indianagriculture a snapshot

TRANSCRIPT

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 1/89

Confidential- For Kagashin clients onlyMay, 2014

The Difference Between Information & Knowledge

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 2/89

INDIAN AGRICULTURE

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 3/89

Table of Contents

• Agrochemicals

- Overview

- Segments

- Consumption

- Growth Drivers- Top Companies

- Key Challenges

• Insecticides, Fungicides &Herbicides

- Demand Pattern In Indian Market

- Insecticides Market Share

- Fungicides Market Share

- Herbicides Market Share

• Fertilizers

- Overview

- Consumption

- Fertilizer – Indian Scenario

- Usage

- Efficiency

- Production

- Imports

- Subsidy

- State Contribution

- Current Situation

- Growth Drivers

- Challenges

- Policies

• Seeds- Overview

- Growth Drivers

- Production

- Current Status

- Total Cropped Area

- Field Crops: Hybrid Seed Market

- Vegetable Crops: Hybrid Seed

Market

- Impact of new technology

- Regulatory Framework &

Challenges

- Productivity Challenges

- Biotechnology & its effect- Way Forward

- Summary

• Agriculture- Overview

- Size

- Major Acreages

- Major Crops

- Growth drivers

- Major Issues

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 4/89

K e y

S t a t i s t

i c s

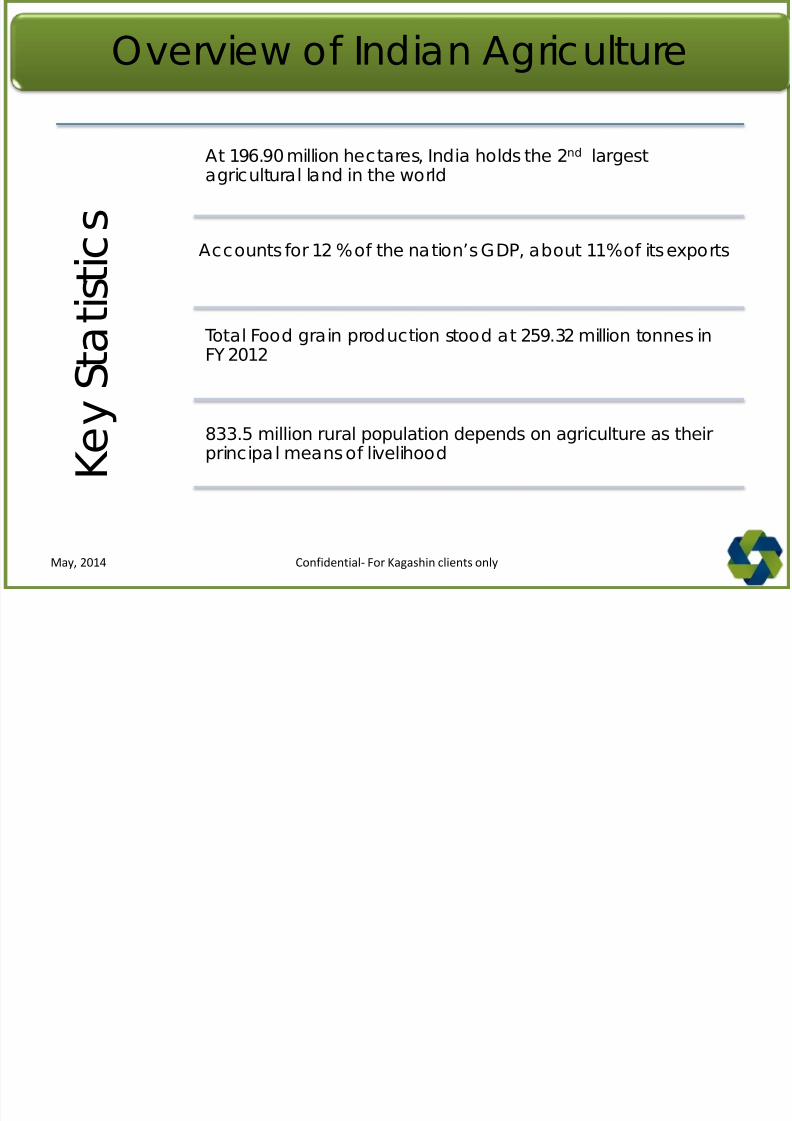

At 196.90 million hectares, India holds the 2nd largestagricultural land in the world

Accounts for 12 % of the nation’s GDP, about 11% of its exports

Total Food grain production stood at 259.32 million tonnes inFY 2012

833.5 million rural population depends on agriculture as theirprincipal means of livelihood

Overview of Indian Agriculture

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 5/89

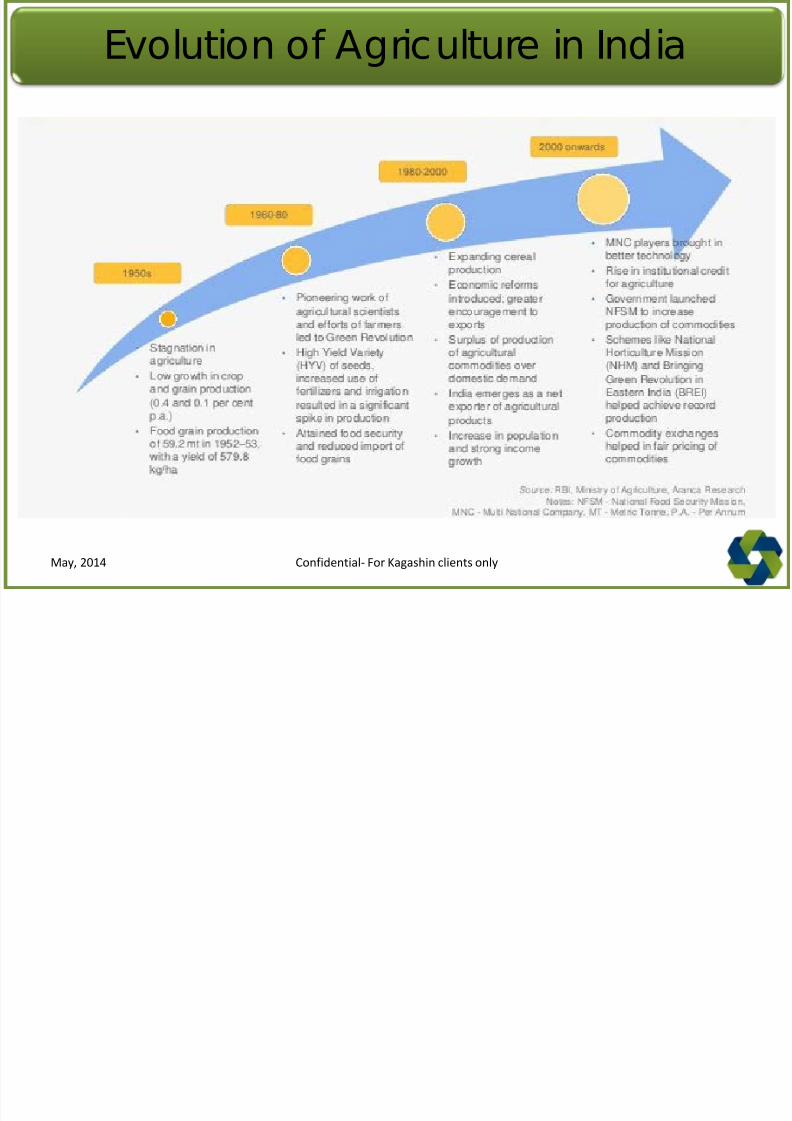

Evolution of Agriculture in India

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 6/89

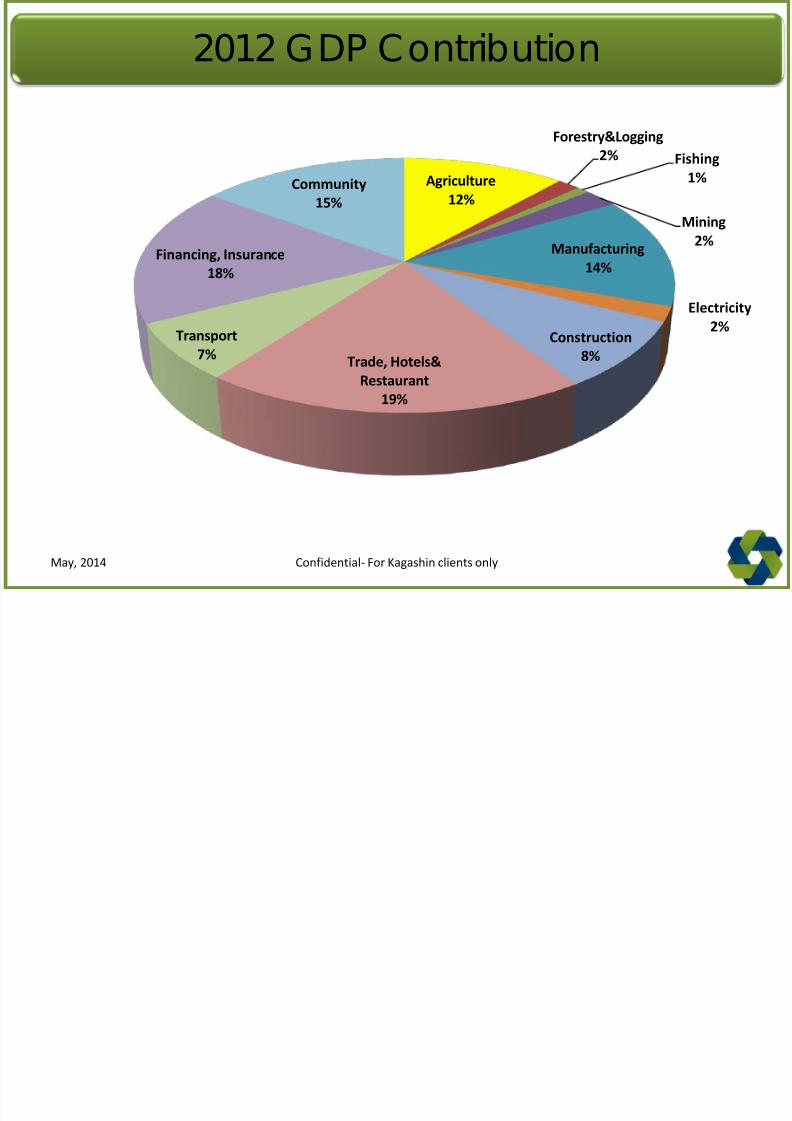

2012 GDP Contribution

Confidential- For Kagashin clients onlyMay, 2014

Agriculture

12%

Forestry&Logging2% Fishing

1%

Mining

2%Manufacturing

14%

Electricity

2%Construction

8%Trade, Hotels&

Restaurant

19%

Transport

7%

Financing, Insurance

18%

Community

15%

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 7/89

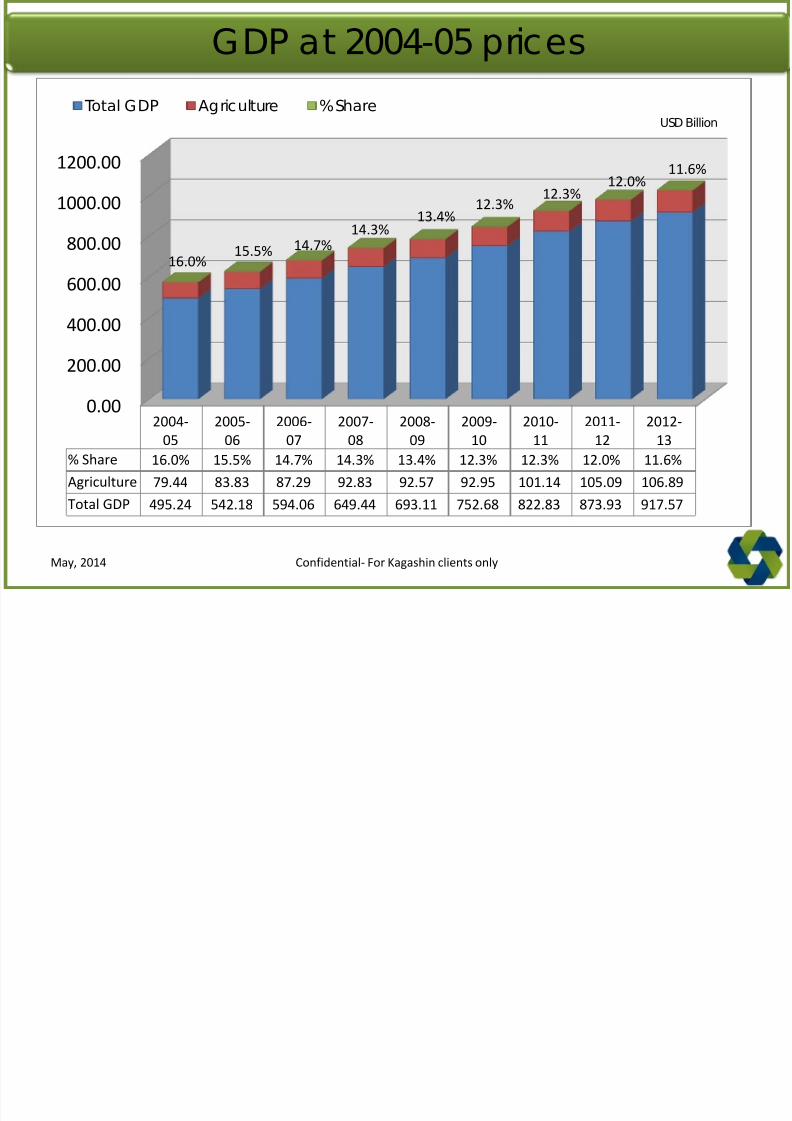

GDP at 2004-05 prices

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

2004-

05

2005-

06

2006-

07

2007-

08

2008-

09

2009-

10

2010-

11

2011-

12

2012-

13

% Share 16.0% 15.5% 14.7% 14.3% 13.4% 12.3% 12.3% 12.0% 11.6%

Agriculture 79.44 83.83 87.29 92.83 92.57 92.95 101.14 105.09 106.89

Total GDP 495.24 542.18 594.06 649.44 693.11 752.68 822.83 873.93 917.57

16.0%15.5% 14.7%

14.3%13.4%

12.3%12.3%

12.0%11.6%

Total GDP Agriculture % ShareUSD Billion

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 8/89

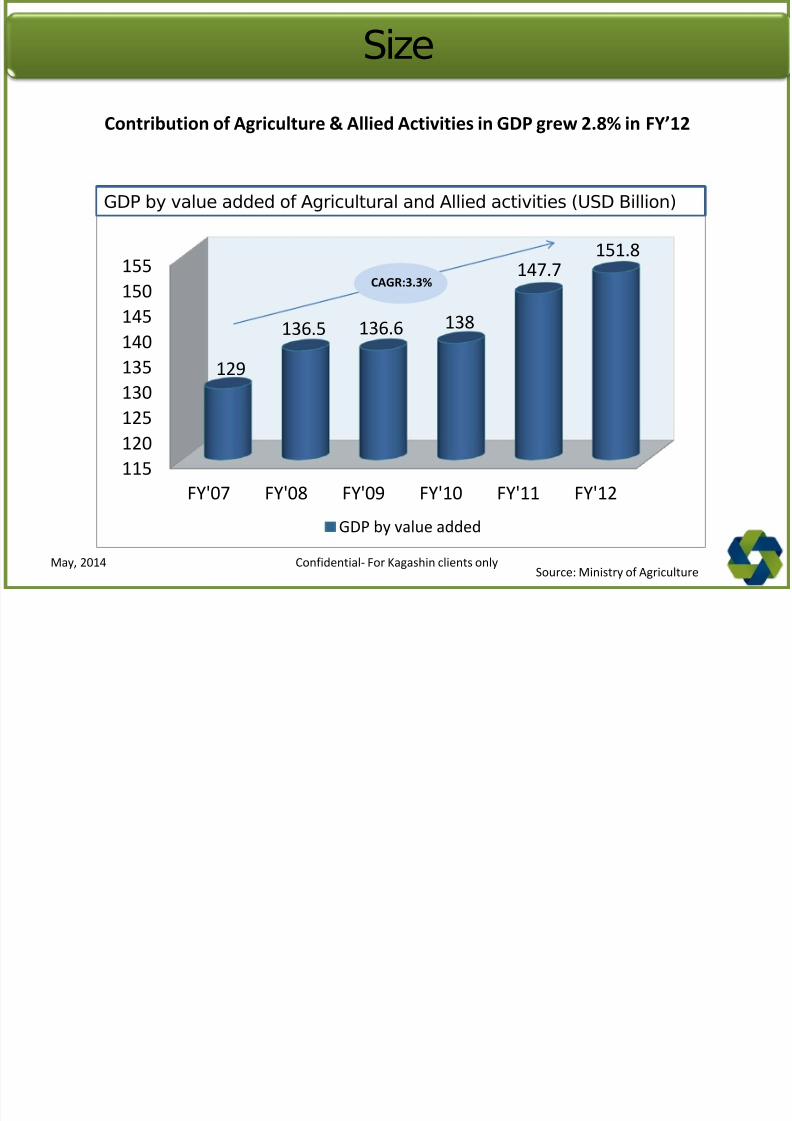

Size

115

120125

130

135

140

145

150

155

FY'07 FY'08 FY'09 FY'10 FY'11 FY'12

129

136.5 136.6 138

147.7

151.8

GDP by value added

CAGR:3.3%

Contribution of Agriculture & Allied Activities in GDP grew 2.8% in FY’12

GDP by value added of Agricultural and Allied activities (USD Billion)

Source: Ministry of AgricultureConfidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 9/89

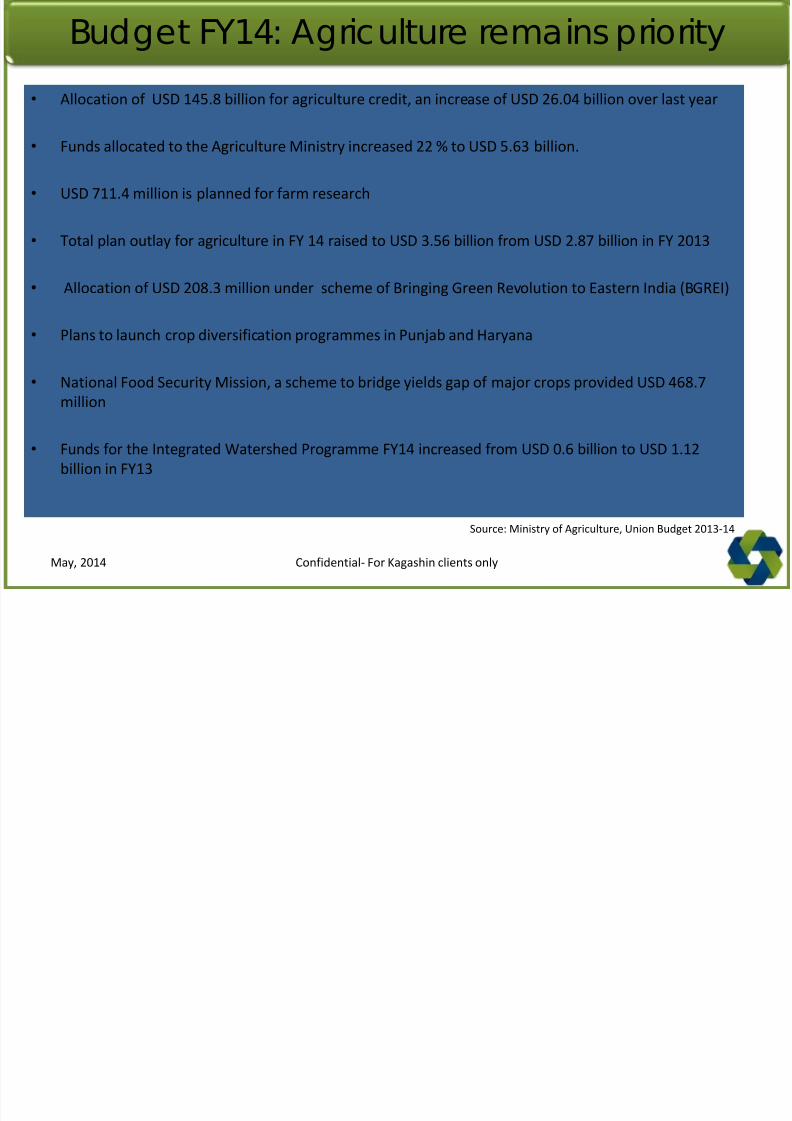

Budget FY14: Agriculture remains priority

• Allocation of USD 145.8 billion for agriculture credit, an increase of USD 26.04 billion over last year

• Funds allocated to the Agriculture Ministry increased 22 % to USD 5.63 billion.

