All market sizes and segments are for organized segment only

Threats to storage batteryindustry

•

§ High market share with unorganized sector:The unorganized sector accounts for a largeproportion of the automotive replacementbattery segment(almost 55%) and thesecompanies sell batteries at low prices.

§

§ Threat from cheap imports : Imports pose a

significant threat to Indian batterymanufacturers and could impact sales in thereplacement market. Cheap imports, mainlyfrom China, for industrial batteries continueunabated and has seen a recent spurt after theindustrial slow down .The price differential forimported batteries is about 20%.

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 14/61

All market sizes and segments are for organized segment only

Segmentation

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 15/61

All market sizes and segments are for organized segment only

Current Capacity Scenario

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 16/61

All market sizes and segments are for organized segment only

Future capacity scenario

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 17/61

All market sizes and segments are for organized segment only

Future capacity scenario• Storage batteries industry to achieve 12-14.5% production

growth during 2010-13•

• The reasons for such growth in production are :

•a) The demand is expected to be largely driven by OEM

battery segment , which is expected to grow by 14-15%.b) A healthy rise in demand from automotive segment is also

expected to support the growth.

c) The industrial segment is likely to grow at a relativelyslower but a healthy pace of 9-10% during the period.

•

•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 18/61

All market sizes and segments are for organized segment only

Critical Success Factor• Sourcing of raw materials for example lead and zinc is the most

important critical success factor.•• More than 75% of lead demand of battery manufacturers are met by

import from other countries.

•• e.g. of what companies are doing :•

a) Exide has acquired two lead recycling smelters namely Leadage Alloys(51%) and Chloride Metals (100%) in FY 09. Recently the companyhas increased its stake in Leadage Alloys to 100%. Due to

sourcing of lead from their own recycling smelters, Exide is able tobuy lead at cheaper costs, i.e. at 8-16% cheaper than the marketrates.

b)c) Amara Raja entered into a Lead supply agreement for almost 100% of

the estimated quantity as per the business plan. The Company

sources Lead from Korea ,Australia and also from Indiancompanies, an adequate geographic de risking.

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 19/61

All market sizes and segments are for organized segment only

Regulations

• In response to concerns about lead poisoning, the CentralGovernment of India, Ministry of Environment and Forests,promulgated “The Batteries (Management and Handling) Rules,2001”. Under this act battery manufacturers are required tocollect 90% of their sales volume.

•

• In May 2010 “The Batteries (Management and Handling) Ruleswere amended, where it was made mandatory for allcompanies to report employees’ blood lead samples every sixmonths.

•

•Lead prices have been highly volatile varying between US$ 1000to US$3200 in the last 2 years. Lead accounts for almost 60%

of the cost of sales. So any hike in the tax rates are going todirectly affect the margins. In the Union Budget of 2010 therehave been two changes :Hike in excise duty from 8% to 10%and MAT has been increased to 18% of book profits from

existing 15%.•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 20/61

All market sizes and segments are for organized segment only

• Exide was incorporated as Associated Battery Makers(Eastern) Ltd., on 31st January, 1947 under theCompanies Act, 1913 to purchase all or any of theassets of the business of manufacturers, buyers andsellers of and dealers in and repairers of electricaland chemical appliances and goods carried on by theChloride Electric Storage Company (India) Ltd, inIndia.

•• The name of the Company was changed to Chloride

India Ltd on 2nd August, 1972.

•• The name of the Company was again changed to

Chloride Industries Ltd. vide fresh Certificate of

About the Company(EXIDE)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 21/61

All market sizes and segments are for organized segment only

• The name of the Company was further changed to ExideIndustries Ltd. on 25th August, 1995.

• The Company manufactures the widest range of storagebatteries in the world from 2.5 Ah to 20,400 Ah capacity,

covering the broadest spectrum of applications.• The Company has six factories strategically located acrossthe country – two in Maharashtra, one in West Bengal,two in Tamil Nadu and one in Haryana.

