dr g raviprasad

TRANSCRIPT

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 1/14

12/16/200

Dr G Raviprasad

5th December, 2009

FAI Annual Seminar,

Hyderabad

India-Present Fertiliser Policy Scenario

• Urea under fully controlled environment:

• Phosphatics: partially decontrolled but state-wise MRPsand allocation is fixed by the Central Government

• Result: Huge difference between international prices of fertilisers and prices to Indian Farmers, and hugewastage of inputs

• Subsidy: 2008-09 we have spent 1 lakh crore onfertiliser subsidy and nevertheless this year also we willbe spending at least half of that

• It will have an adverse impact on the long run

• Discussions are on for a nutrient based subsidy system• We are also talking about giving subsidy directly to

farmers

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 2/14

12/16/200

What is total decontrol?

• A scenario where farmers pay the actualinternational market price of fertilisers. MRP isopen and anybody is free to sell any fertiliser anywhere in india as long as the product is recognisedby Governemnt of India

Scheme of presentation

• Prices of raw material- the trend

• Major fertiliser price trend

• Expected fertilisers price to farmers after decontrol

• The expected consumption of fertilisers afterdecontrol

• The state wise consumption projection afterdecontrol

• The impact on fertliser marketing

• The strategic intervention

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 3/14

12/16/200

5

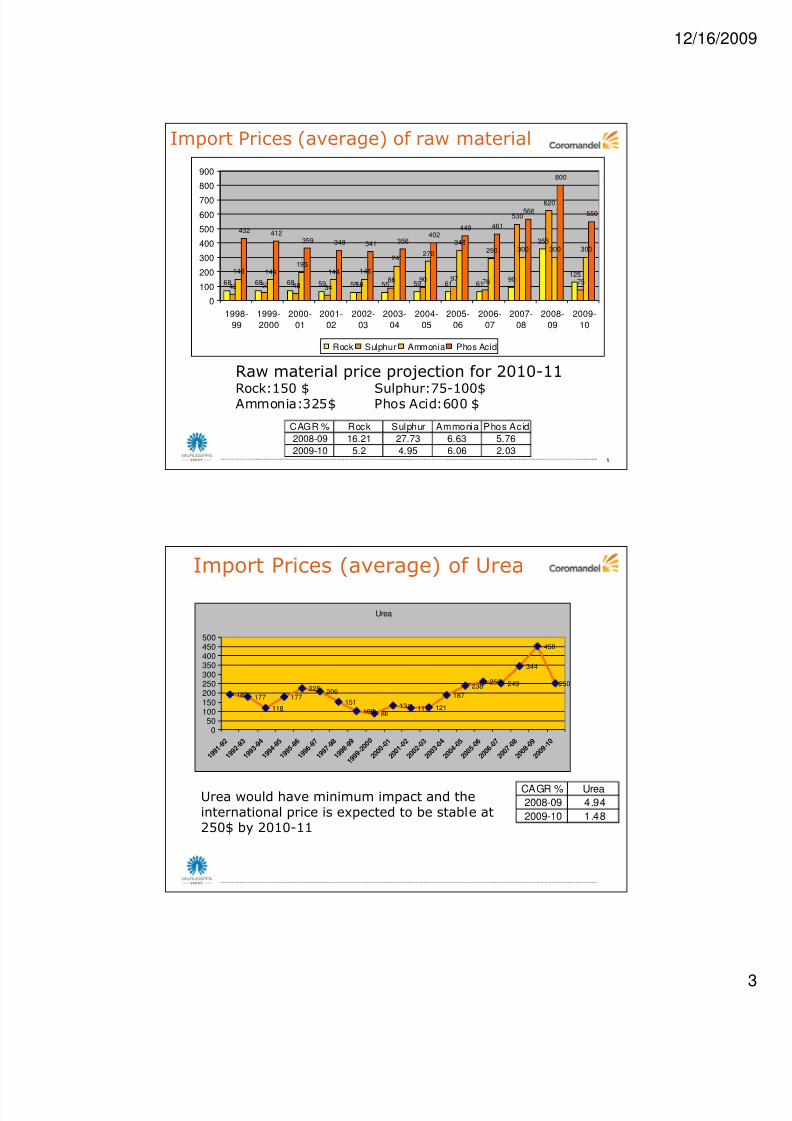

Import Prices (average) of raw material

68 68 68 59 55 55 59 61 6190

355

125

42 52 48 34 5686 90 97 76

530

620

75

148 144195

144 146

241270

348290 300 300 300

432 412359 348 341 356

402449 461

566

800

550

0

100

200

300

400

500

600

700

800

900

1998-

99

1999-

2000

2000-

01

2001-

02

2002-

03

2003-

04

2004-

05

2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

Rock Sulphur Ammonia Phos Acid

Raw material price projection for 2010-11

Rock:150 $ Sulphur:75-100$Ammonia:325$ Phos Acid:600 $

CAGR % Rock Sulphur Ammonia Phos Acid

2008-09 16.21 27.73 6.63 5.76

2009-10 5.2 4.95 6.06 2.03

Import Prices (average) of Urea

Urea

189 177

118

177

225 206

151

100 86131 117 121

187

238259 249

344

450

250

050

100150200250300350400450500

1 9 9 1

- 9 2

1 9 9 2

- 9 3

1 9 9 3

- 9 4

1 9 9 4

- 9 5

1 9 9 5

- 9 6

1 9 9 6

- 9 7

1 9 9 7

- 9 8

1 9 9 8

- 9 9

1 9 9 9

- 2 0 0

0

2 0 0 0

- 0 1

2 0 0 1

- 0 2

2 0 0 2

- 0 3

2 0 0 3

- 0 4

2 0 0 4

- 0 5

2 0 0 5

- 0 6

2 0 0 6

- 0 7

2 0 0 7

- 0 8

2 0 0 8

- 0 9

2 0 0 9

- 1 0

Urea would have minimum impact and theinternational price is expected to be stable at250$ by 2010-11