• USD 711.4 million is planned for farm research

• Total plan outlay for agriculture in FY 14 raised to USD 3.56 billion from USD 2.87 billion in FY 2013

• Allocation of USD 208.3 million under scheme of Bringing Green Revolution to Eastern India (BGREI)

• Plans to launch crop diversification programmes in Punjab and Haryana

• National Food Security Mission, a scheme to bridge yields gap of major crops provided USD 468.7

million

• Funds for the Integrated Watershed Programme FY14 increased from USD 0.6 billion to USD 1.12

billion in FY13

Source: Ministry of Agriculture, Union Budget 2013-14

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 10/89

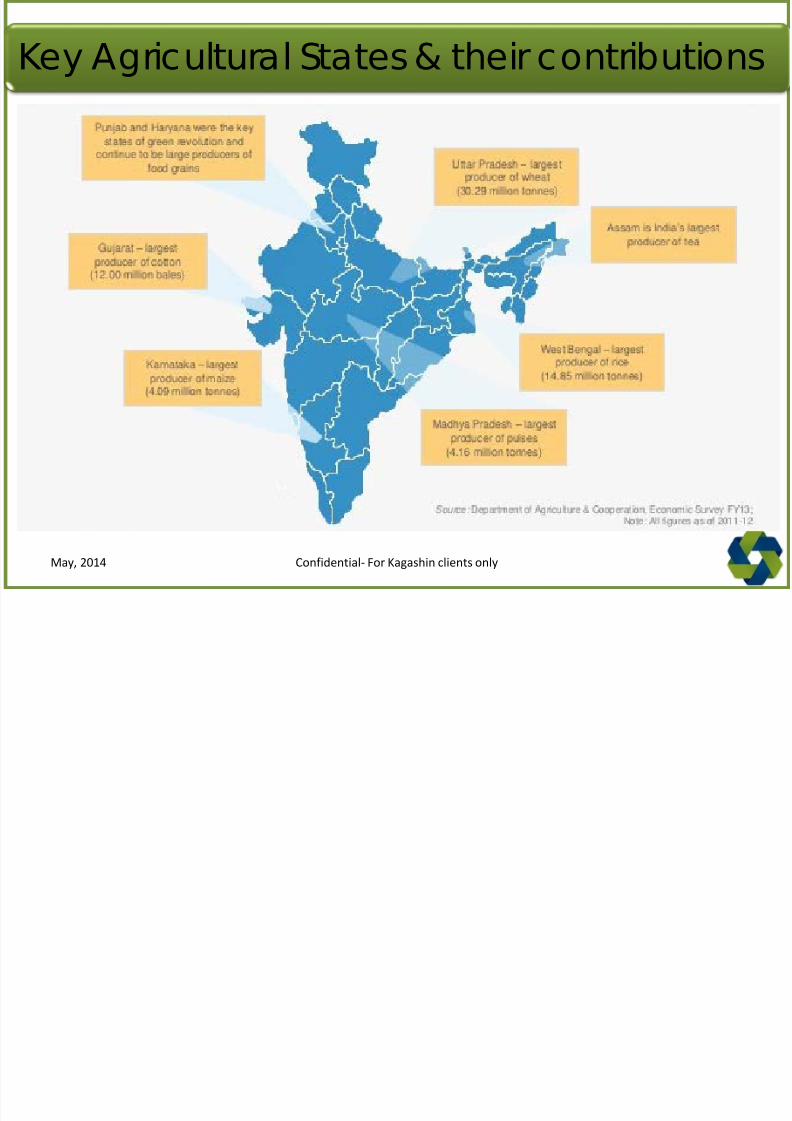

Key Agricultural States & their contributions

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 11/89

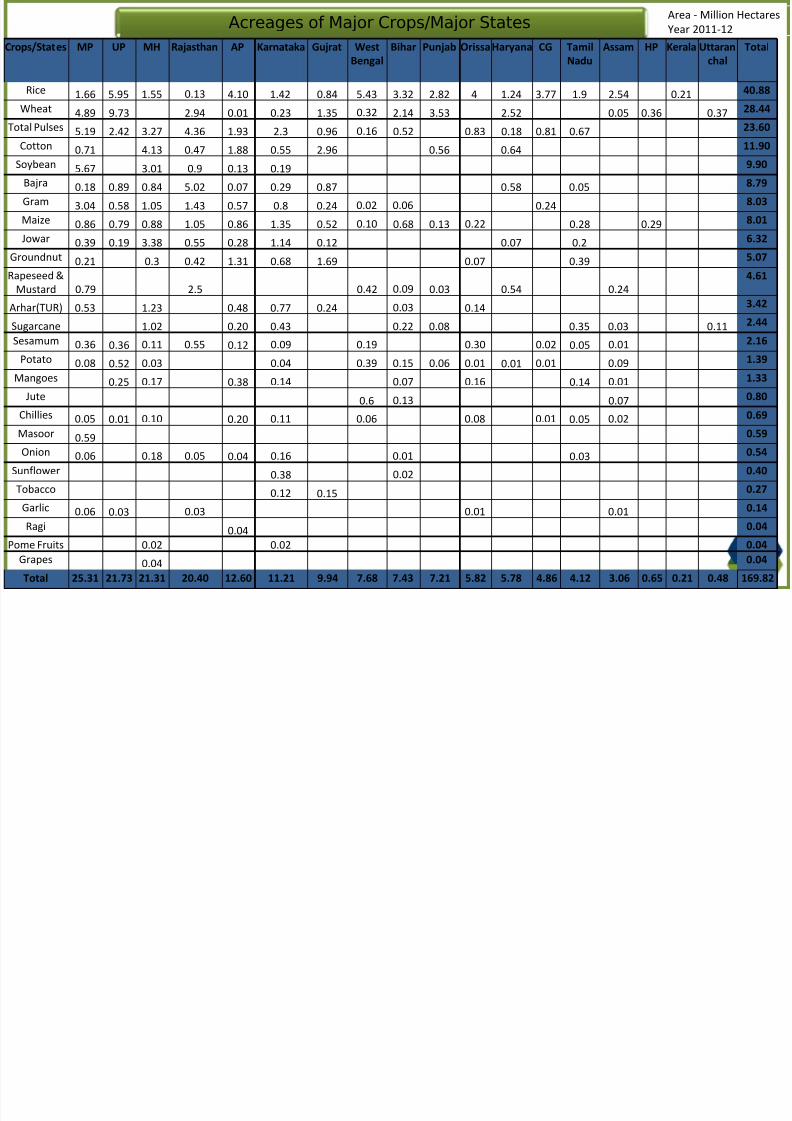

Acreages of Major Crops/Major StatesArea - Million Hectares

Year 2011-12

Crops/States MP UP MH Rajasthan AP Karnataka Gujrat West

Bengal

Bihar Punjab Orissa Haryana CG Tamil

Nadu

Assam HP Kerala Uttaran

chal

Total

Rice 1.66 5.95 1.55 0.13 4.10 1.42 0.84 5.43 3.32 2.82 4 1.24 3.77 1.9 2.54 0.21 40.88

Wheat 4.89 9.73 2.94 0.01 0.23 1.35 0.32 2.14 3.53 2.52 0.05 0.36 0.37 28.44

Total Pulses 5.19 2.42 3.27 4.36 1.93 2.3 0.96 0.16 0.52 0.83 0.18 0.81 0.67 23.60

Cotton 0.71 4.13 0.47 1.88 0.55 2.96 0.56 0.64 11.90

Soybean 5.67 3.01 0.9 0.13 0.19 9.90

Bajra 0.18 0.89 0.84 5.02 0.07 0.29 0.87 0.58 0.05 8.79

Gram 3.04 0.58 1.05 1.43 0.57 0.8 0.24 0.02 0.06 0.24 8.03

Maize 0.86 0.79 0.88 1.05 0.86 1.35 0.52 0.10 0.68 0.13 0.22 0.28 0.29 8.01

Jowar 0.39 0.19 3.38 0.55 0.28 1.14 0.12 0.07 0.2 6.32

Groundnut 0.21 0.3 0.42 1.31 0.68 1.69 0.07 0.39 5.07

Rapeseed &Mustard 0.79 2.5 0.42 0.09 0.03 0.54 0.24

4.61

Arhar(TUR) 0.53 1.23 0.48 0.77 0.24 0.03 0.14 3.42

Sugarcane 1.02 0.20 0.43 0.22 0.08 0.35 0.03 0.11 2.44

Sesamum 0.36 0.36 0.11 0.55 0.12 0.09 0.19 0.30 0.02 0.05 0.01 2.16

Potato 0.08 0.52 0.03 0.04 0.39 0.15 0.06 0.01 0.01 0.01 0.09 1.39

Mangoes 0.25 0.17 0.38 0.14 0.07 0.16 0.14 0.01 1.33

Jute 0.6 0.13 0.07 0.80

Chillies 0.05 0.01 0.10 0.20 0.11 0.06 0.08 0.01 0.05 0.02 0.69Masoor 0.59 0.59

Onion 0.06 0.18 0.05 0.04 0.16 0.01 0.03 0.54

Sunflower 0.38 0.02 0.40

Tobacco 0.12 0.15 0.27

Garlic 0.06 0.03 0.03 0.01 0.01 0.14

Ragi 0.04 0.04

Pome Fruits 0.02 0.02 0.04

Grapes 0.04 0.04

Total 25.31 21.73 21.31 20.40 12.60 11.21 9.94 7.68 7.43 7.21 5.82 5.78 4.86 4.12 3.06 0.65 0.21 0.48 169.82

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 12/89

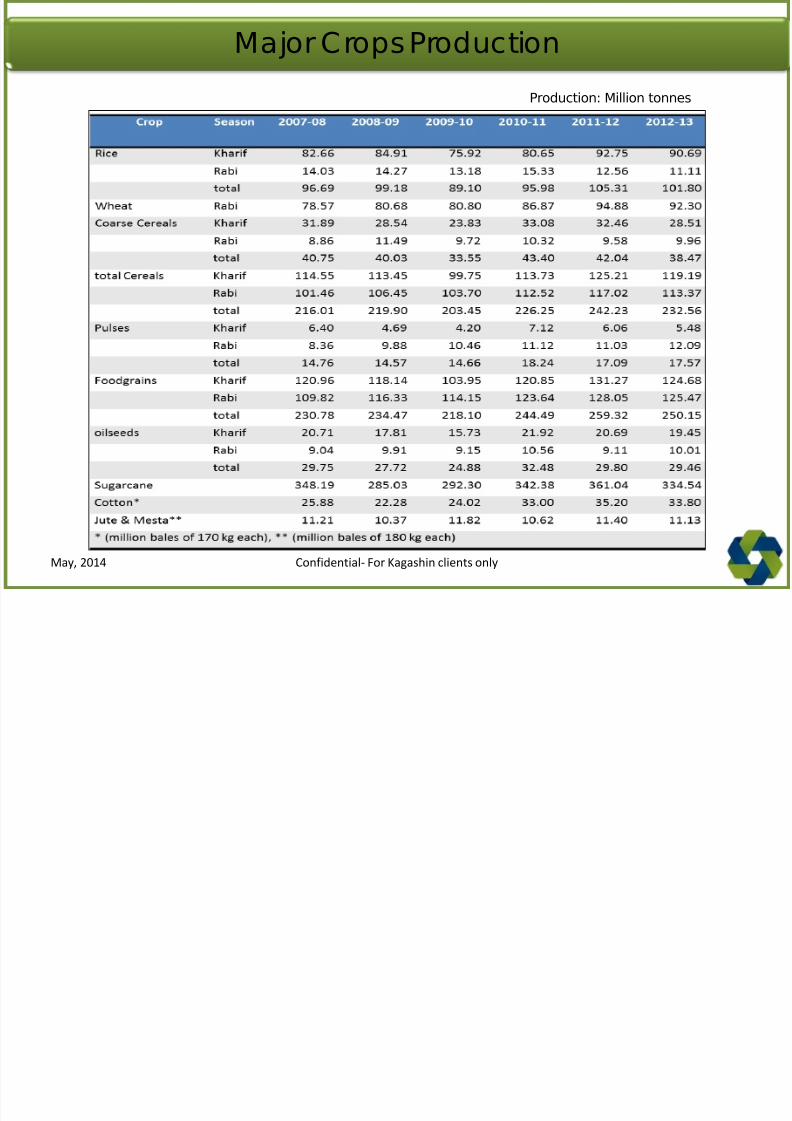

Major Crops Production

Production: Million tonnes

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 13/89

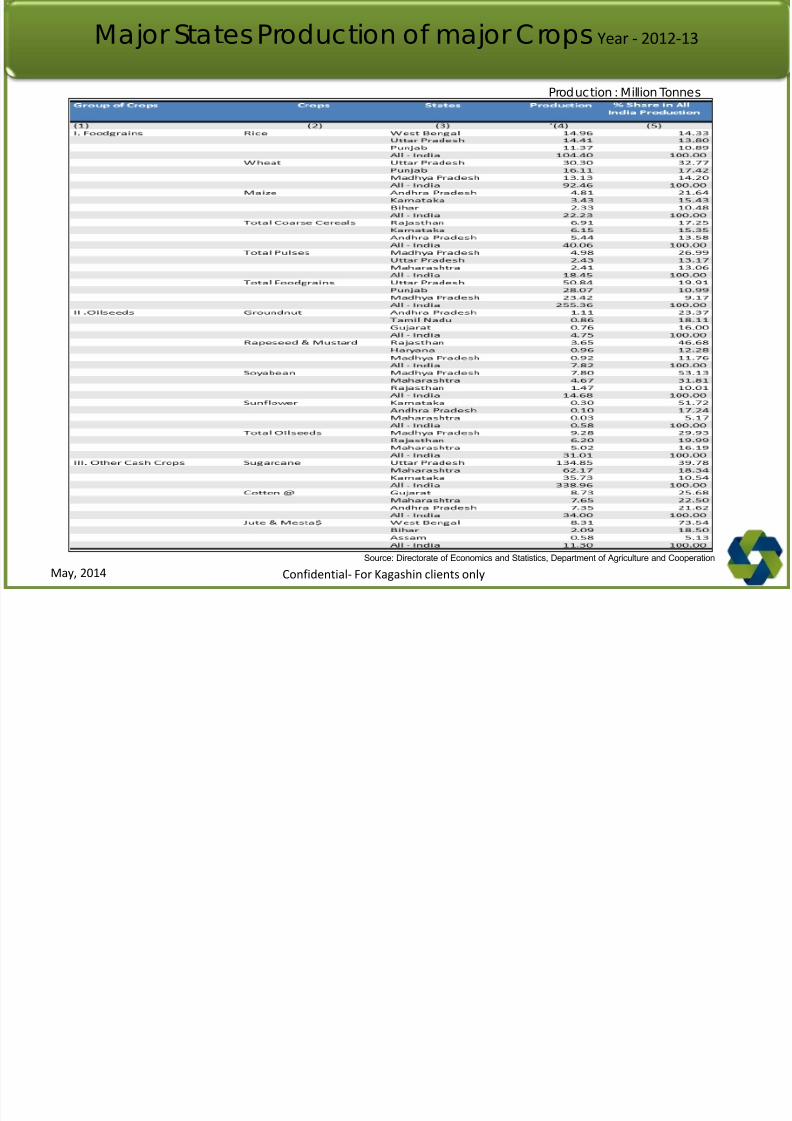

Major States Production of major Crops Year - 2012-13

Source: Directorate of Economics and Statistics, Department of Agriculture and Cooperation

Production : Million Tonnes

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 14/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 15/89

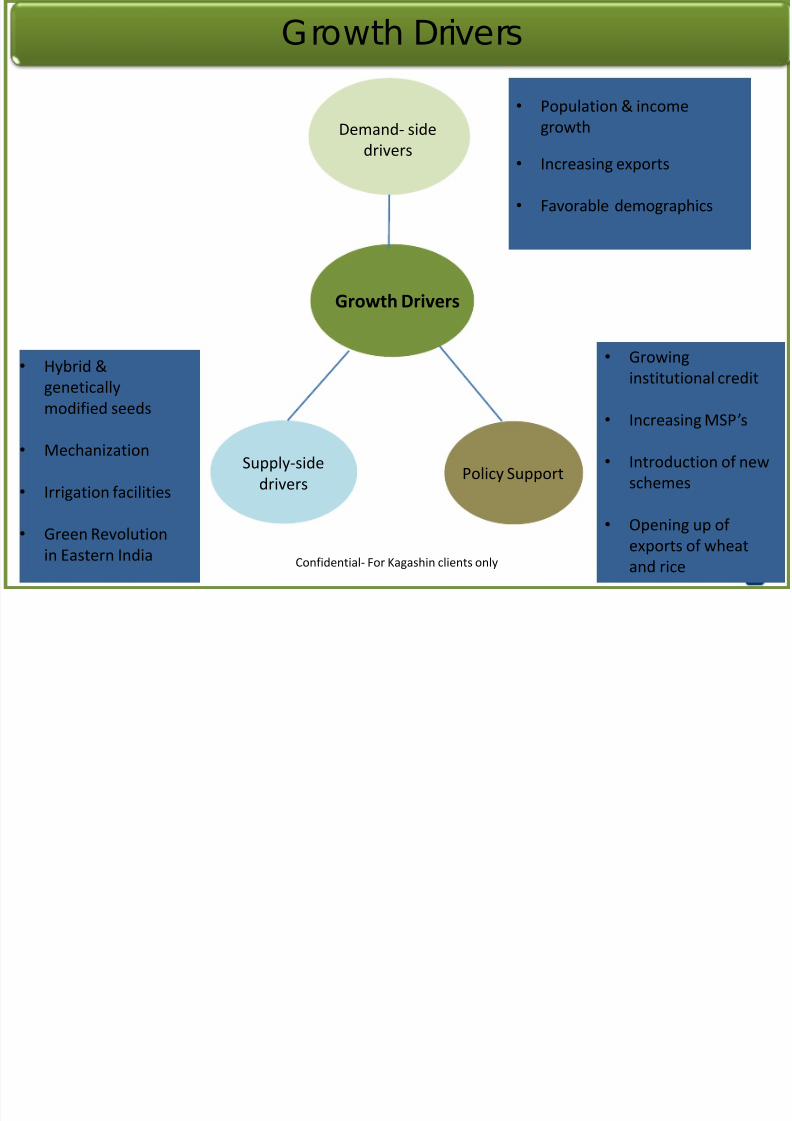

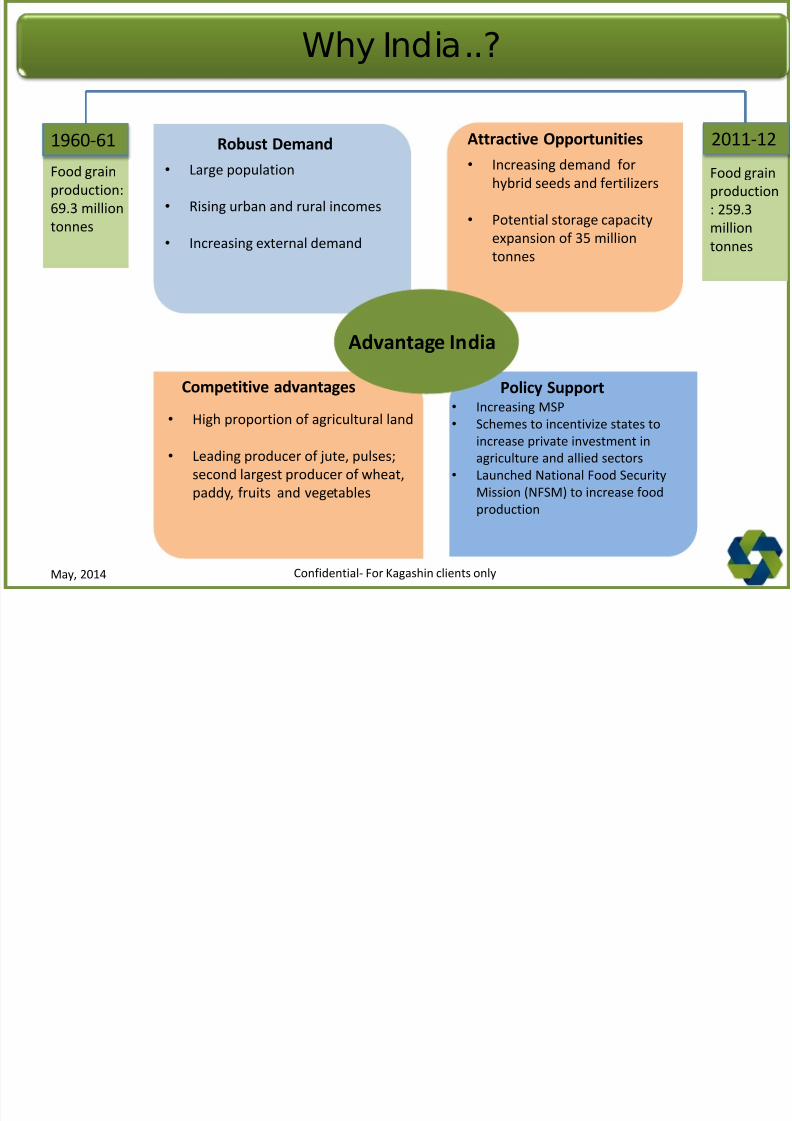

Why India..?