• The Company’s predecessor carried on their operations as

import house from 1916 under the name ChlorideElectrical Storage Company. Thereafter, the Companystarted manufacturing storage batteries in the countryand have grown to become one of the largestmanufacturer and exporter of batteries in the sub-continent today.

About the Company(EXIDE)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 22/61

All market sizes and segments are for organized segment only

• Exide separated from its UK-based parent,Chloride Group Plc., in 1989, after the latterdivested its ownership in favour of a group of Indian shareholders.

•

• The Company has grown steadily, modernized itsmanufacturing processes and taken initiativeson the service front.

About the Company(EXIDE)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 23/61

All market sizes and segments are for organized segment only

History of events

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 24/61

All market sizes and segments are for organized segment only

History (Contd)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 25/61

All market sizes and segments are for organized segment only

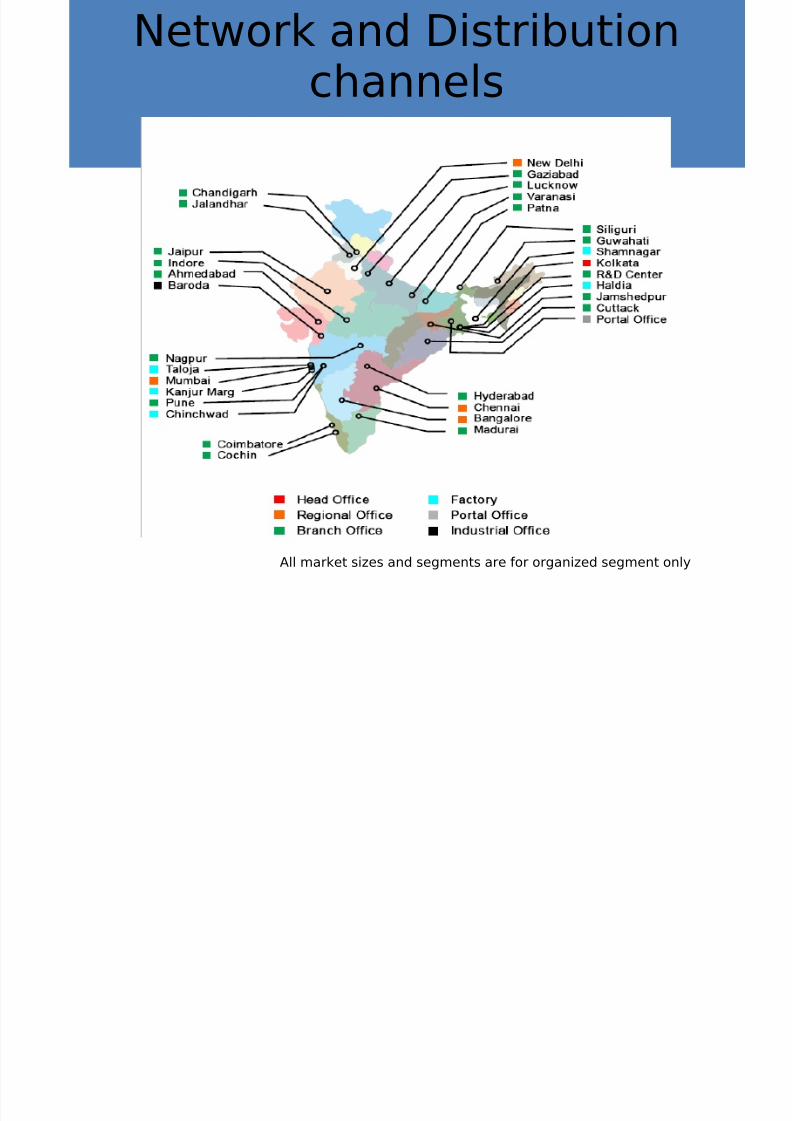

Network and Distributionchannels

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 26/61

All market sizes and segments are for organized segment only

• Exide has manufacturing facilities spreadstrategically across the country.

•

• Exide has the widest distribution reach amongbattery manufacturers in India. It has about38,500 retail outlets for aftermarket sales,which is more than double its nearestcompetitors.