CAGR % Urea2008-09 4.94

2009-10 1.48

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 4/14

12/16/200

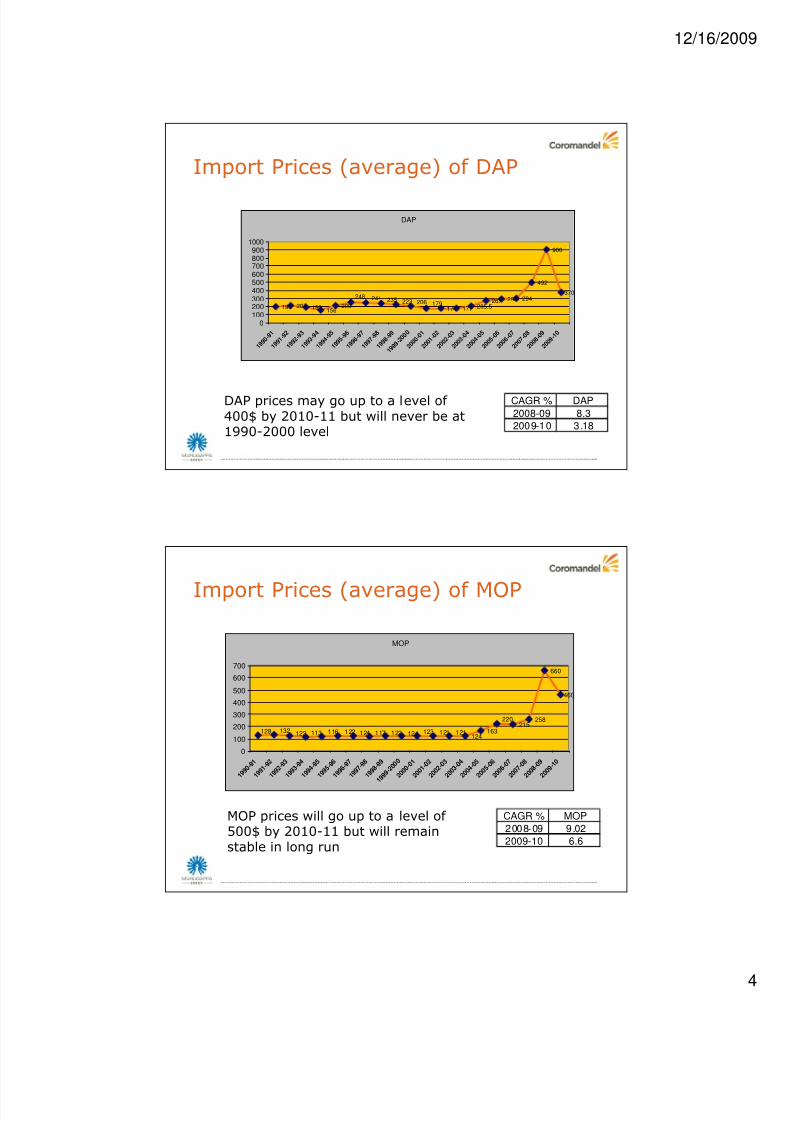

Import Prices (average) of DAP

DAP

198 207 190 156209 174 177 205.5

267 290 294

492

900

370

179206223235241248

0

100

200

300

400

500

600

700

800

900

1000

1 9 9 0

- 9 1

1 9 9 1

- 9 2

1 9 9 2

- 9 3

1 9 9 3

- 9 4

1 9 9 4

- 9 5

1 9 9 5

- 9 6

1 9 9 6

- 9 7

1 9 9 7

- 9 8

1 9 9 8

- 9 9

1 9 9 9

- 2 0 0

0

2 0 0 0

- 0 1

2 0 0 1

- 0 2

2 0 0 2

- 0 3

2 0 0 3

- 0 4

2 0 0 4

- 0 5

2 0 0 5

- 0 6

2 0 0 6

- 0 7

2 0 0 7

- 0 8

2 0 0 8

- 0 9

2 0 0 9

- 1 0

DAP prices may go up to a level of 400$ by 2010-11 but will never be at1990-2000 level

CAGR % DAP

2008-09 8.3

2009-10 3.18

Import Prices (average) of MOP

MOP

124163

215258

660

460

128 132122 113 116 122 124 117 122 124 123 121 121

220

0

100

200

300

400

500

600

700

1 9 9 0

- 9 1

1 9 9 1

- 9 2

1 9 9 2

- 9 3

1 9 9 3

- 9 4

1 9 9 4

- 9 5

1 9 9 5

- 9 6

1 9 9 6

- 9 7

1 9 9 7

- 9 8

1 9 9 8

- 9 9

1 9 9 9

- 2 0 0

0

2 0 0 0

- 0 1

2 0 0 1

- 0 2

2 0 0 2

- 0 3

2 0 0 3

- 0 4

2 0 0 4

- 0 5

2 0 0 5

- 0 6

2 0 0 6

- 0 7

2 0 0 7

- 0 8

2 0 0 8

- 0 9

2 0 0 9

- 1 0

MOP prices will go up to a level of 500$ by 2010-11 but will remainstable in long run