1960-61 2011-12Food grain

production:

69.3 million

tonnes

Food grain

production

: 259.3

million

tonnes

• Large population

• Rising urban and rural incomes

• Increasing external demand

Robust Demand Attractive Opportunities

Policy SupportCompetitive advantages

Advantage India

• Increasing demand for

hybrid seeds and fertilizers

• Potential storage capacity

expansion of 35 million

tonnes

• High proportion of agricultural land

• Leading producer of jute, pulses;

second largest producer of wheat,

paddy, fruits and vegetables

• Increasing MSP

• Schemes to incentivize states to

increase private investment in

agriculture and allied sectors

• Launched National Food Security

Mission (NFSM) to increase food

production

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 16/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 17/89

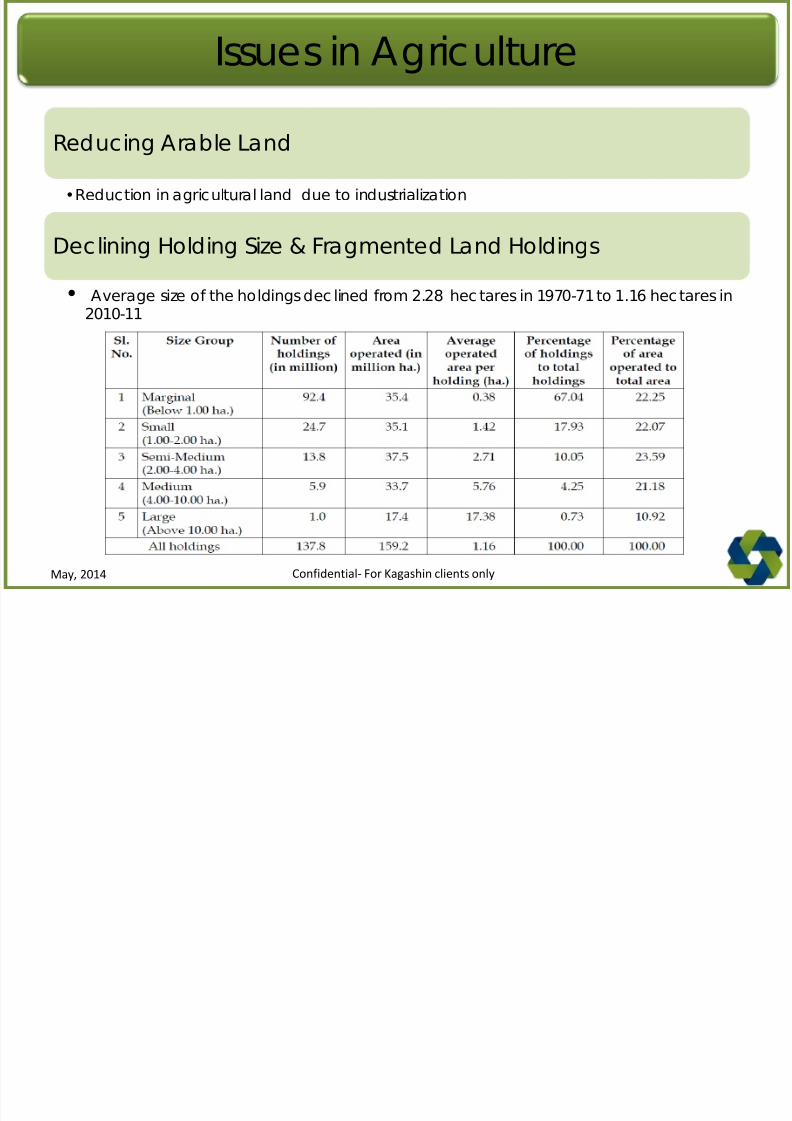

Water Management

•Low utilization of rain water (~28.3 percent), due to lack of infrastructure

Climate Change

•Impact due to c limate changes is expected to cause a drop between 4.5 and 9percent by 2039 and by 25 percent by 2099

Unwanted Crop Diversification

• Diversification to commercially attractive c rops even in adverse agro c limatic conditionsobserved

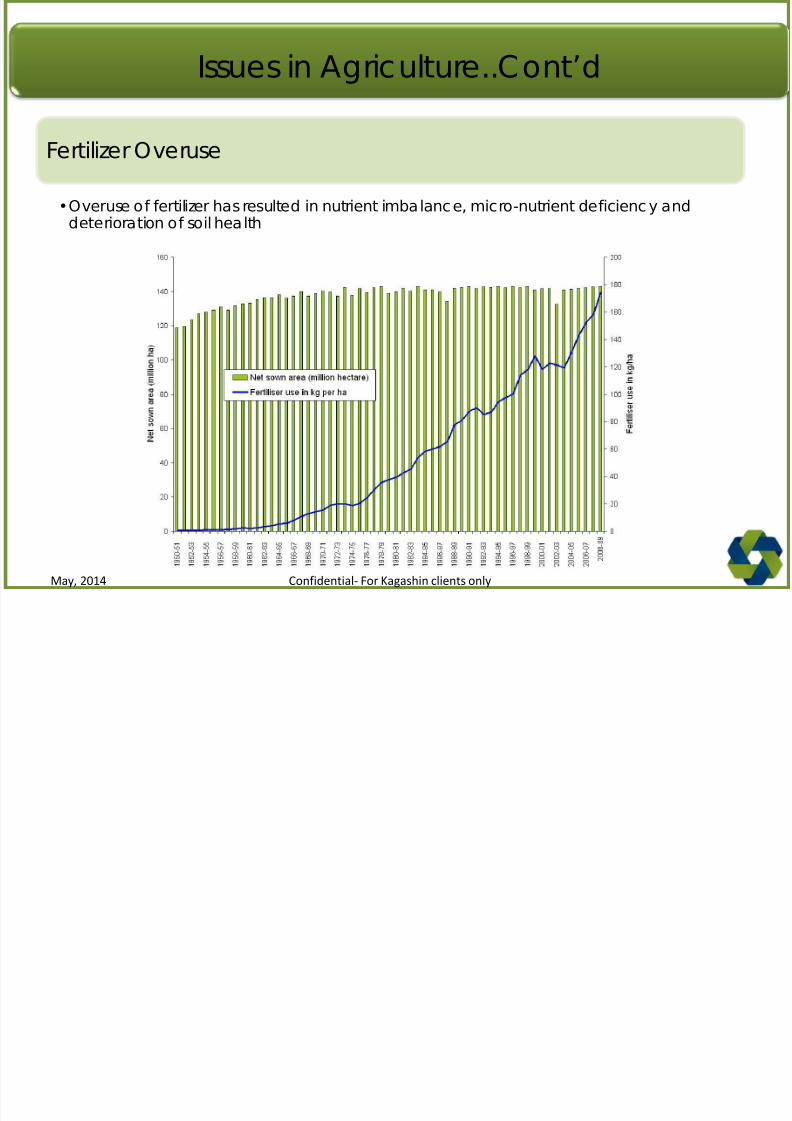

Issues in Agriculture..Cont’d

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 18/89

Rural Credit

•Inefficiencies in disbursement of rural credit to farmers undermine the development ofagriculture

Excessive Government intervention

•Government interventions in factor markets and in output markets has constrainedgrowth of the rural non-farm sec tor

Over-regulation of domestic agricultural trade

•Over- regulation has led to increased costs, price risks and uncertainty

Issues in Agriculture..Cont’d

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 19/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 20/89

AGROCHEMICALS

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 21/89

Table of Contents

• Agriculture- Overview

- Size

- Major Acreages

- Major Crops

- Growth drivers

- Major Issues

• Insecticides, Fungicides &Herbicides

- Demand Pattern In Indian Market

- Insecticides Market Share

- Fungicides Market Share

- Herbicides Market Share

• Fertilizers- Overview

- Consumption

- Fertilizer – Indian Scenario

- Usage

- Efficiency

- Production- Imports

- Subsidy

- State Contribution

- Current Situation

- Growth Drivers

- Challenges

- Policies

• Seeds- Overview

- Growth Drivers

- Production

- Current Status

- Total Cropped Area

- Field Crops: Hybrid Seed Market

- Vegetable Crops: Hybrid Seed

Market

- Impact of new technology

- Regulatory Framework &

Challenges

- Productivity Challenges

- Biotechnology & its effect- Way Forward

- Summary

• Agrochemicals - Overview

- Segments

- Consumption

- Growth Drivers

- Top Companies- Key Challenges

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 22/89

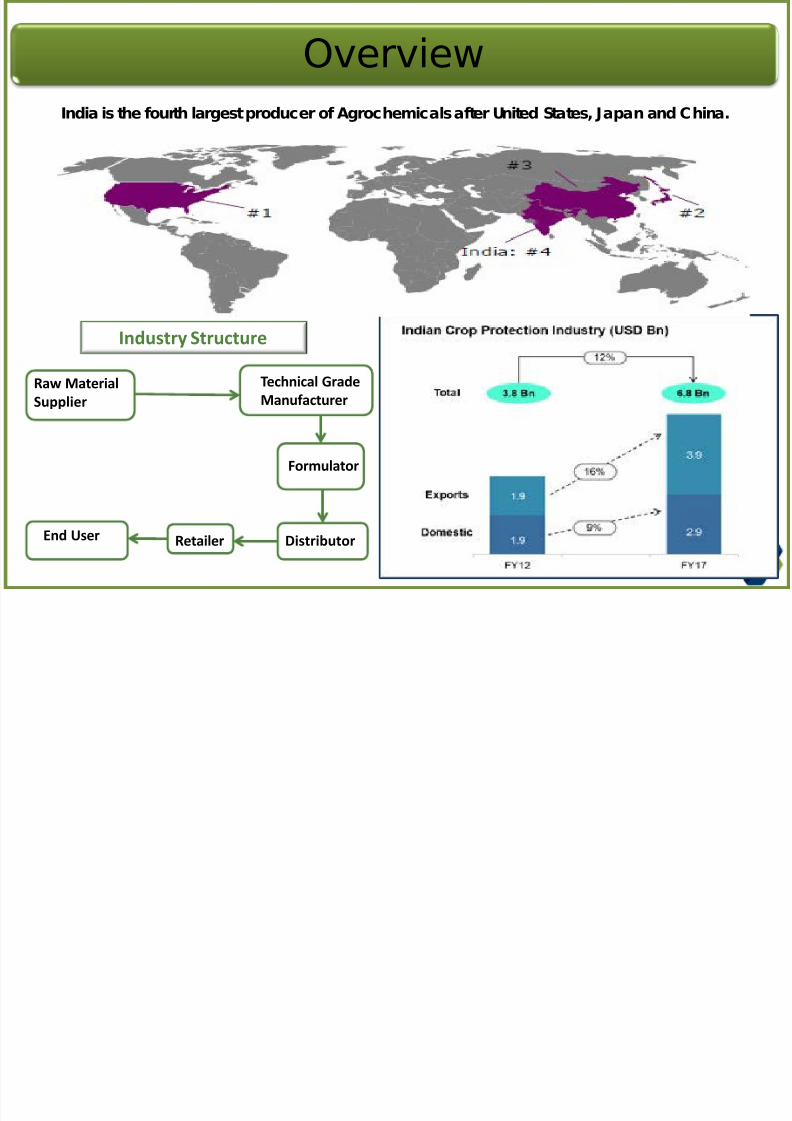

Overview

India is the fourth largest producer of Agrochemicals after United States, Japan and China.

Technical Grade

ManufacturerRaw Material

Supplier

Formulator

DistributorEnd User

Industry Structure

Retailer

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 23/89

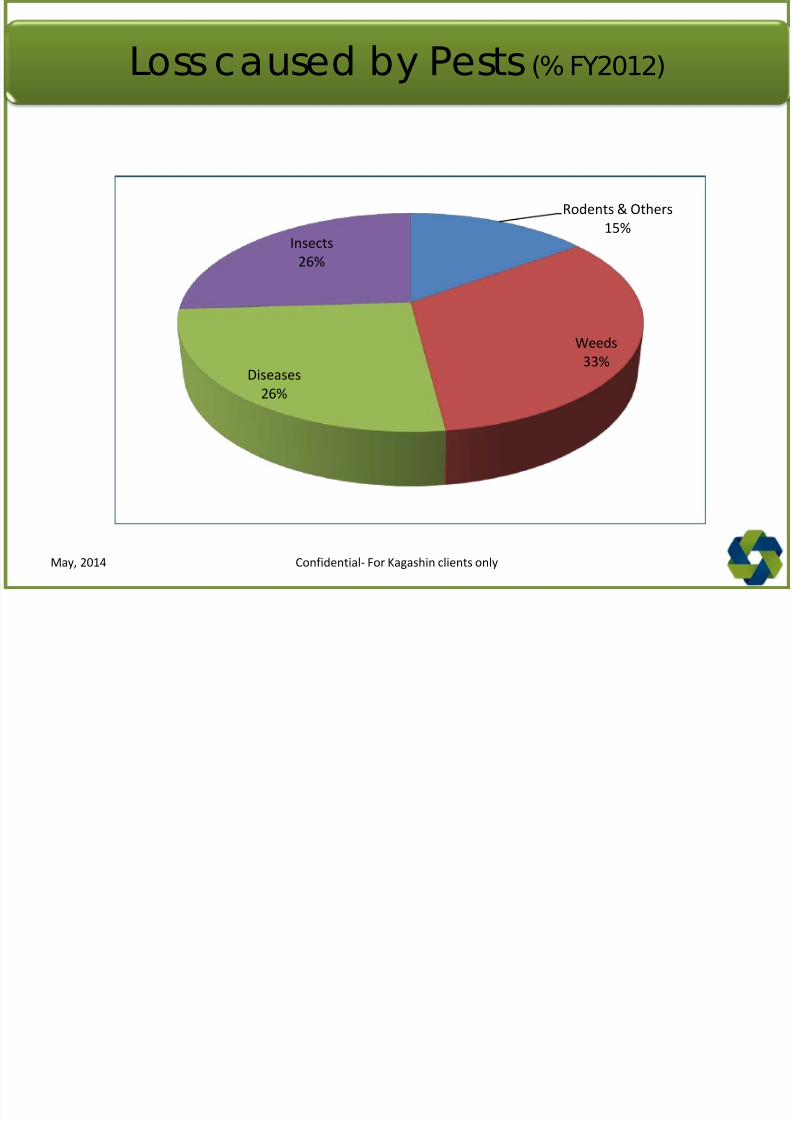

Loss caused by Pests (% FY2012)