•• The company currently has more than 9,000 main

dealers and 210 hub offices, which it plans toincrease to 250 by end-FY11E and to 510 over

the next 2-3 years.

Strong Distribution Channels

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 27/61

All market sizes and segments are for organized segment only

• Exide is basically into 3 segments , they are :Automotive,Industrial and Submarine.

•

Automotive•

Exide supplies batteries to the major car and two wheelermanufacturers in India [General Motors, Toyota, Hyundai,TATA Motors, Maruti, FIAT, Leyland, Renault, Honda toname a few].

• Almost 80% of cars manufactured in India use a batterymanufactured by EXIDE.

• During FY10, company’s automotive battery segmentshowed a growth of 13% in sales.

• The company has also recently launched the Deep CyclingE-bike batteries for electric bicycles and scooters and is

also in the process of developing batteries for Stop StartMicro Hybrid vehicles

Segment

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 28/61

All market sizes and segments are for organized segment only

Industrial• Industrial batteries are of three types, Conventional

lead acid batteries, VRLA (Valve regulated lead acidbatteries) batteries and Nickel- Cadmium batteries.

• The Company designs and manufacture industrial

batteries in a wide range from 2.5 Ah to 20,400 Ahin conventional flooded and Valve Regulated LeadAcid (VRLA) design.

• In India, it sells products mainly under EXIDE, INDEX,SF, CEIL & POWER SAFE brands and in theinternational markets mainly under CEIL, CHLORIDEand INDEX brands.

• During FY10 company’s industrial battery segmentreported a growth of 10% in sales.

•

Segment(Contd..)

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 29/61

All market sizes and segments are for organized segment only

• SF Sonic : Characterized by power atits peak throughout its lifetime, SFSonic is the ultimate in power-packed batteries. Backed by thetechnology of the world famousFurukawa Battery of Japan, SF Sonic

has a formidable line up of modelsfor all types of 4 wheelers and 2wheelers on Indian roads.

Major Exide products: Auto

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 30/61

All market sizes and segments are for organized segment only

Major Exide products: Auto

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 31/61

All market sizes and segments are for organized segment only

• They are essential requirements to keep electricallyoperated equipments going when the mains fail.

• Railway, Telecommunications, Defense, Mining,Hospitals, Airlines Signaling & Communications. Alldepend on Exide to fulfill their needs for Standby

Power.• Railway Systems, from Air conditioning, Train Lightingto Signaling, Diesel Loco Starter, and ElectricMultiple Units depend on Exide to keep runningsmoothly.

• Starting with batteries for Fork Lift Trucks, Golf Carts,Electric Wheel Chairs, etc., Exide has steadilydeveloped the technology for powering electricvehicles as well as water vessels driven by batterypower.

• The special power-packs are considerably lighter and

can be recharged faster than conventionalbatteries.

Exide Products-IndustrialSegment

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 32/61

All market sizes and segments are for organized segment only

• Motive power batteries : Heat Sealed polypropylene Classic,Magnum & Gen-X batteries are specially made to meetinternational standards of Motive Power.

•

• Traction Batteries: Traction batteries from Exide are soldunder the Ceil & Index brand.

•

• Stand-by batteries(Telecommunications): ‘Exide PowerSafe’series of EPST/MST/NMST/NEPST maintenance free SMFVRLA batteries.

•

• Stand-by batteries(power plants and major infrastructure) :Plante, HDP/NDP/OpZs Range of 2 Volt Tubular batteries.