CAGR % MOP

2008-09 9.02

2009-10 6.6

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 5/14

12/16/200

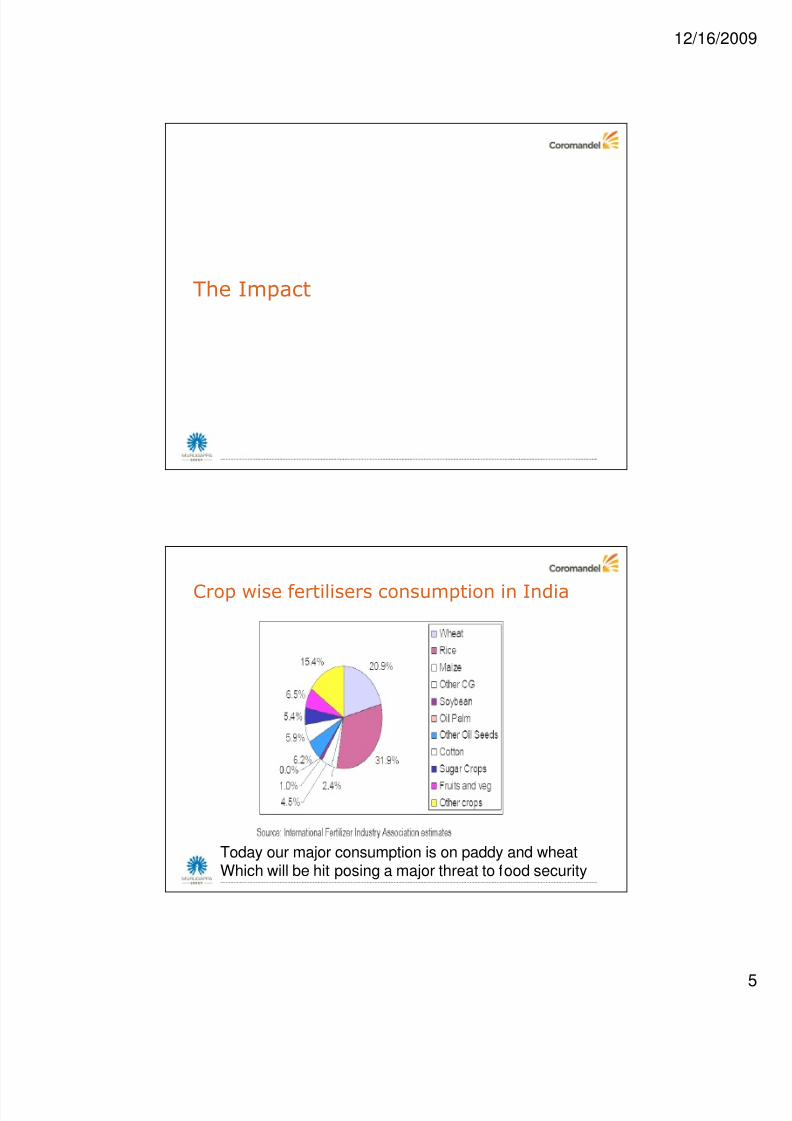

The Impact

Crop wise fertilisers consumption in India

Today our major consumption is on paddy and wheatWhich will be hit posing a major threat to food security

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 6/14

12/16/200

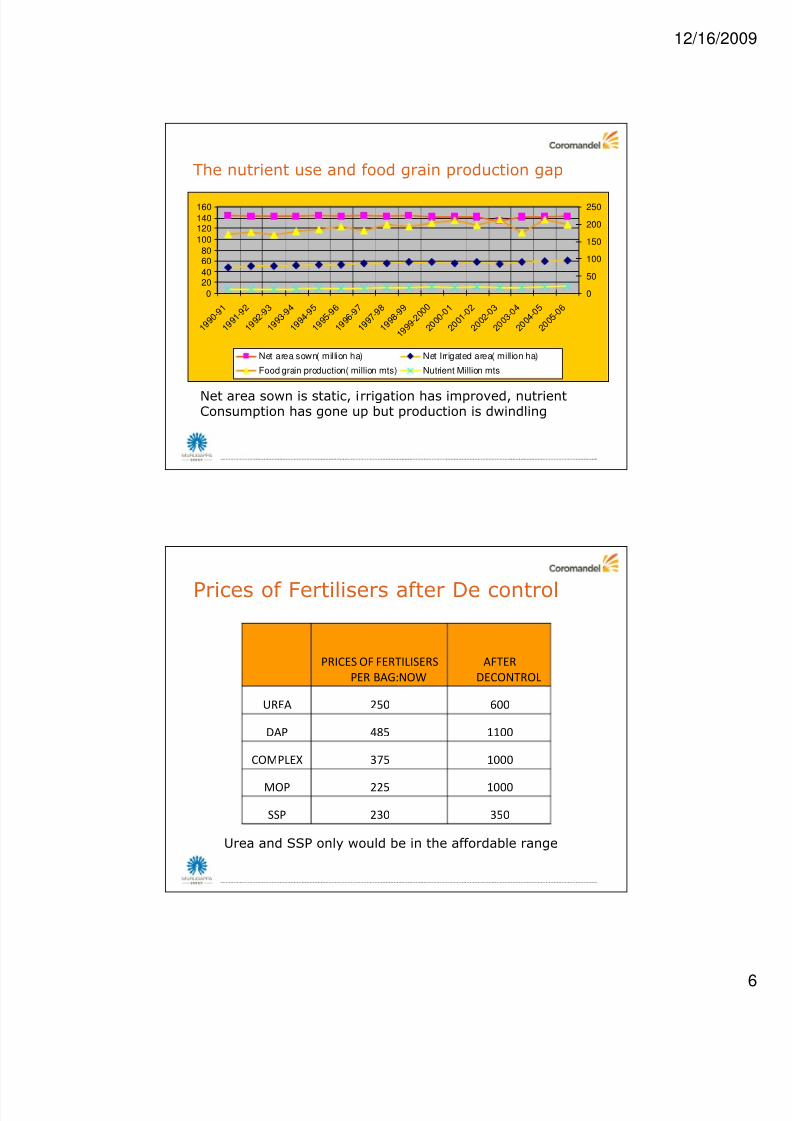

The nutrient use and food grain production gap

0

2040

6080

100

120140

160

1 9 9 0

- 9 1

1 9 9 1

- 9 2

1 9 9 2

- 9 3

1 9 9 3

- 9 4

1 9 9 4

- 9 5

1 9 9 5

- 9 6

1 9 9 6

- 9 7

1 9 9 7

- 9 8

1 9 9 8

- 9 9

1 9 9 9

- 2 0 0

0

2 0 0 0

- 0 1

2 0 0 1

- 0 2

2 0 0 2

- 0 3

2 0 0 3

- 0 4

2 0 0 4

- 0 5

2 0 0 5

- 0 6

0

50

100

150

200

250

Net area sown( million ha) Net Irrigated area( million ha)