Rodents & Others

15%

Weeds

33%Diseases

26%

Insects

26%

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 24/89

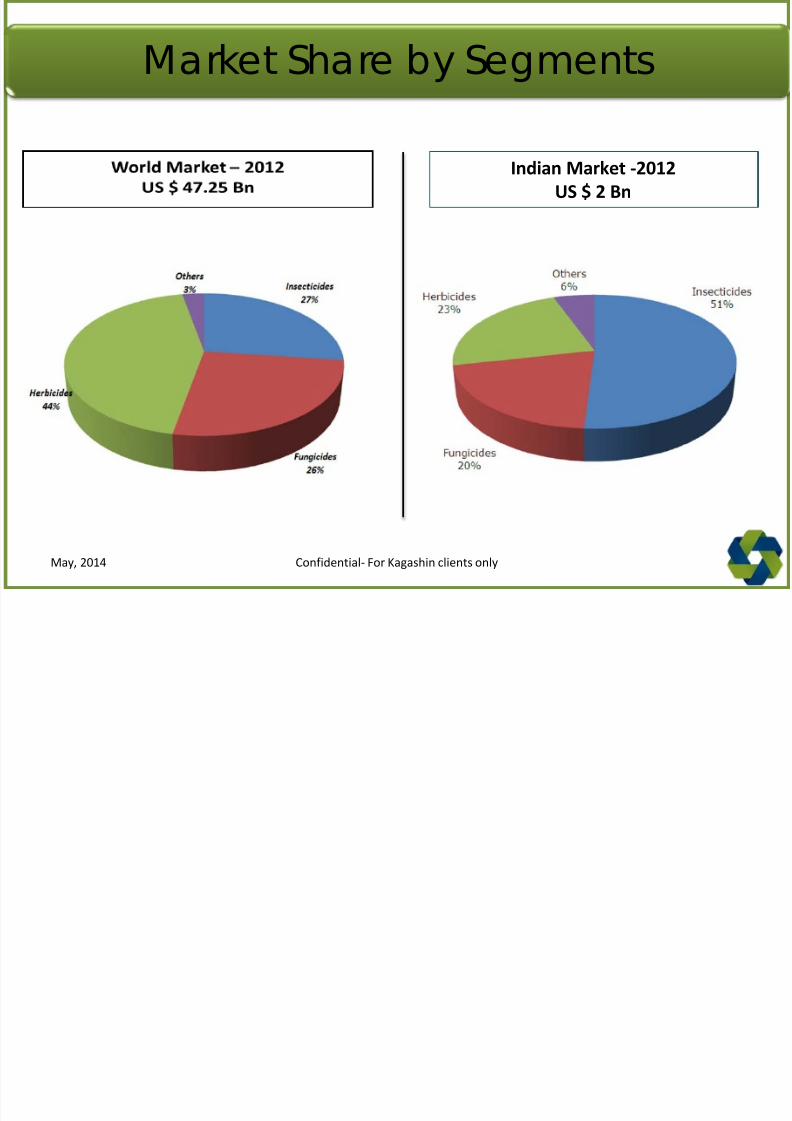

Market Share by Segments

Indian Market -2012

US $ 2 Bn

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 25/89

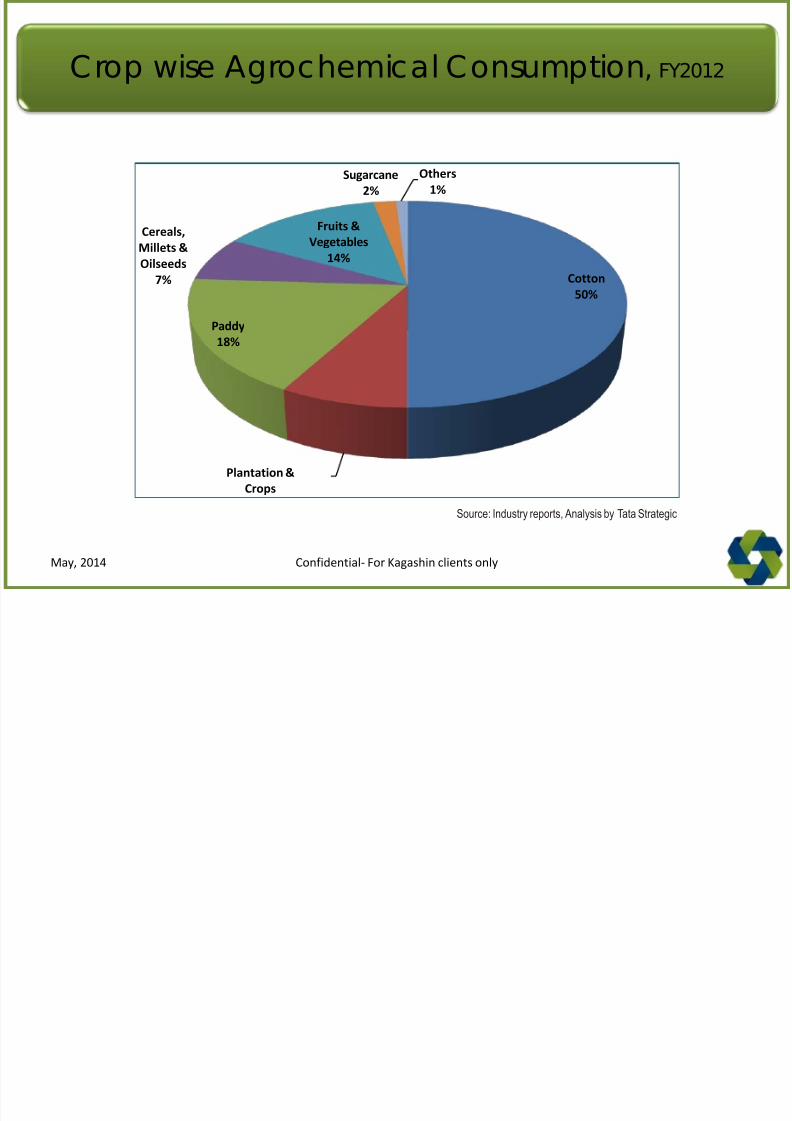

Crop wise Agrochemical Consumption, FY2012

Cotton50%

Plantation &

Crops

Paddy

18%

Cereals,

Millets &

Oilseeds

7%

Fruits &

Vegetables

14%

Sugarcane

2%

Others

1%

Source: Industry reports, Analysis by Tata Strategic

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 26/89

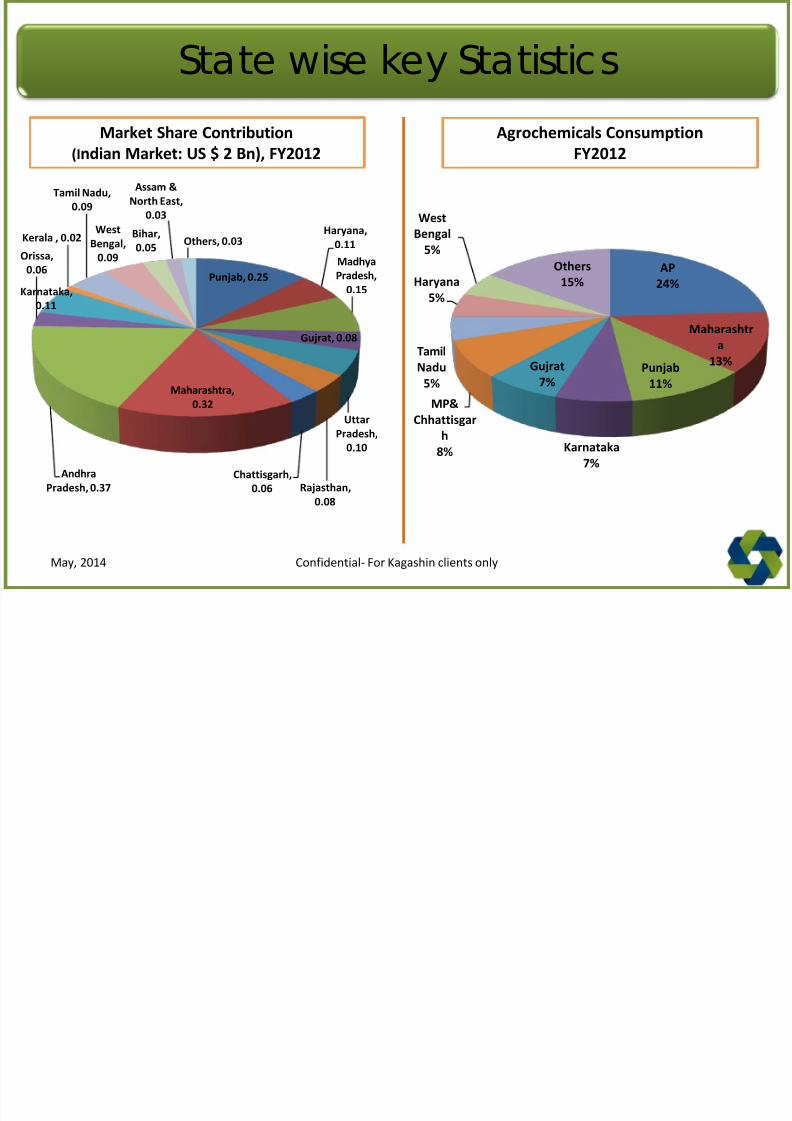

State wise key Statistics

Punjab, 0.25

Haryana,

0.11

Madhya

Pradesh,0.15

Gujrat, 0.08

UttarPradesh,

0.10

Rajasthan,

0.08

Chattisgarh,

0.06

Maharashtra,

0.32

Andhra

Pradesh, 0.37

Orissa,

0.06

Karnataka,

0.11

Kerala , 0.02

Tamil Nadu,

0.09

West

Bengal,

0.09

Bihar,

0.05

Assam &

North East,

0.03

Others, 0.03

AP

24%

Maharashtr

a

13%Punjab

11%

Karnataka

7%

Gujrat

7%

MP&

Chhattisgarh

8%

Tamil

Nadu

5%

Haryana5%

West

Bengal

5%

Others

15%

Agrochemicals Consumption

FY2012

Market Share Contribution

(Indian Market: US $ 2 Bn), FY2012

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 27/89

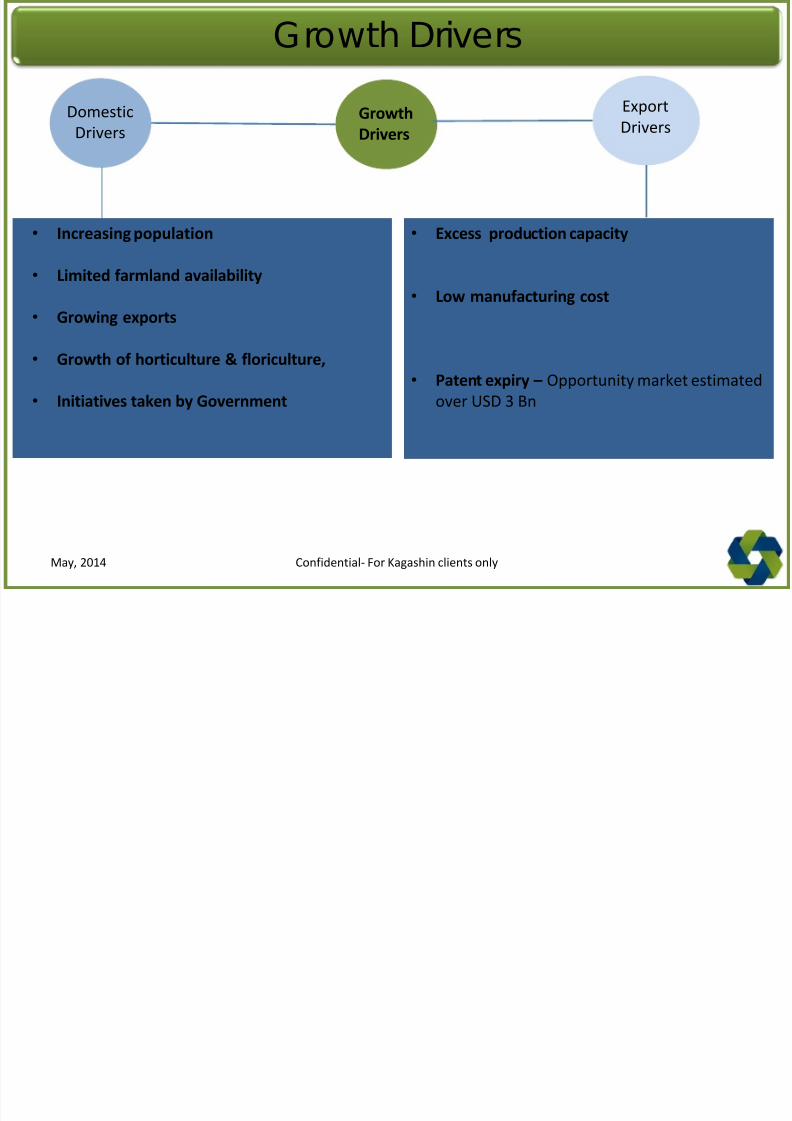

Growth Drivers

Growth

Drivers

Export

DriversDomestic

Drivers

• Excess production capacity

• Low manufacturing cost

• Patent expiry – Opportunity market estimated

over USD 3 Bn

• Increasing population

• Limited farmland availability

• Growing exports

• Growth of horticulture & floriculture,

• Initiatives taken by Government

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 28/89

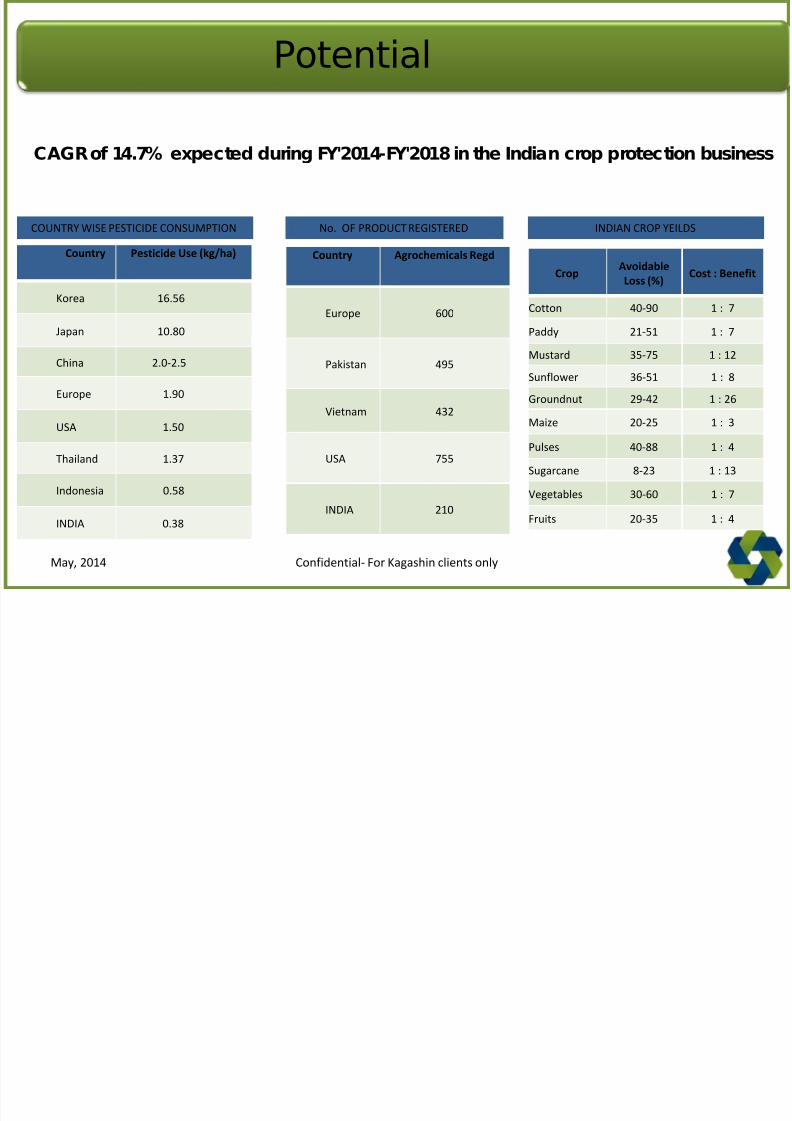

Potential

COUNTRY WISE PESTICIDE CONSUMPTION

Country Pesticide Use (kg/ha)

Korea 16.56

Japan 10.80

China 2.0-2.5

Europe 1.90

USA 1.50

Thailand 1.37

Indonesia 0.58

INDIA 0.38

Country Agrochemicals Regd

Europe 600

Pakistan 495

Vietnam 432

USA 755

INDIA 210

No. OF PRODUCT REGISTERED

CropAvoidable

Loss (%)Cost : Benefit

Cotton 40-90 1 : 7

Paddy 21-51 1 : 7

Mustard 35-75 1 : 12

Sunflower 36-51 1 : 8

Groundnut 29-42 1 : 26

Maize 20-25 1 : 3

Pulses 40-88 1 : 4

Sugarcane 8-23 1 : 13

Vegetables 30-60 1 : 7

Fruits 20-35 1 : 4

INDIAN CROP YEILDS

CAGR of 14.7% expected during FY'2014-FY'2018 in the Indian crop protection business

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 29/89

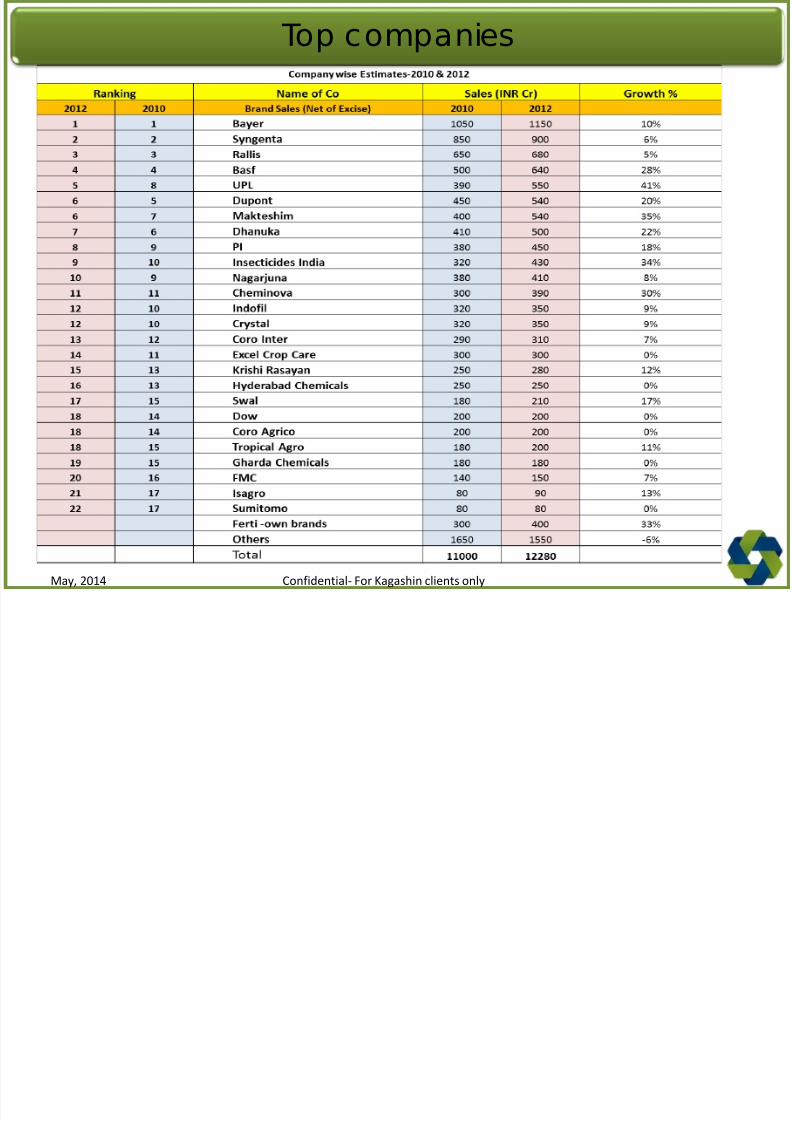

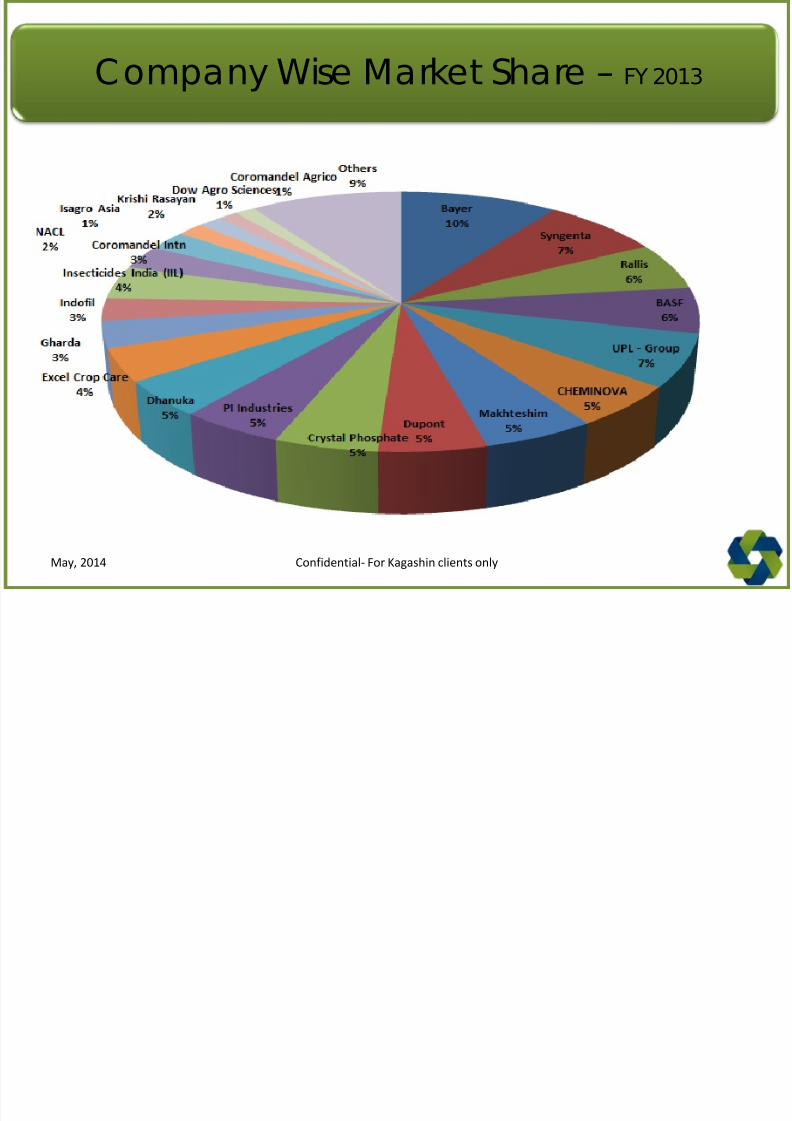

Top companies

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 30/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 31/89

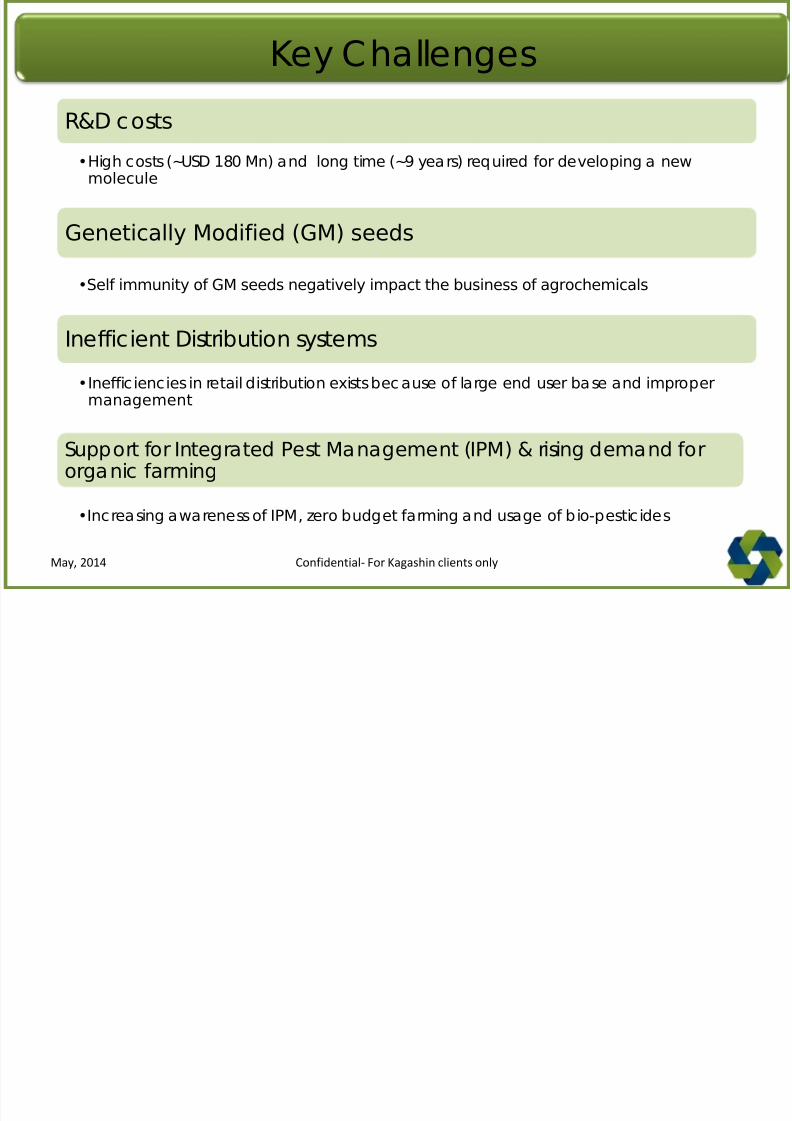

Key Challenges

R&D costs

•High costs (~USD 180 Mn) and long time (~9 years) required for developing a newmolecule

Genetically Modified (GM) seeds

•Self immunity of GM seeds negatively impact the business of agrochemicals

Inefficient Distribution systems

•Inefficiencies in retail distribution exists bec ause of large end user base and impropermanagement

Support for Integrated Pest Management (IPM) & rising demand fororganic farming

•Increasing awareness of IPM, zero budget farming and usage of bio-pesticides

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 32/89

Cyclical Nature of Demand

•More demand for agroc hemicals for kharif crops (~70% of annual consumption ofPesticides)

Increased Reliance on Exports

•C yclical nature ,declining demand, resulting in increase exports for better capacityutilization

Shift in Government Policies in Recent Years

•Stringent registration and export formalities of products delays growth of agrochemicals in

India

Longer period for registration of innovative products

•In India, registration of new products takes 3-5 years which discourages domesticmanufacturers