Exide Products-IndustrialSegment

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 33/61

All market sizes and segments are for organized segment only

Exide Products-IndustrialSegment

Others are:• Camp lamp batteries• Mono bloc batteries• Semi-traction batteries• Solar PV batteries•

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 34/61

All market sizes and segments are for organized segment only

Customers

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 35/61

All market sizes and segments are for organized segment only

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 36/61

All market sizes and segments are for organized segment only

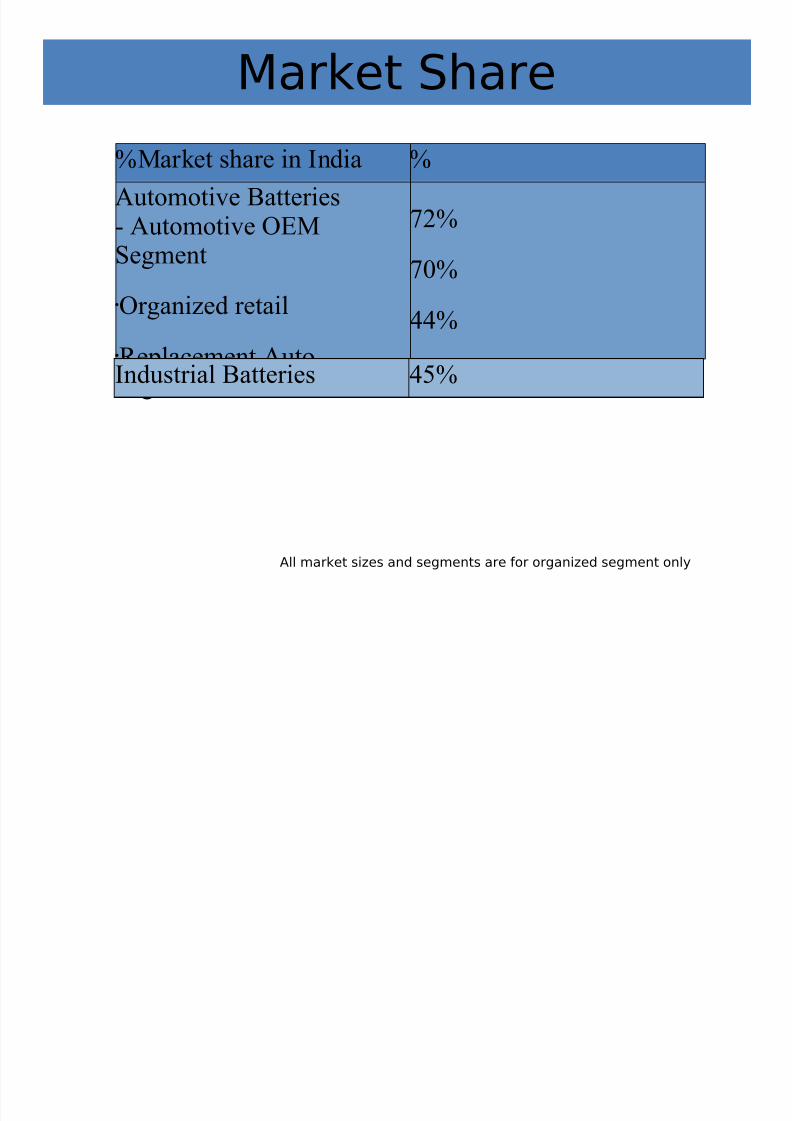

Market Share

%Market share in India %Automotive Batteries- Automotive OEMSegment

Organized retail

Replacement AutoSegment

72%

70%44%

Industrial Batteries 45%

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 37/61

All market sizes and segments are for organized segment only

Market share

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 38/61

All market sizes and segments are for organized segment only

Market share

Di t ib ti

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 39/61

All market sizes and segments are for organized segment only

Distribution :Hub and Retail outlets

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 40/61

All market sizes and segments are for organized segment only

Size of the company

• Rs.537.09Cr

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 41/61

All market sizes and segments are for organized segment only

Mergers and Acquisitions

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 42/61

All market sizes and segments are for organized segment only

M&A contd

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 43/61

All market sizes and segments are for organized segment only

Financials

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 44/61

All market sizes and segments are for organized segment only

Financials

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 45/61

All market sizes and segments are for organized segment only

Financials

d

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 46/61

All market sizes and segments are for organized segment only

Ratios : D/E and CurrentRatio

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 47/61

All market sizes and segments are for organized segment only

Ratios : PE & ROCE

S i E l d b

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 48/61

All market sizes and segments are for organized segment only

Strategies Employed byExide

• Cost Reduction : The company has beenexpanding its production capacities toachieve economies of scale. The companyannounced plans on Oct.,2010 an

investment of Rs 375-400 crores for thisyear to scale up the capacities.Acquired stake in 2 metals company for

supply of Lead to mitigate the risk of volatilityof price variations.