Food grain production( million mts) Nutrient Million mts

Net area sown is static, irrigation has improved, nutrientConsumption has gone up but production is dwindling

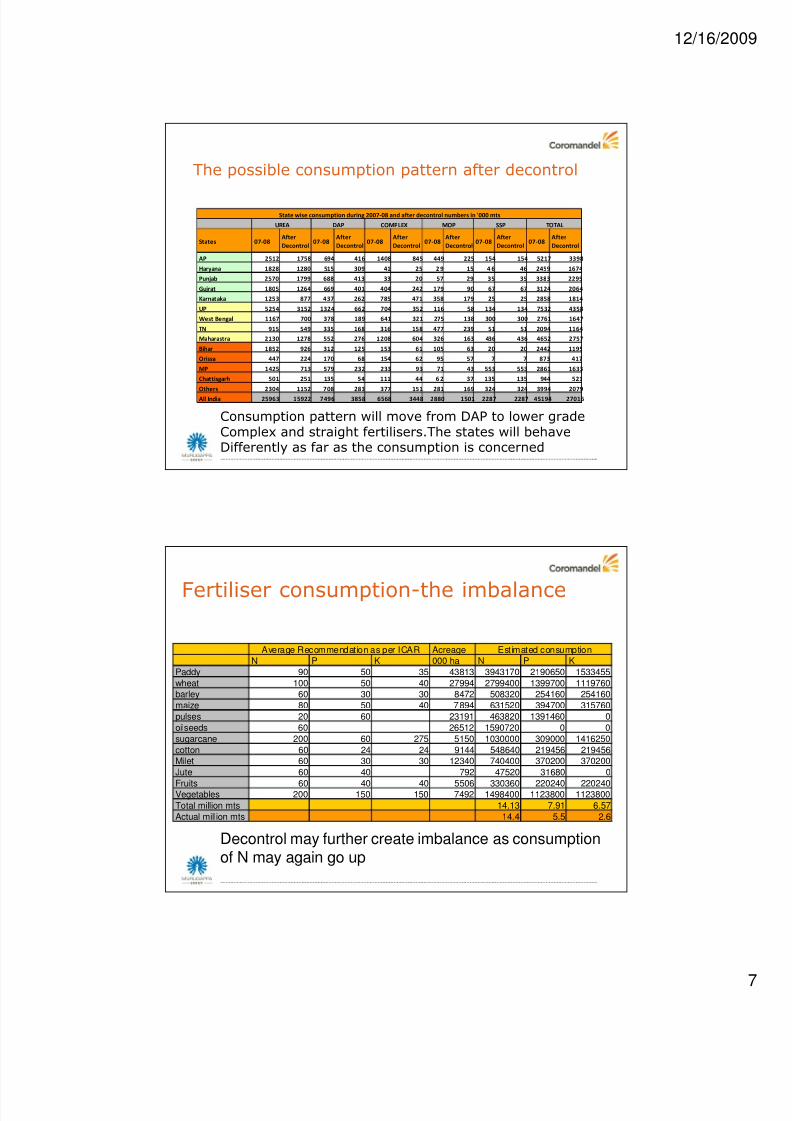

Prices of Fertilisers after De control

PRICES OF FERTILISERS

PER BAG:NOW

AFTER

DECONTROL

UREA 250 600

DAP 485 1100

COMPLEX 375 1000

MOP 225 1000

SSP 230 350

Urea and SSP only would be in the affordable range

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 7/14

12/16/200

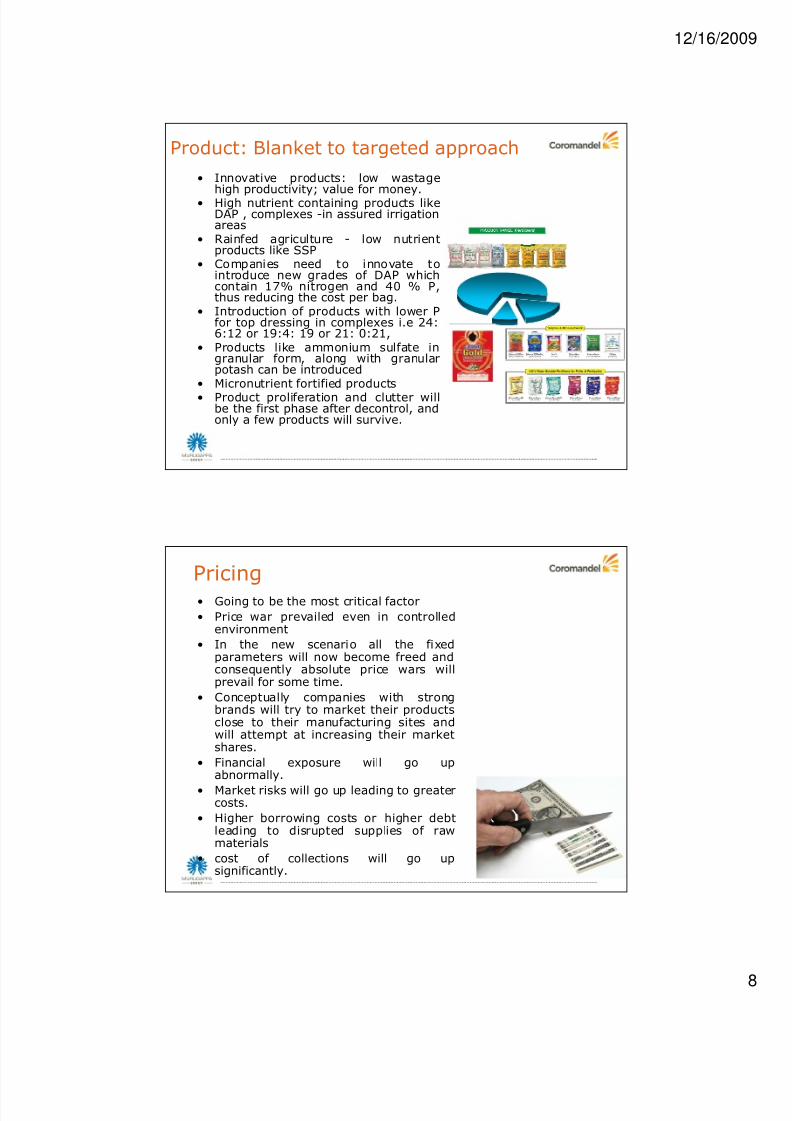

The possible consumption pattern after decontrol

States 07-08After

Decontrol07-08

After

Decontrol07-08

After

Decontrol07-08

After

Decontrol07-08

After

Decontrol07-08

After

Decontrol

AP 2512 1758 694 416 1408 845 449 225 154 154 5217 3398

Haryana 1828 1280 515 309 41 25 2 9 15 4 6 46 2459 1674

Punjab 2570 1799 688 413 33 20 57 29 35 35 3383 2295

Gujrat 1805 1264 669 401 404 242 179 90 67 67 3124 2064

Karnataka 1253 877 437 262 785 471 358 179 25 25 2858 1814

UP 5254 3152 1324 662 704 352 116 58 134 134 7532 4358

West Bengal 1167 700 378 189 641 321 275 138 300 300 2761 1647

TN 915 549 335 168 316 158 477 239 51 51 2094 1164

Maharastra 2130 1278 552 276 1208 604 326 163 436 436 4652 2757

Bihar 1852 926 312 125 153 61 105 63 20 20 2442 1195

Orissa 447 224 170 68 154 62 95 57 7 7 873 417

MP 1425 713 579 232 233 93 71 43 553 553 2861 1633