Key Challenges..Cont’d

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 33/89

INSECTICIDES, FUNGICIDES & HERBICIDES

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 34/89

Table of Contents

• Agriculture

- Overview

- Size

- Major Acreages

- Major Crops

- Growth drivers

- Major Issues

• Agrochemicals

- Overview

- Segments

- Consumption

- Growth Drivers

- Top Companies

- Key Challenges

• Seeds

- Overview

- Growth Drivers

- Production

- Current Status

- Total Cropped Area

- Field Crops: Hybrid Seed Market

- Vegetable Crops: Hybrid Seed

Market

- Impact of new technology

- Regulatory Framework &

Challenges

- Productivity Challenges

- Biotechnology & its effect- Way Forward

- Summary

Fertilizers-Overview

-Consumption

-Fertilizer – Indian Scenario

-Usage

-Efficiency

-Production-Imports

-Subsidy

-State Contribution

-Current Situation

-Growth Drivers

-Challenges

-Policies

Insecticides, Fungicides &

Herbicides- Demand Pattern In Indian Market

- Insecticides Market Share

- Fungicides Market Share

- Herbicides Market Share

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 35/89

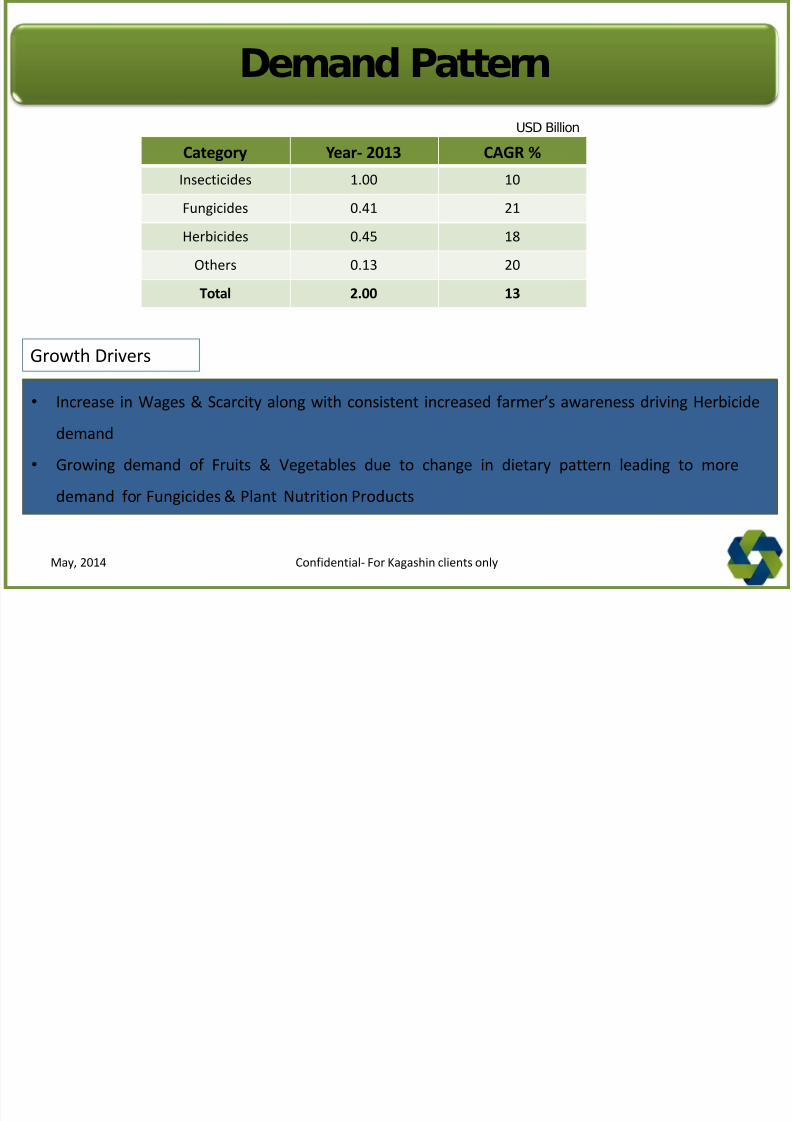

Demand Pattern

Category Year- 2013 CAGR %

Insecticides 1.00 10

Fungicides 0.41 21

Herbicides 0.45 18

Others 0.13 20

Total 2.00 13

USD Billion

• Increase in Wages & Scarcity along with consistent increased farmer’s awareness driving Herbicide

demand

• Growing demand of Fruits & Vegetables due to change in dietary pattern leading to more

demand for Fungicides & Plant Nutrition Products

Growth Drivers

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 36/89

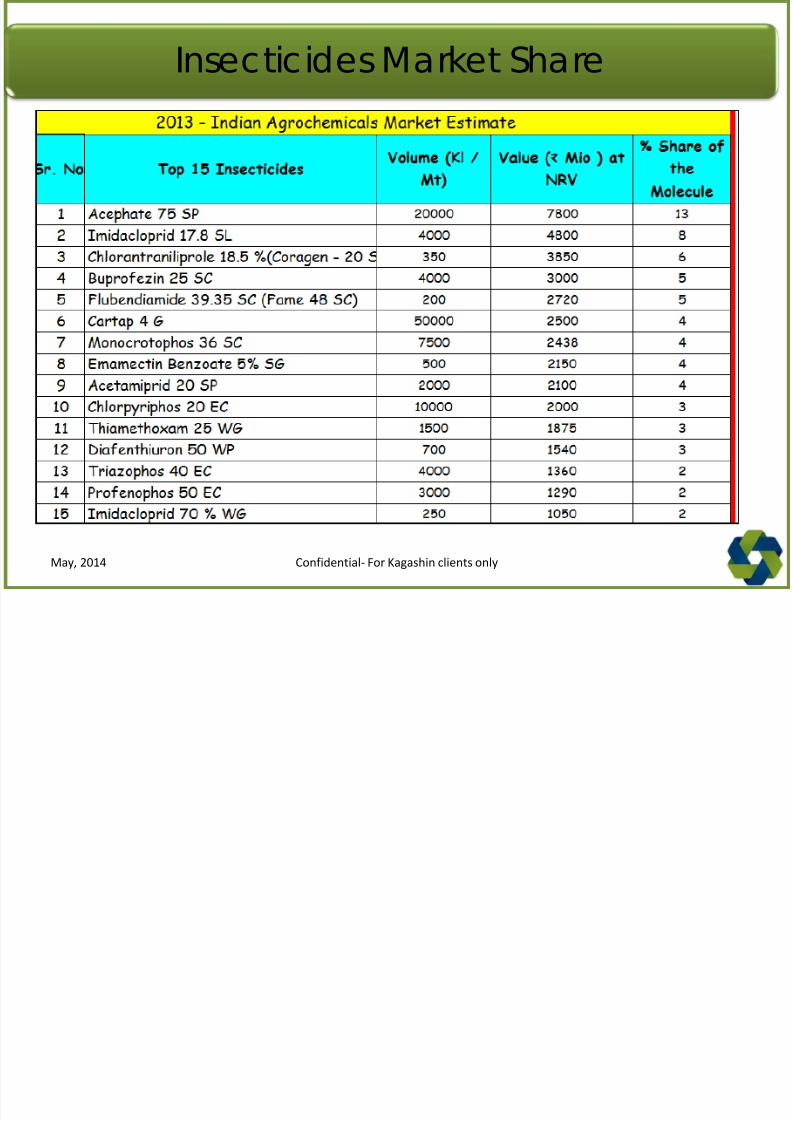

Insecticides Market Share

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 37/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 38/89

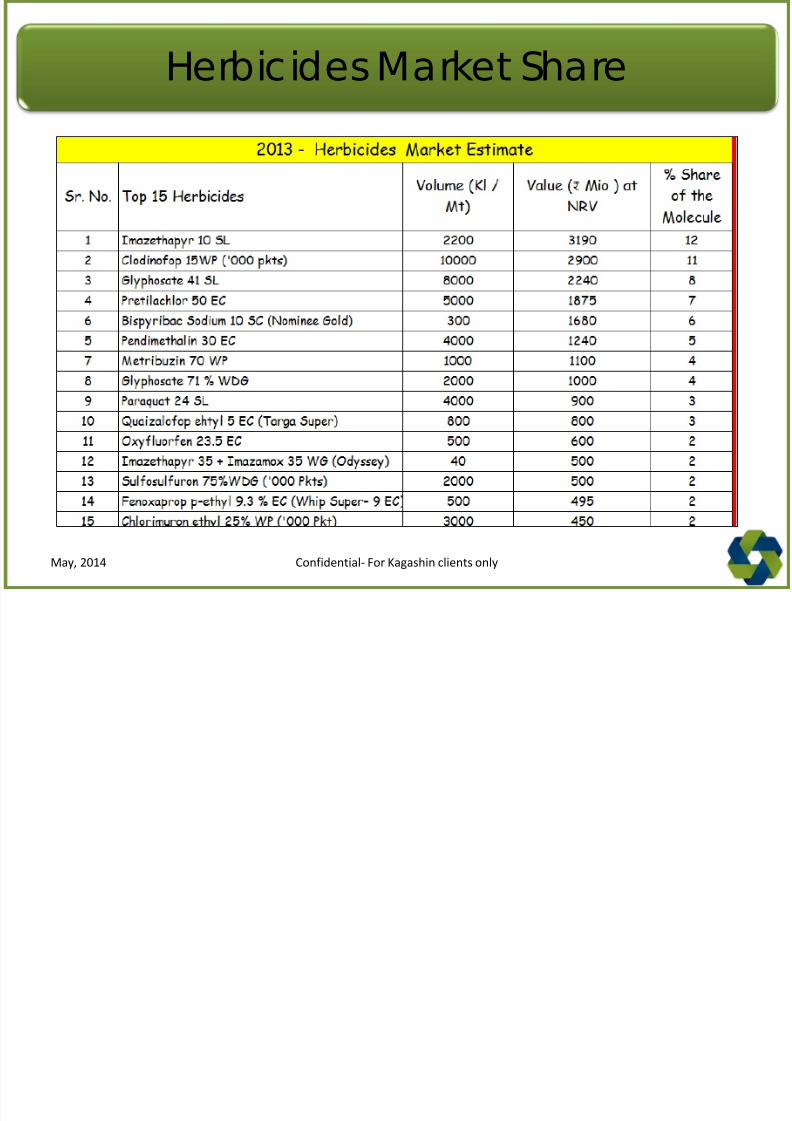

Herbicides Market Share

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 39/89

FERTILIZERS

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 40/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 41/89

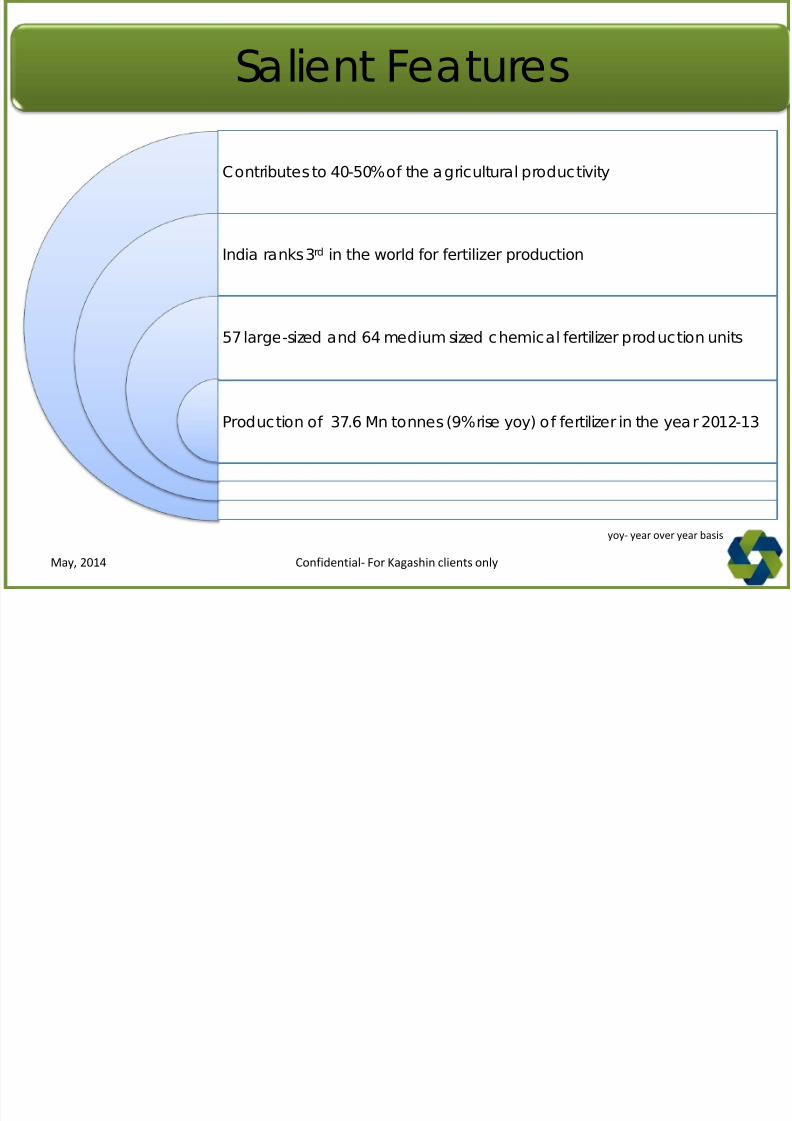

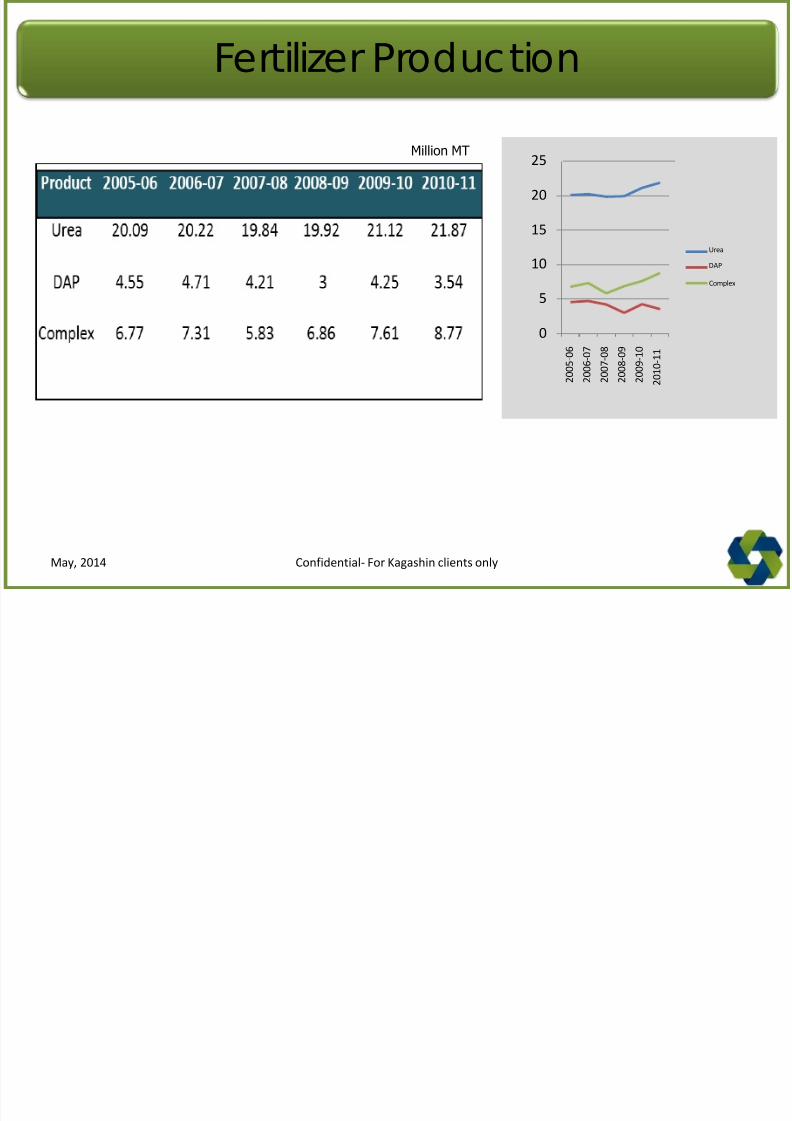

Salient Features

Contributes to 40-50% of the agricultural productivity

India ranks 3rd in the world for fertilizer production

57 large-sized and 64 medium sized chemical fertilizer production units

Production of 37.6 Mn tonnes (9% rise yoy) of fertilizer in the year 2012-13

yoy- year over year basis

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 42/89

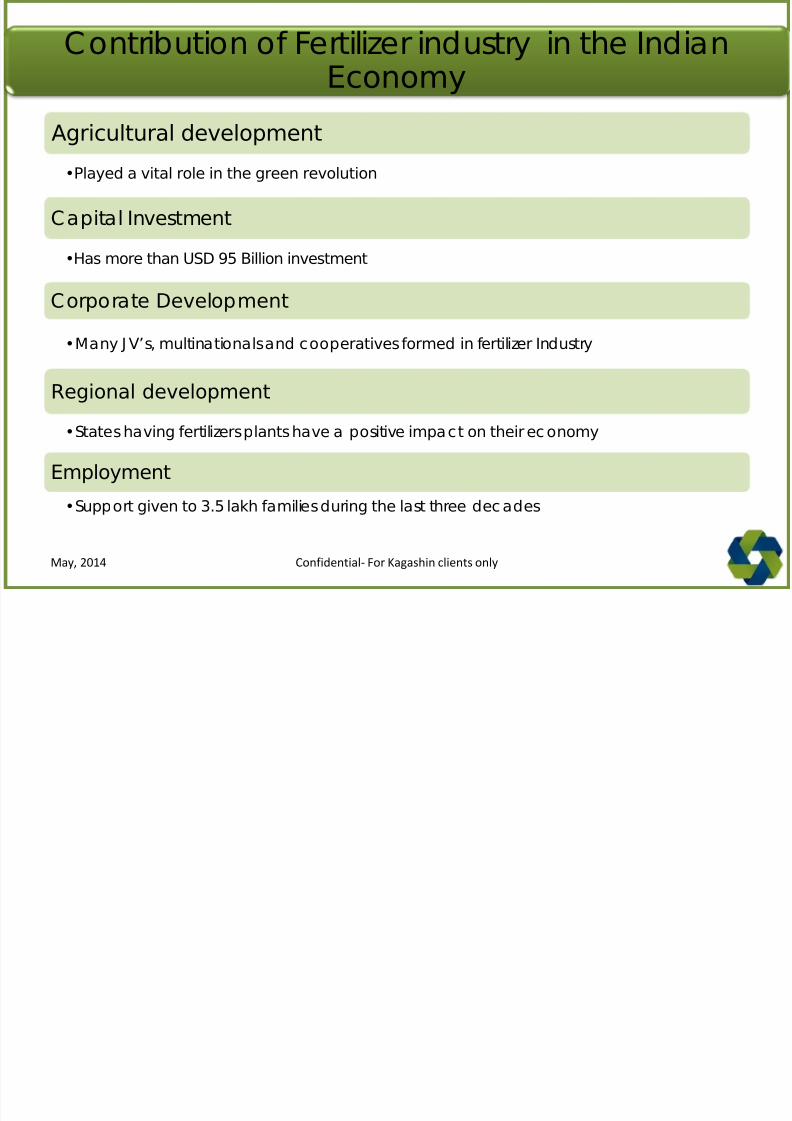

Contribution of Fertilizer industry in the IndianEconomy

Agricultural development•Played a vital role in the green revolution

Capital Investment

•Has more than USD 95 Billion investment

Corporate Development

•Many J V’s, multinationals and cooperatives formed in fertilizer Industry

Regional development

•States having fertilizers plants have a positive impact on their ec onomy

Employment

•Support given to 3.5 lakh families during the last three dec ades

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 43/89

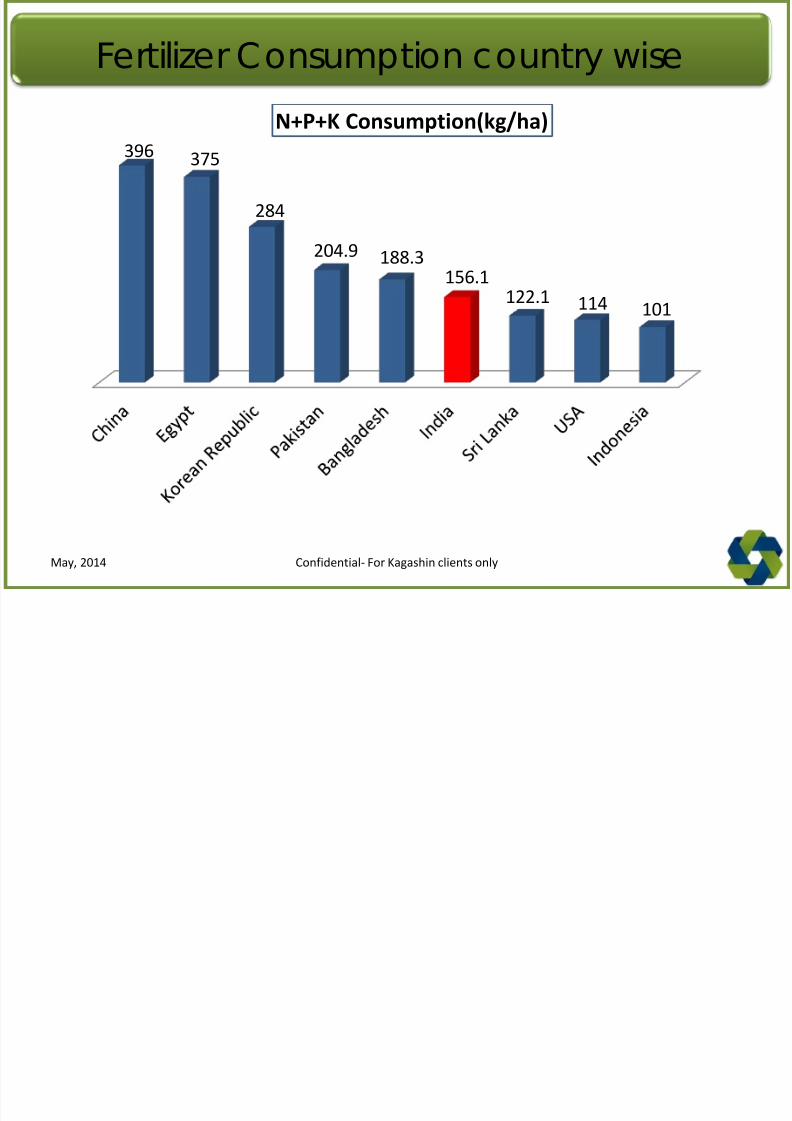

Fertilizer Consumption country wise

396 375

284

204.9 188.3

156.1 122.1 114 101

N+P+K Consumption(kg/ha)