• Product Mix: Exide is also expanding its R &D facilities to develop new technologies fortheir batteries. They are developing newproduct mixes.

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 49/61

All market sizes and segments are for organized segment only

Current Market Share

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 50/61

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 51/61

All market sizes and segments are for organized segment only

Market share within automobilesegment

k h i hi d

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 52/61

All market sizes and segments are for organized segment only

Market share within Industrysegment

M k i f T l I d

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 53/61

All market sizes and segments are for organized segment only

Market size of Telecom Industrysegment

• Telecom

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 54/61

B k h h f

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 55/61

All market sizes and segments are for organized segment only

Breakthroughs of competitors(Contd.)

EXIDE - OTHER BREAKTHROUGHS

• Exide acquired 100% shareholding of ChlorideMetals Limited in 2007 and also acquired 51%shareholding in 2008 and balance 49% of Leadage Alloys India Limited in August 2010and thus Captive smelting and refiningoperations resulted not only in committed

supplies but also provides a price advantagecompared to competition

B k h h f

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 56/61

All market sizes and segments are for organized segment only

Breakthroughs of competitors(Contd.)

•AMARA RAJA BATTERIES LIMITED

•• 2008:Amara Raja Batteries entered the two wheeler battery

segment in with the launch of Amaron Pro Bike Rider 2-wheeler batteries, powered by VRLA (Valve RegulatedLead Acid) technology from JCI customized by AmaraRaja’s R&D for the Indian markets. Key features are :

a) 30% higher crankingb) First ever 60 month warranty

c) Zero Maintenance•• 2010:Agreement with Honda, Japan, for the development of

VRLA motorcycle batteries.• 2010:Launch of UPS,Tribal Italia is a design marvel in the

UPS category that incorporates the best in class UPS

B k h h f

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 57/61

All market sizes and segments are for organized segment only

Breakthroughs of competitors(Contd.)

• Amara Raja was the first supplier of batteriesfor India’s first micro hybrid vehicle(scorpio)of Mahindra &Mahindra.

•

• Introduced the zero-maintenance automotivebatteries for the first time in India.

•• First to introduce VRLA batteries for industrial

standby applications.•• ARBL is the country's first manufacturer of

maintenance-free traction batteries used inForklifts and Pallet trucks.

B kth h f

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 58/61

All market sizes and segments are for organized segment only

Breakthroughs of competitors(Contd.)

• The company increased its large VRLA batteryoperating capacity. It extended both themedium (increase by 50%) and the small VRLAbattery capacity (extended from 1.8 million

units to 2.4 million units). This increase in theoperating capacity will not only provideeconomies of large scale, but will also aid thecompany cater to a larger market, as it seeks totap the unorganized battery sector.

B kth h f

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 59/61

All market sizes and segments are for organized segment only

Breakthroughs of competitors(Contd.)

HBL POWER SYSTEMS

• Tubular gel VRLA battery introduced to Indian

market for Telecom and Solar powerapplications and PLT VRLA AGM SLI batteryis the first for the automotive sector.

•

• A joint venture in Saudi Arabia with theAlShuwayer group that will focus on leadand industrial battery demand in the MENAregion .

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 60/61

All market sizes and segments are for organized segment only

• Detailed analysis of Financial performance, Sales , Growth andProfitability of Exide and its competitors.

•• Segment wise analysis

•• Analysis of different cost

•• Analysis of Past Strategies of Exide that has followed and their

current strategies and analysis of Competitor strategies.

•• SWOT analysis of EXIDE and other competitors.

•• New Product Launches and Target markets.

Future Work

8/7/2019 SM presentation_Akash Sarkar

http://slidepdf.com/reader/full/sm-presentationakash-sarkar 61/61

Thank You