Chattisgarh 501 251 135 54 111 44 6 2 37 135 135 944 521

Others 2304 1152 708 283 377 151 281 169 324 324 3994 2079

All India 25963 15922 7496 3858 6568 3448 2880 1501 2287 2287 45194 27016

SSP TOTAL

State wise consumption during 2007-08 and after decontrol numbers in '000 mts

UREA DAP COMPLEX MOP

Consumption pattern will move from DAP to lower gradeComplex and straight fertilisers.The states will behaveDifferently as far as the consumption is concerned

Fertiliser consumption-the imbalance

Acreage

N P K 000 ha N P K

Paddy 90 50 35 43813 3943170 2190650 1533455

wheat 100 50 40 27994 2799400 1399700 1119760

barley 60 30 30 8472 508320 254160 254160

maize 80 50 40 7894 631520 394700 315760

pulses 20 60 23191 463820 1391460 0

oilseeds 60 26512 1590720 0 0

sugarcane 200 60 275 5150 1030000 309000 1416250

cotton 60 24 24 9144 548640 219456 219456

Milet 60 30 30 12340 740400 370200 370200

Jute 60 40 792 47520 31680 0

Fruits 60 40 40 5506 330360 220240 220240Vegetables 200 150 150 7492 1498400 1123800 1123800

Total million mts 14.13 7.91 6.57

Actual million mts 14.4 5.5 2.6

Average Recommendation as per ICAR Estimated consumption

Decontrol may further create imbalance as consumptionof N may again go up

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 8/14

12/16/200

Product: Blanket to targeted approach

• Innovative products: low wastagehigh productivity; value for money.