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 44/89

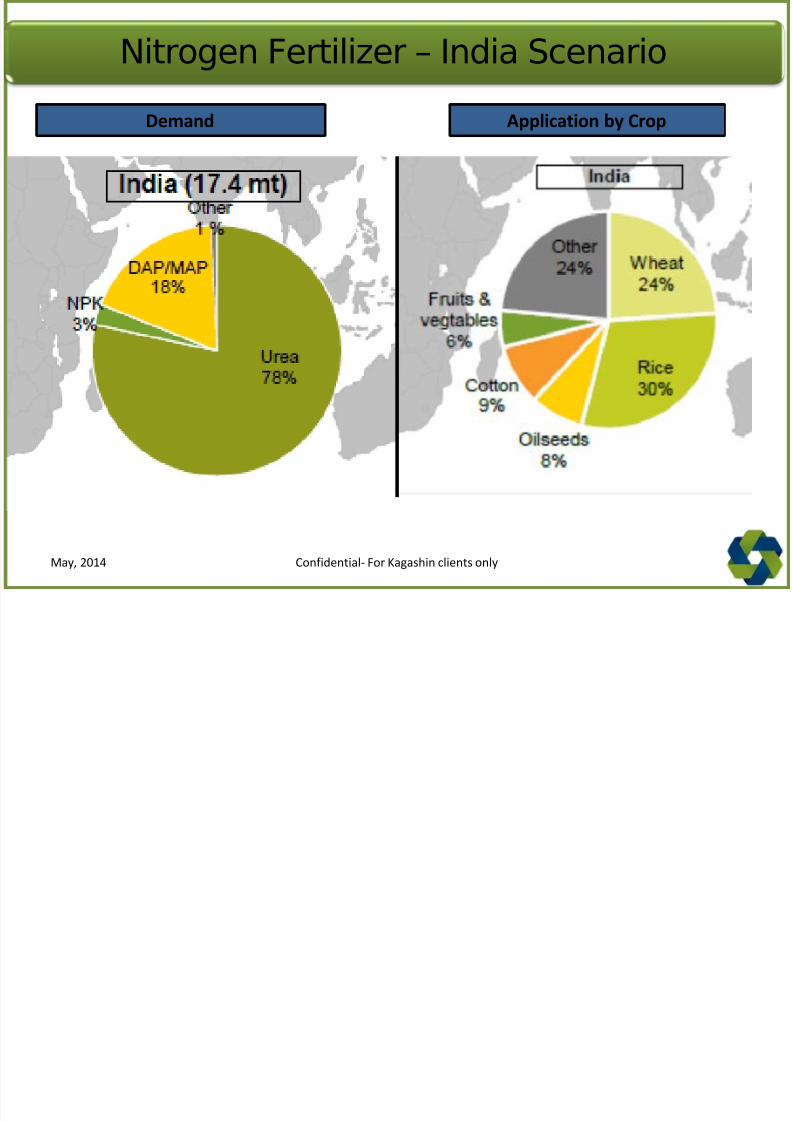

Nitrogen Fertilizer – India Scenario

Demand Application by Crop

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 45/89

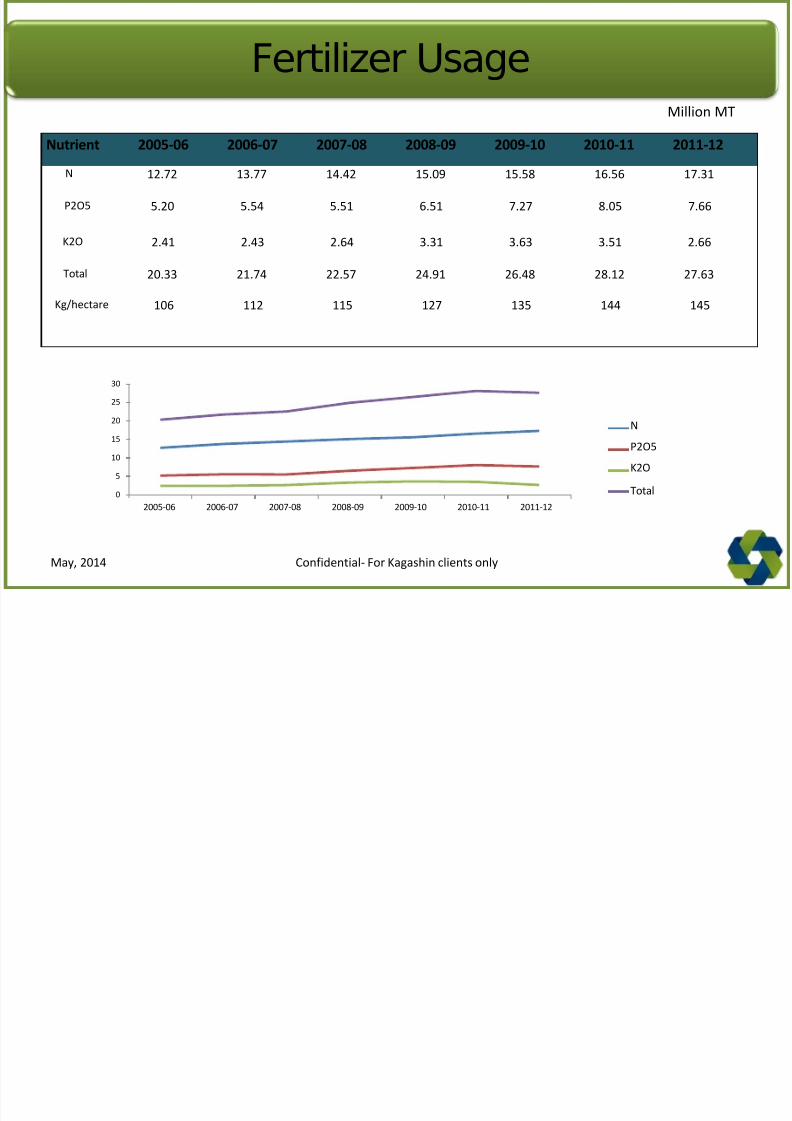

Fertilizer Usage

0

5

10

15

20

30

25

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

N

P2O5

K2O

Total

Million MT

Nutrient 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

N 12.72 13.77 14.42 15.09 15.58 16.56 17.31

P2O5 5.20 5.54 5.51 6.51 7.27 8.05 7.66

K2O 2.41 2.43 2.64 3.31 3.63 3.51 2.66

Total 20.33 21.74 22.57 24.91 26.48 28.12 27.63

Kg/hectare 106 112 115 127 135 144 145

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 46/89

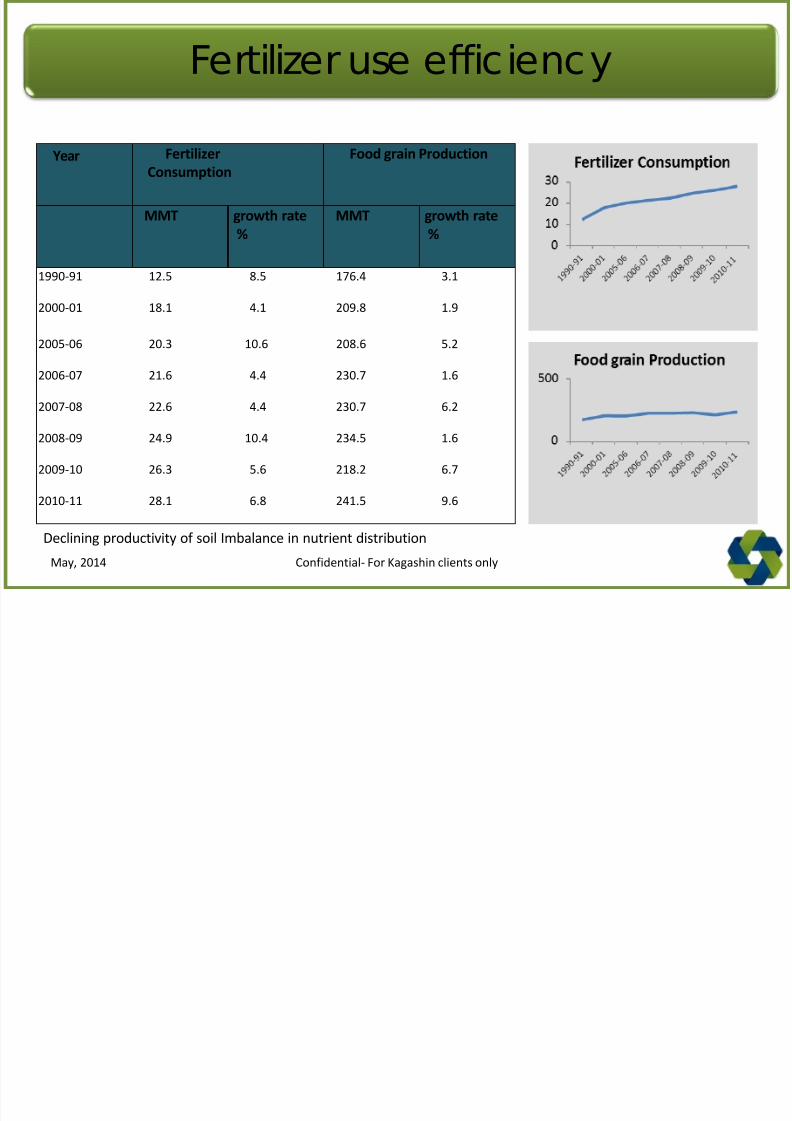

Fertilizer use efficiency

Year Fertilizer

Consumption

Food grain Production

MMT growth rate

%

MMT growth rate

%

1990-91 12.5 8.5 176.4 3.1

2000-01 18.1 4.1 209.8 1.9

2005-06 20.3 10.6 208.6 5.2

2006-07 21.6 4.4 230.7 1.6

2007-08 22.6 4.4 230.7 6.2

2008-09 24.9 10.4 234.5 1.6

2009-10 26.3 5.6 218.2 6.7

2010-11 28.1 6.8 241.5 9.6

Declining productivity of soil Imbalance in nutrient distribution

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 47/89

Fertilizer Production

Complex

5

0

10

25

20

15

2 0 0 5 - 0 6

2 0 0 6 - 0 7

2 0 0 7 - 0 8

2 0 0 8 - 0 9

2 0 0 9 - 1 0

2 0 1 0 - 1 1

Urea

DAP

Million MT

Confidential- For Kagashin clients onlyMay, 2014

I

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 48/89

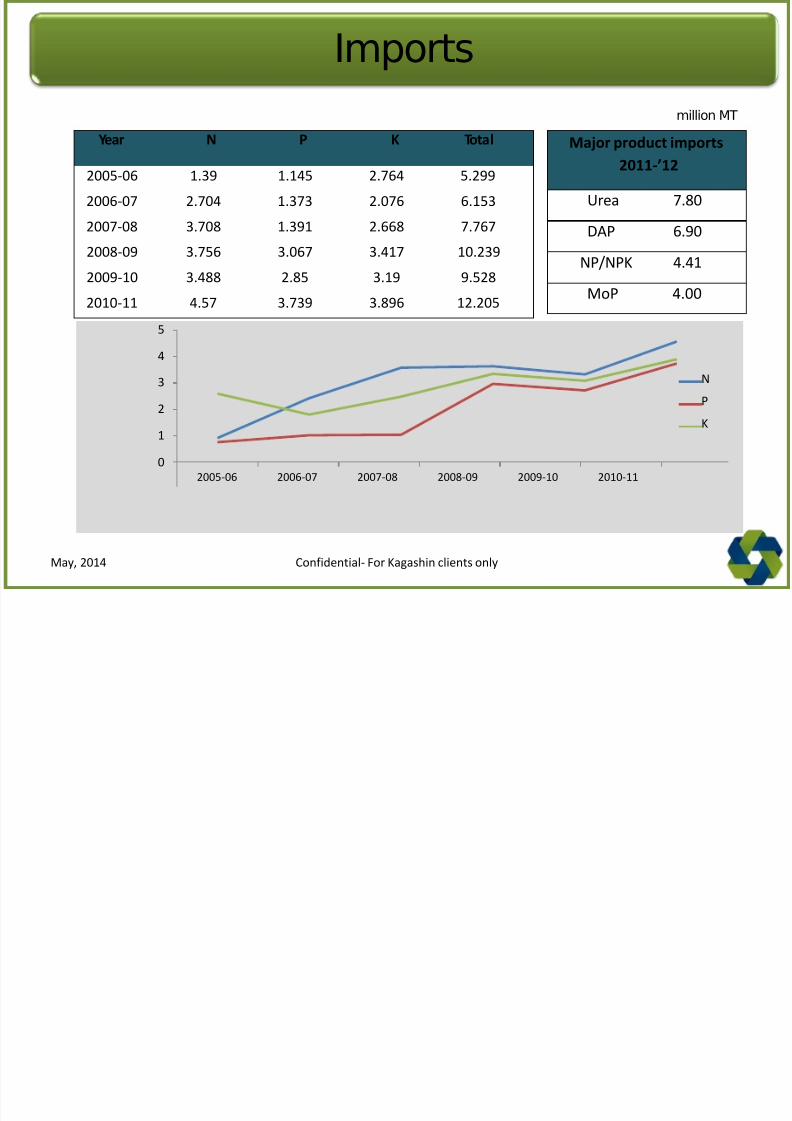

Imports

3

2

1

0

5

4

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

N

P

K

Year N P K Total

2005-06 1.39 1.145 2.764 5.299

2006-07 2.704 1.373 2.076 6.153

2007-08 3.708 1.391 2.668 7.767

2008-09 3.756 3.067 3.417 10.239

2009-10 3.488 2.85 3.19 9.5282010-11 4.57 3.739 3.896 12.205

Major product imports2011-’12

Urea 7.80

DAP 6.90

NP/NPK 4.41

MoP 4.00

million MT

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 49/89

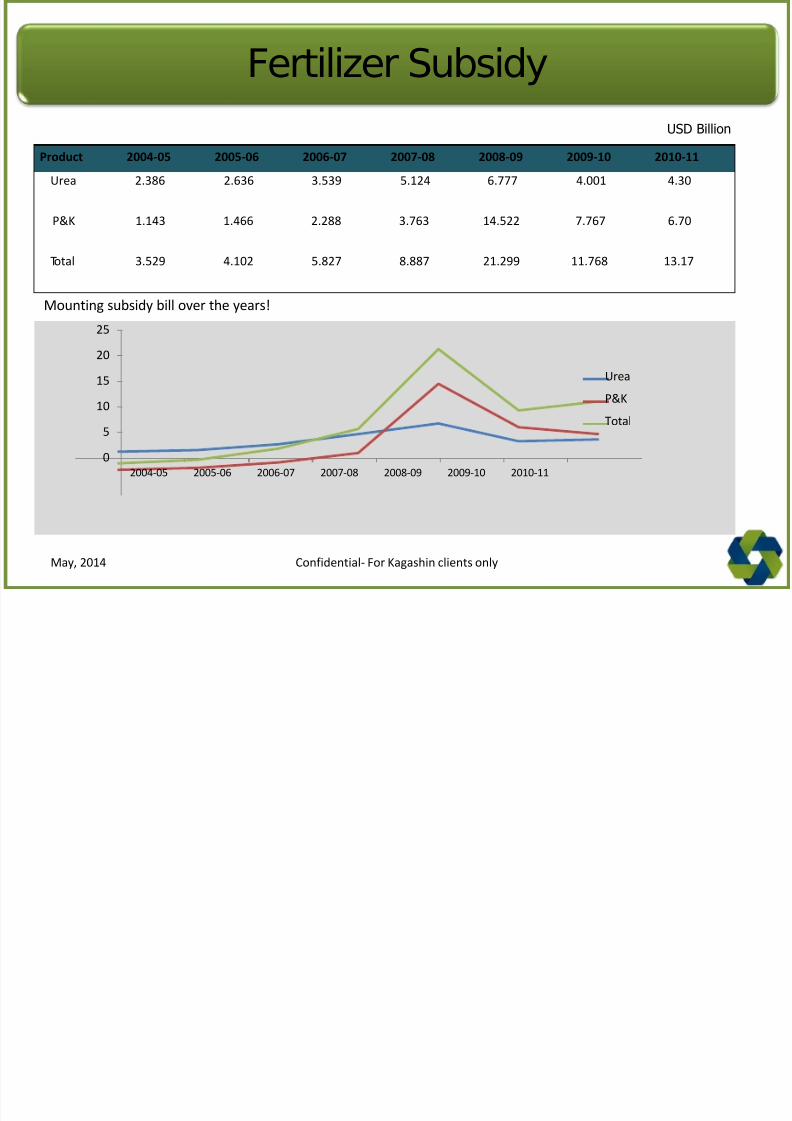

Fertilizer Subsidy

Mounting subsidy bill over the years!

25

20

15

10

5

0

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Urea

P&K

Total

Product 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Urea 2.386 2.636 3.539 5.124 6.777 4.001 4.30

P&K 1.143 1.466 2.288 3.763 14.522 7.767 6.70

Total 3.529 4.102 5.827 8.887 21.299 11.768 13.17

USD Billion

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 50/89

Objectives laid down for sector growth

• Expansion and efficiency enhancement through revamping of existing fertilizer plants

• Setting up JV projects in countries having abundant and cheaper raw material resources

• Exploring the use of alternative energy sources like liquefied natural gas, coal gasification,

etc. to overcome the constraints in the availability of conventional energy sources

• Looking at possibilities of revival of some of the closed units by setting up Brownfield units

subject to availability of gas

Source: Ministry of Chemicals & Fertilizers, India

Confidential- For Kagashin clients onlyMay, 2014

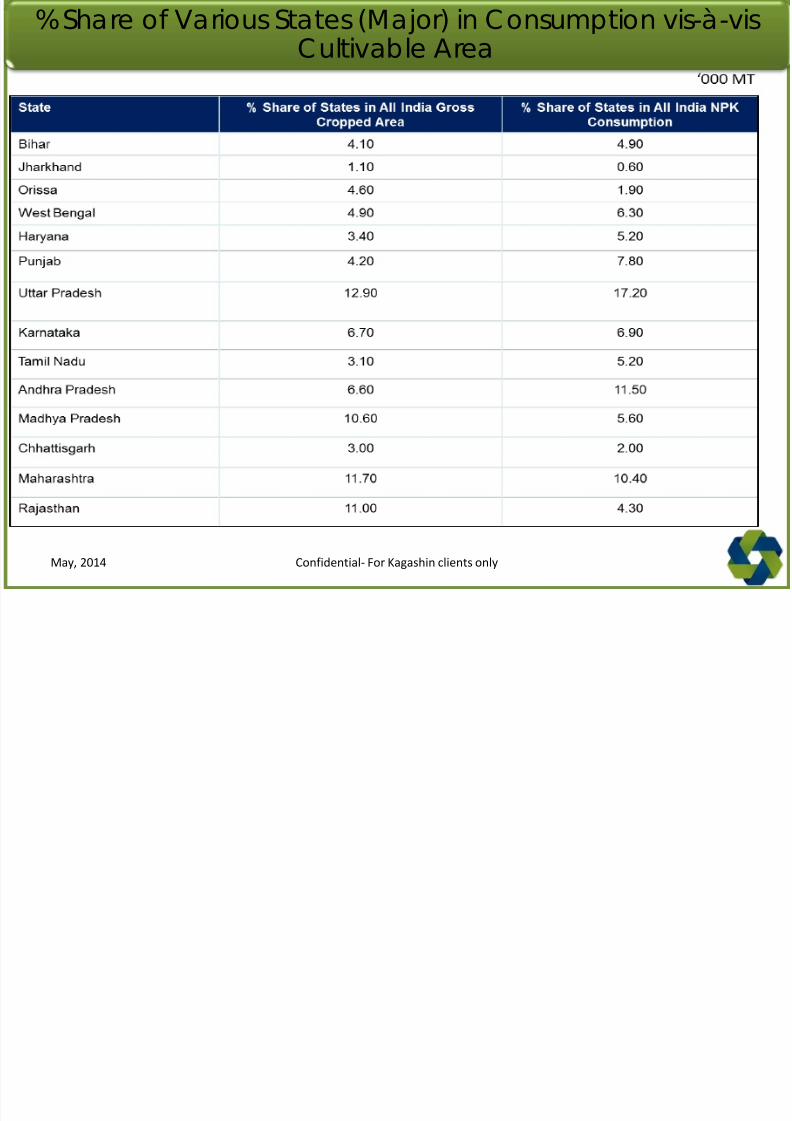

% Share of Various States (Major) in Consumption vis-à-vis

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 51/89

Cultivable Area

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 52/89

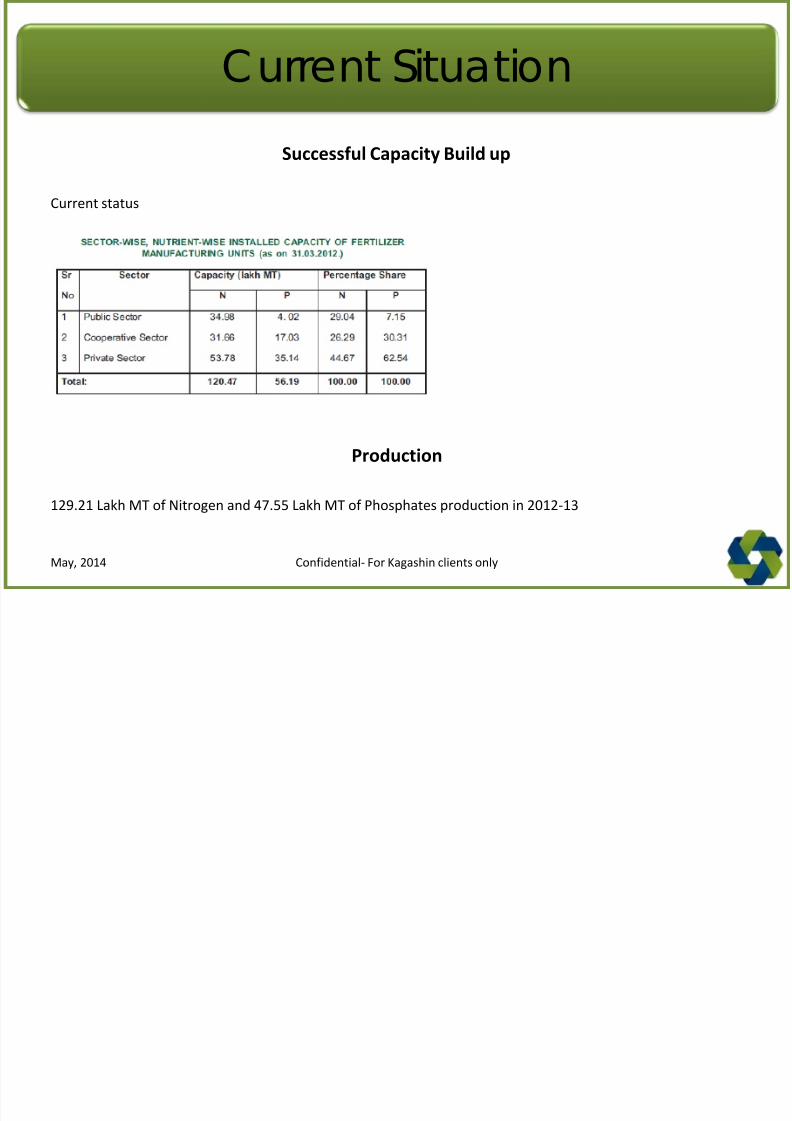

Current Situation

Successful Capacity Build up

Current status

Production

129.21 Lakh MT of Nitrogen and 47.55 Lakh MT of Phosphates production in 2012-13

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 53/89

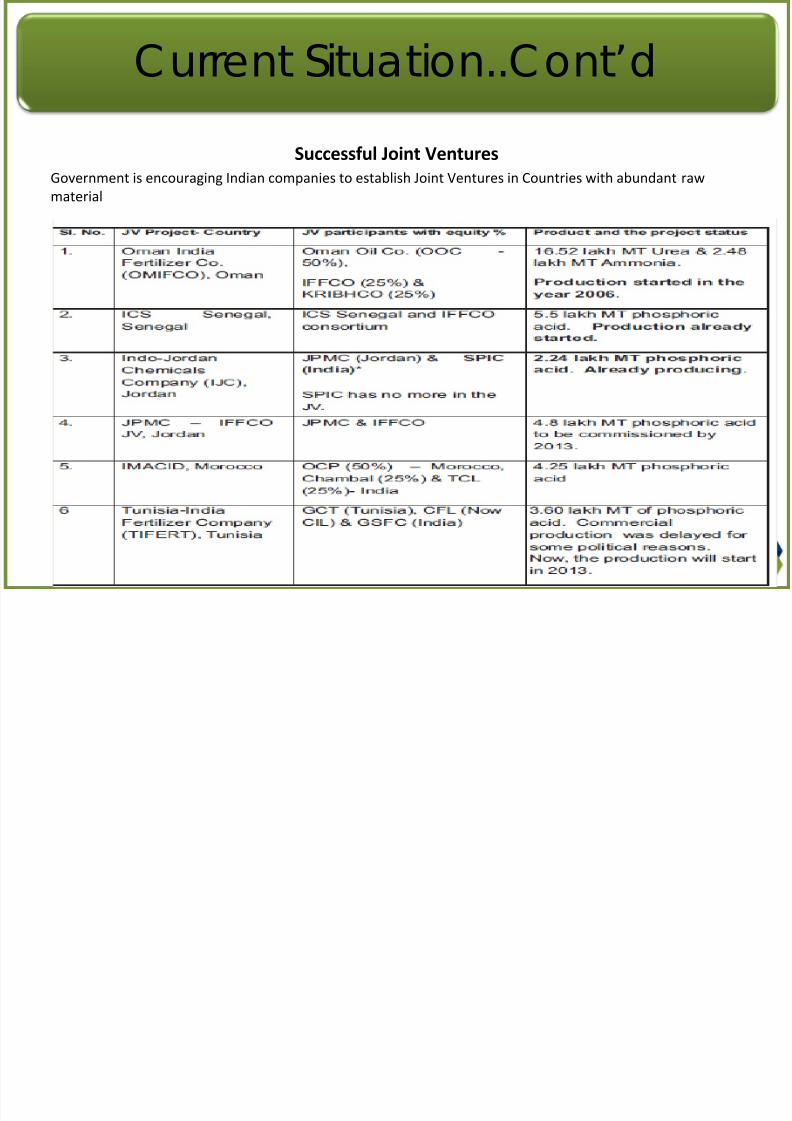

Successful Joint VenturesGovernment is encouraging Indian companies to establish Joint Ventures in Countries with abundant raw

material

Current Situation..Cont’d

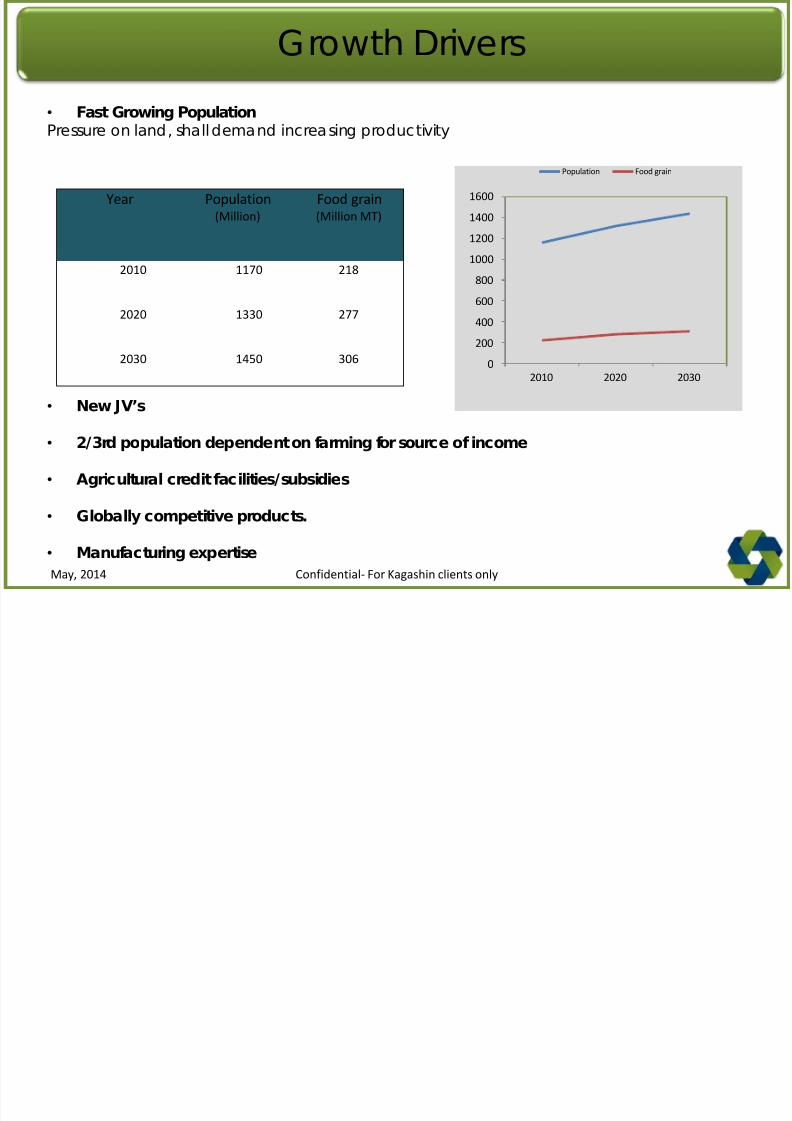

Growth Drivers

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 54/89

Growth Drivers

• Fast Growing PopulationPressure on land, shall demand increasing productivity

• New JV’s

• 2/3rd population dependent on farming for source of income

• Agricultural credit facilities/subsidies

• Globally competitive products.

• Manufacturing expertise

Year Population(Million)

Food grain(Million MT)

2010 1170 218

2020 1330 277

2030 1450 306

1600

1400

1200

1000

800600

400

200

02010 2020 2030

Population Food grain

Confidential- For Kagashin clients onlyMay, 2014

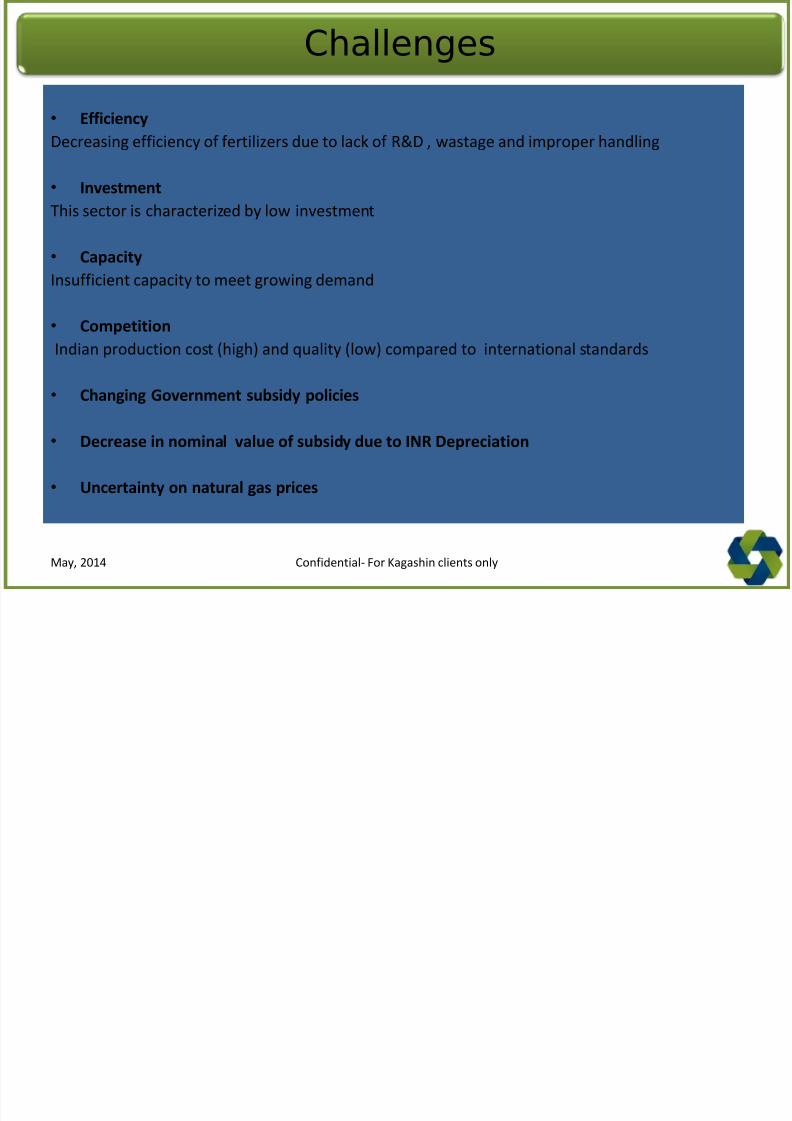

Challenges

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 55/89

Challenges

• Efficiency

Decreasing efficiency of fertilizers due to lack of R&D , wastage and improper handling

• Investment

This sector is characterized by low investment

• Capacity

Insufficient capacity to meet growing demand

• Competition

Indian production cost (high) and quality (low) compared to international standards

• Changing Government subsidy policies

• Decrease in nominal value of subsidy due to INR Depreciation

• Uncertainty on natural gas prices

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 56/89

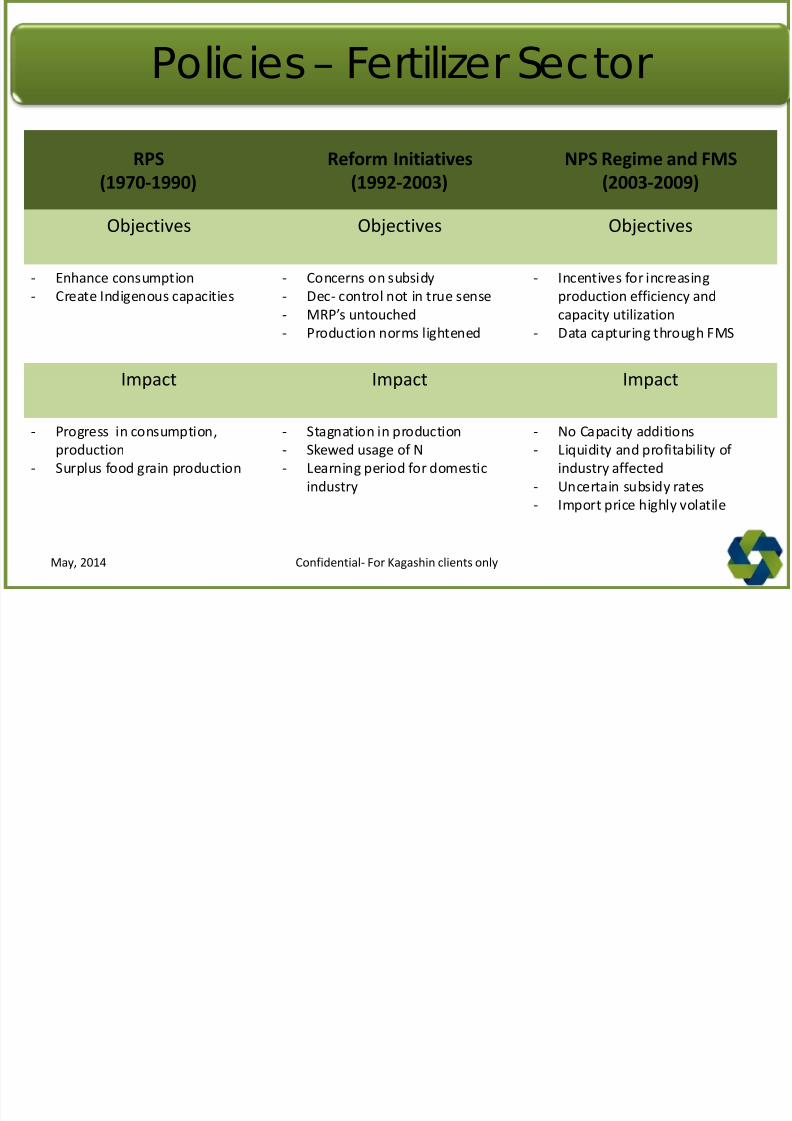

Policies – Fertilizer Sector

RPS

(1970-1990)

Reform Initiatives

(1992-2003)

NPS Regime and FMS

(2003-2009)

Objectives Objectives Objectives

- Enhance consumption- Create Indigenous capacities - Concerns on subsidy- Dec- control not in true sense

- MRP’s untouched

- Production norms lightened

- Incentives for increasingproduction efficiency and

capacity utilization

- Data capturing through FMS

Impact Impact Impact

- Progress in consumption,

production

- Surplus food grain production

- Stagnation in production

- Skewed usage of N

- Learning period for domestic

industry

- No Capacity additions

- Liquidity and profitability of

industry affected

- Uncertain subsidy rates

- Import price highly volatile

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 57/89

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 58/89

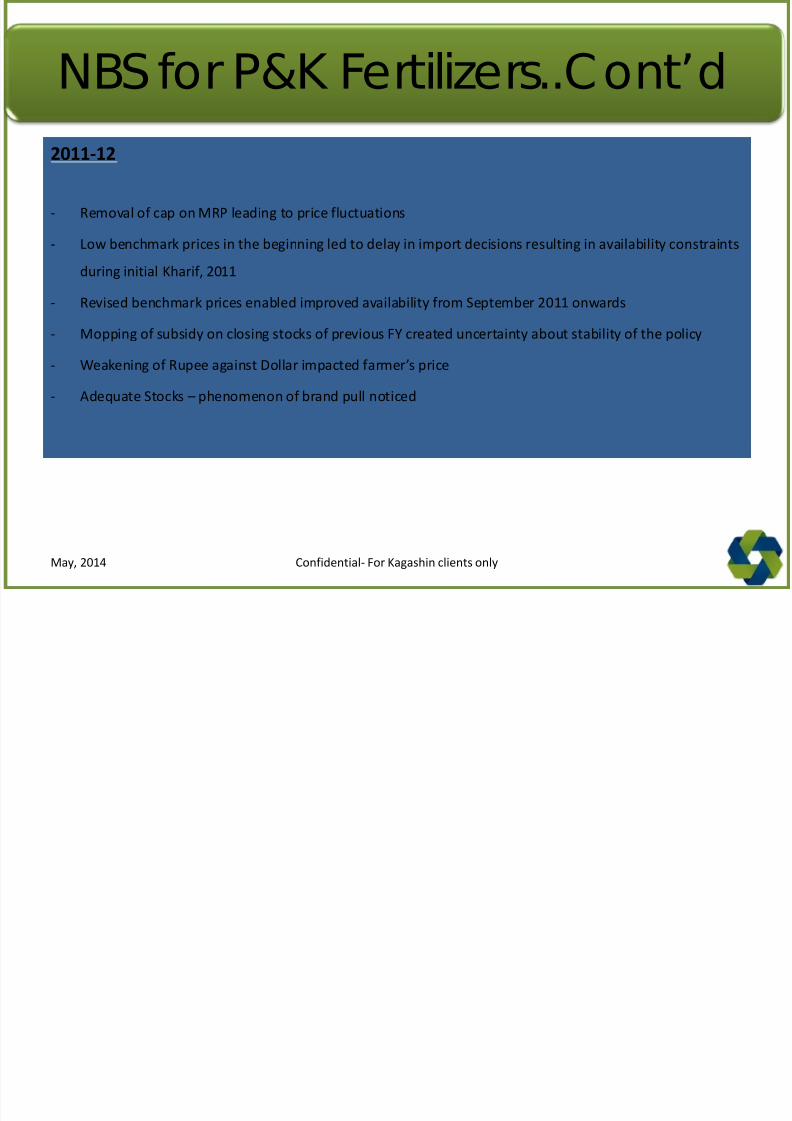

NBS for P&K Fertilizers..Cont’d

2011-12

- Removal of cap on MRP leading to price fluctuations

- Low benchmark prices in the beginning led to delay in import decisions resulting in availability constraints

during initial Kharif, 2011

- Revised benchmark prices enabled improved availability from September 2011 onwards