• High nutrient containing products likeDAP , complexes -in assured irrigationareas

• Rainfed agriculture - low nutrientproducts like SSP

• Companies need to innovate tointroduce new grades of DAP whichcontain 17% nitrogen and 40 % P,thus reducing the cost per bag.

• Introduction of products with lower Pfor top dressing in complexes i.e 24:6:12 or 19:4: 19 or 21: 0:21,

• Products like ammonium sulfate ingranular form, along with granularpotash can be introduced

• Micronutrient fortified products• Product proliferation and clutter will

be the first phase after decontrol, andonly a few products will survive.

Pricing• Going to be the most critical factor

• Price war prevailed even in controlledenvironment

• In the new scenario all the fixedparameters will now become freed andconsequently absolute price wars willprevail for some time.

• Conceptually companies with strongbrands will try to market their productsclose to their manufacturing sites andwill attempt at increasing their marketshares.

• Financial exposure will go upabnormally.

• Market risks will go up leading to greatercosts.

• Higher borrowing costs or higher debtleading to disrupted supplies of rawmaterials

• cost of collections will go upsignificantly.

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 9/14

12/16/200

Distribution

• companies have to come together tosurvive post decontrol and streamlinetheir distribution set up.

• Distant markets will not be servicedby companies.

• Therefore the real aspect of productexchange has to be adoptedwhereby; companies will beproducing two or more brands fromthe same location, leading to shared

marketing concepts.

Imports

• Imports will play a key role,from the point of pricing andavailability.

• Once availability increases anddemand comes downautomatically, pricing pressureswill enter the matrix upsettingthe equilibrium.

• Mature companies will be able tobalance

• Imports will always be used bythe government to bridgedemand supply gaps in specificareas or at specific times so thatindustry does not profitabnormally.

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 10/14

12/16/200

Market Development

• Chaotic scenario in the field since allcompanies would be anxious to create brandpull

• This will have serious backlash and thecustomer I,e the farmer will be left withoutany direction ,and the products andstrategies will be less understood .

• Buying behaviour of farmers will drasticallychange and the entire consumer behaviourwill need to be revisited.

• As the issues evolve solutions will be

emerging, and time alone will be a witnessto all changes.

Strategic intervention

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 11/14

12/16/200

Product to Solutions

• Till now the fertiliser application is based on certainavailable grades in the market and farmers go forblanket application

• Currently grades and brands are region specific

• In total decontrol, the sale of fertilisers will besubstituted with total nutrient solutions.

• Micronutrient fortified fertilisers, customized fertilisers,water soluble fertilisers, bio fertilizers, organic fertilizersetc will be marketed to provide comprehensive nutrientsolutions which are cost effective.

• In fact the traditional 50 kg, bag may be replaced bydosages per acre and they may be stage and location

specific.

Understanding customer behaviour

• Present cost of fertilisers: 30 to 40 % of the total cost

• After decontrol: economics comes ahead0f added benefits or aesthetics

• The increased cost of fertilisers can resultin two activities.– Reduced chemical fertilizer application

:poor food grain output.– apply the cheapest: imbalanced

chemical nutrition• Dealer now loses his ability to influence

and the focus shifts to farmers• Companies will revive extension

programmes.• Crop productivity will become a key

rallying point and use of macro, micro andtrace elements will set in.

• Soil analysis, crop husbandry, correctplant nutrition, appropriate plantprotection and mechanization will be thebuzz words.

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 12/14

12/16/200

Product versatility

• Companies with versatile product offerings will have an edge• Companies with a single product will cease to exist or partner

with bigger ones.• Business will no more be volume driven but versatility and

value driven.• Companies that offer total plant nutrition will score• Organic products, high concentrate fertilisers, micronutrients,

low grade fertilisers, plant protection chemicals, specialties,mechanization, retail etc will come into picture

• Price becomes a critical factor,• Farmers in rainfed areas will opt for cheaper nutrient bags like

SSP, low grade complexes and compost rather than opting forhigh grade fertilisers.

• Rainfall and precipitation will also decide the type of fertilizerused.

• If monsoon is on time and good the farmer will try using highconcentrate fertilisers like DAP,

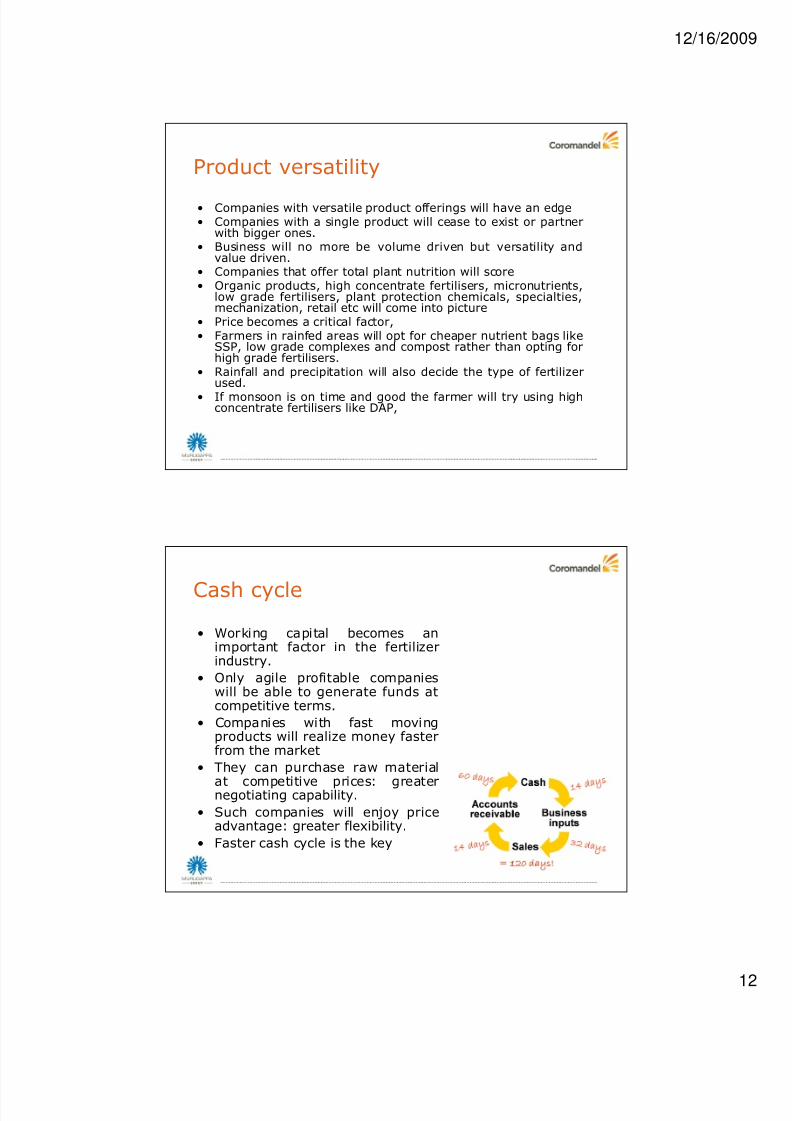

Cash cycle

• Working capital becomes animportant factor in the fertilizerindustry.

• Only agile profitable companieswill be able to generate funds atcompetitive terms.

• Companies with fast movingproducts will realize money fasterfrom the market

• They can purchase raw material

at competitive prices: greaternegotiating capability.

• Such companies will enjoy priceadvantage: greater flexibility.

• Faster cash cycle is the key

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 13/14

12/16/200

Human Resource

• The days of completing sales atrail heads or offices will come toan end

• Crop stage, prices of output,irrigation, competitor stock,brand strength, publicitycampaigns have all to bestudied and marketingpersonnel have to increase theirlevel of contact with farmers.

• Marketing will assume a more

significant role as it becomesthe single fund raising source

competition

• Competition from emergingtechnologies: GM crops, enzyme basedproducts, seaweed based products andmany more.

• All input companies will compete for ashare in farmers wallet.

• Products using recombinant DNA routepromising fixing atmospheric nitrogen,phosphorous releasing bacteria/products, low grade potash will allenter

• From competition, companies have toadopt cooptetion

• Agility and alacrity will be the key• nutrition revolution should happen

after the long cherished greenrevolution

8/6/2019 Dr G Raviprasad

http://slidepdf.com/reader/full/dr-g-raviprasad 14/14

12/16/200

Market Development

• Current methods like wall paintings, trolley paintings,hoardings etc can no longer survive in isolation: needfor integrated communication.

• Targeted and relationship marketing will prove to be thecutting edge

• Data about farmers, size of holdings, crops cultivated,irrigation source etc will gain importance.

• Call centers will form an important farmer touch point

• Decision support systems will also be used toguaranteed yield if farmers subscribe.

• Training programmes will be more holistic and will aimat improved crop productivity rather than disjointed

bursts of product advertisement.

28

www.coromandel.biz