- Mopping of subsidy on closing stocks of previous FY created uncertainty about stability of the policy

- Weakening of Rupee against Dollar impacted farmer’s price

- Adequate Stocks – phenomenon of brand pull noticed

Confidential- For Kagashin clients onlyMay, 2014

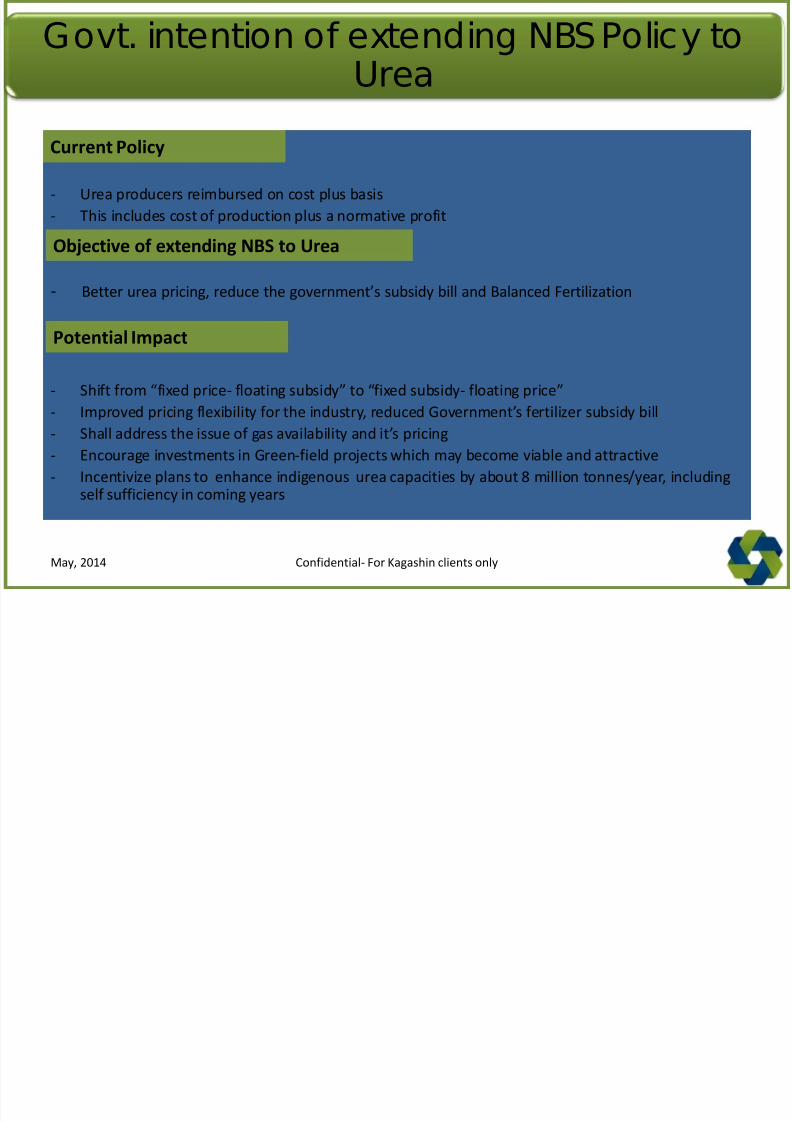

Govt intention of extending NBSPolicy to

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 59/89

Govt. intention of extending NBS Policy toUrea

- Urea producers reimbursed on cost plus basis

- This includes cost of production plus a normative profit

- Better urea pricing, reduce the government’s subsidy bill and Balanced Fertilization

- Shift from “fixed price- floating subsidy” to “fixed subsidy- floating price”

- Improved pricing flexibility for the industry, reduced Government’s fertilizer subsidy bill

- Shall address the issue of gas availability and it’s pricing

- Encourage investments in Green-field projects which may become viable and attractive

- Incentivize plans to enhance indigenous urea capacities by about 8 million tonnes/year, includingself sufficiency in coming years

Objective of extending NBS to Urea

Current Policy

Potential Impact

Confidential- For Kagashin clients onlyMay, 2014

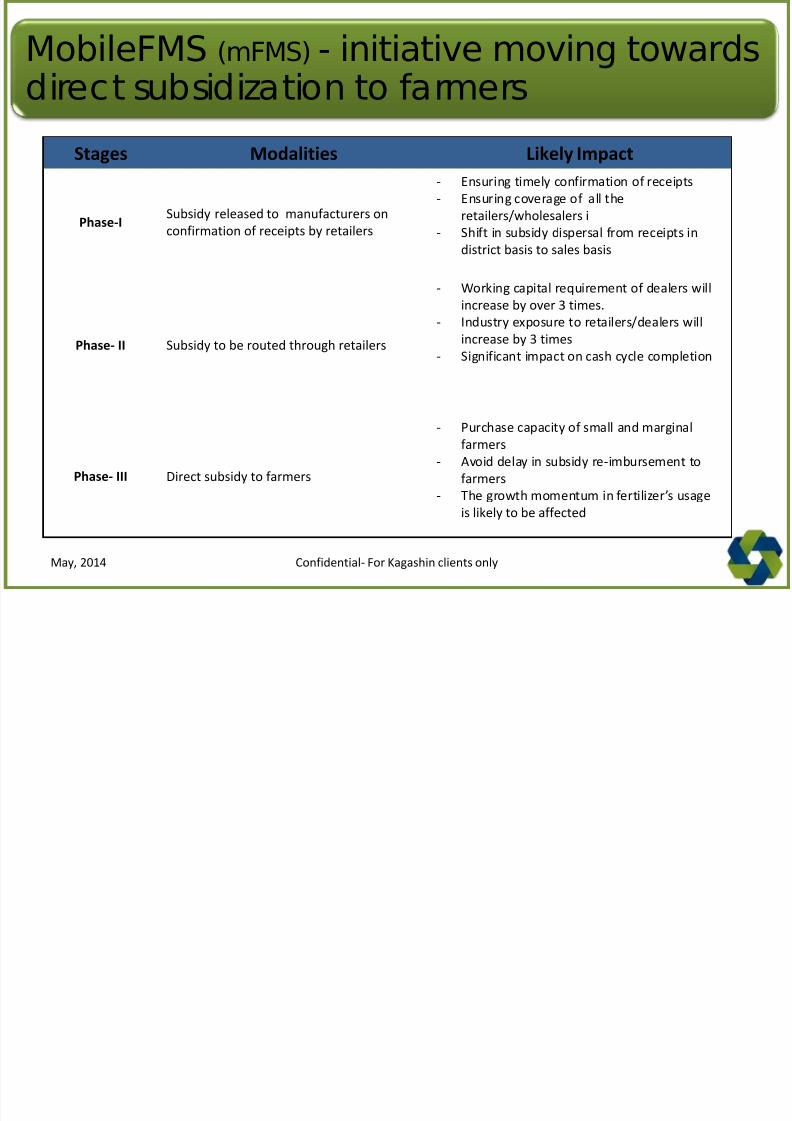

MobileFMS ( FMS) initiative moving towards

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 60/89

MobileFMS (mFMS) - initiative moving towardsdirect subsidization to farmers

Stages Modalities Likely Impact

Phase-ISubsidy released to manufacturers on

confirmation of receipts by retailers

- Ensuring timely confirmation of receipts

- Ensuring coverage of all the

retailers/wholesalers i

- Shift in subsidy dispersal from receipts in

district basis to sales basis

Phase- II Subsidy to be routed through retailers

- Working capital requirement of dealers willincrease by over 3 times.

- Industry exposure to retailers/dealers will

increase by 3 times

- Significant impact on cash cycle completion

Phase- III Direct subsidy to farmers

- Purchase capacity of small and marginalfarmers

- Avoid delay in subsidy re-imbursement to

farmers

- The growth momentum in fertilizer’s usage

is likely to be affected

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 61/89

Table of Contents

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 62/89

Table of Contents

• Agriculture

- Overview

- Size

- Major Acreages

- Major Crops

- Growth drivers

- Major Issues

• Agrochemicals

- Overview

- Segments

- Consumption

- Growth Drivers

- Top Companies- Key Challenges

• Insecticides, Fungicides &

Herbicides- Demand Pattern In Indian Market

- Insecticides Market Share

- Fungicides Market Share

- Herbicides Market Share

• Fertilizers- Overview

- Consumption

- Fertilizer – Indian Scenario

- Usage

- Efficiency

- Production

- Imports

- Subsidy

- State Contribution

- Current Situation

- Growth Drivers

- Challenges

- Policies

• Seeds

- Overview

- Growth Drivers

- Production

- Current Status

- Total Cropped Area

- Field Crops: Hybrid Seed Market

- Vegetable Crops: Hybrid SeedMarket

- Impact of new technology

- Regulatory Framework &

Challenges

- Productivity Challenges

- Biotechnology & its effect

- Way Forward

- Summary

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 63/89

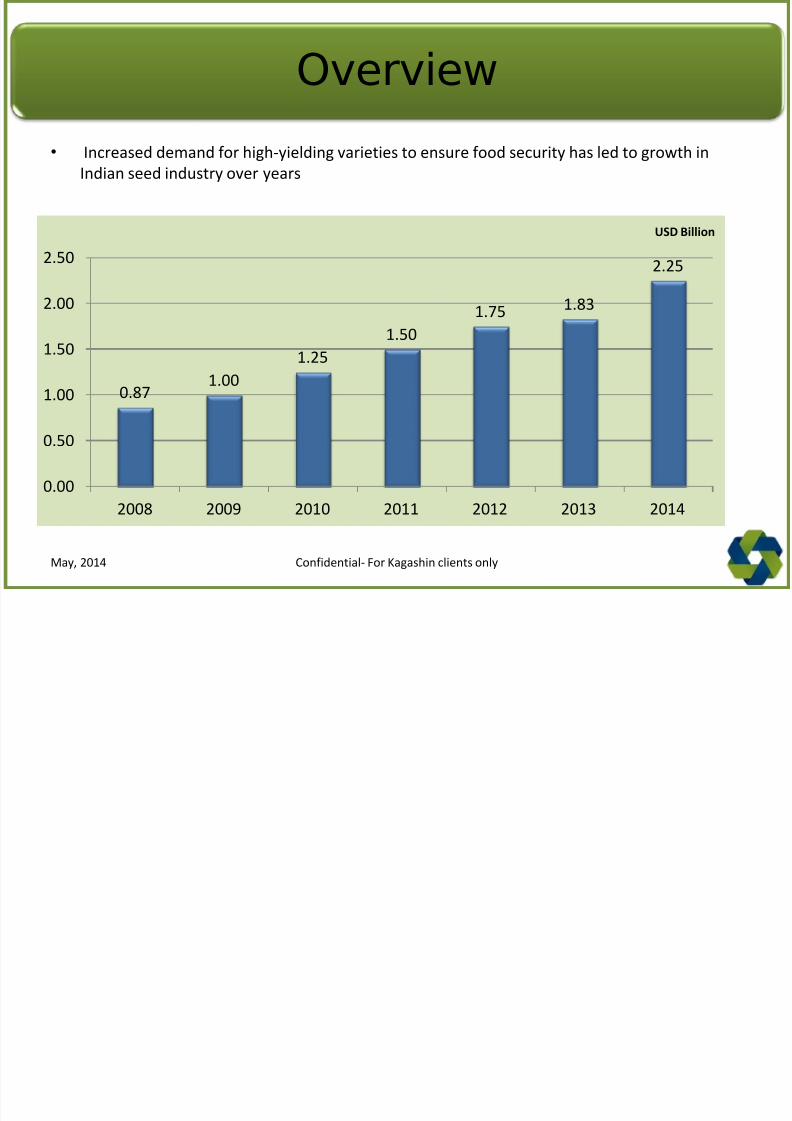

Overview

• Increased demand for high-yielding varieties to ensure food security has led to growth inIndian seed industry over years

0.871.00

1.25

1.50

1.75 1.83

2.25

0.00

0.50

1.00

1.50

2.00

2.50

2008 2009 2010 2011 2012 2013 2014

USD Billion

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 64/89

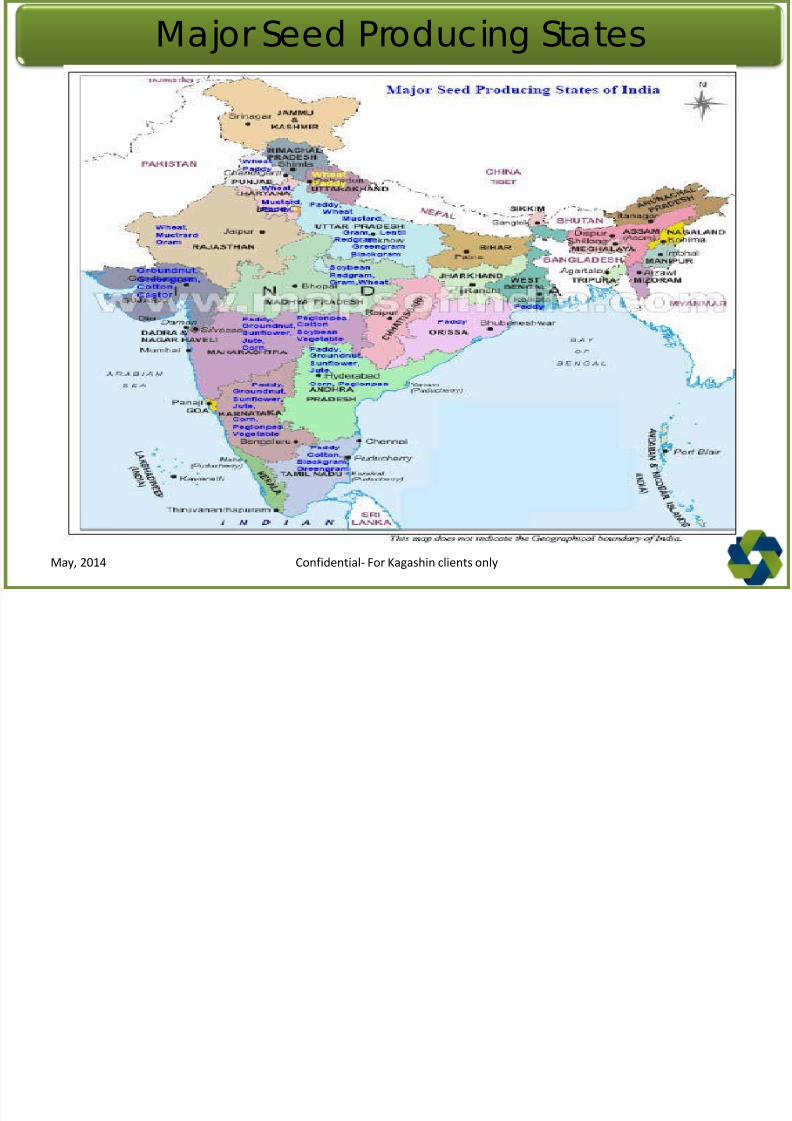

Major Seed Producing States

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 65/89

Major Seed Producing States

Confidential- For Kagashin clients onlyMay, 2014

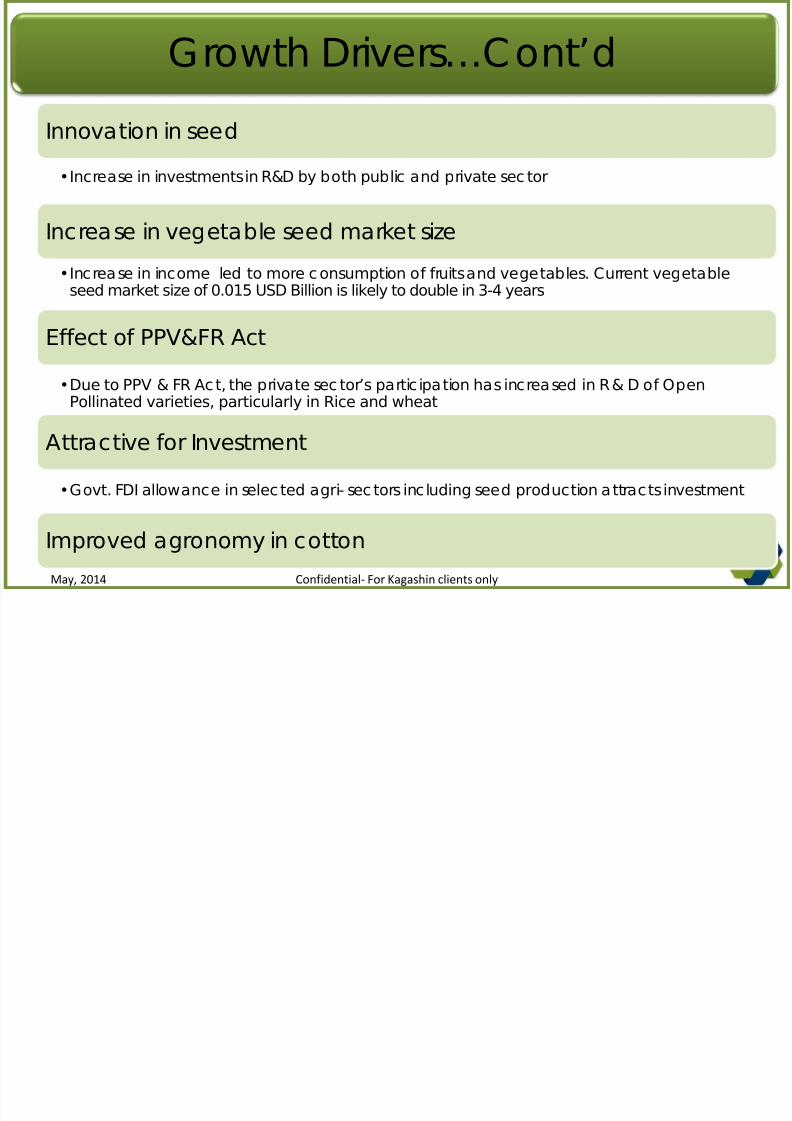

Growth Drivers

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 66/89

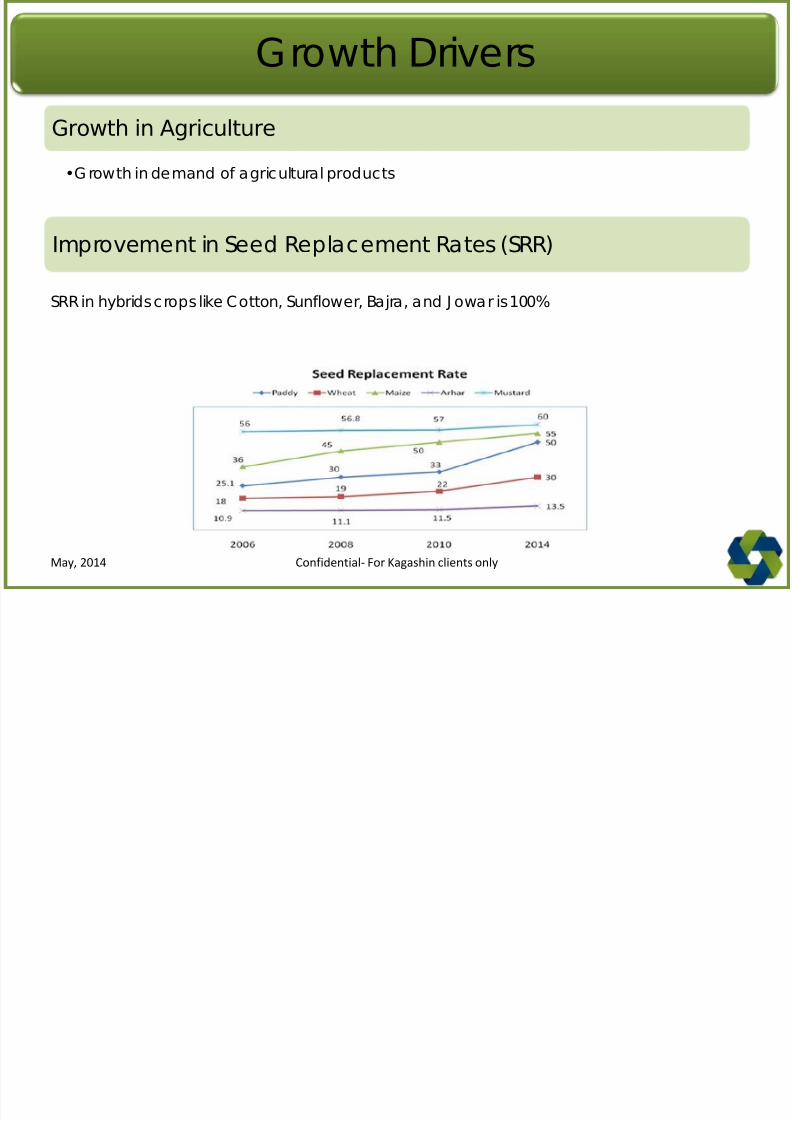

Growth Drivers

Growth in Agriculture

•Growth in demand of agricultural products

Improvement in Seed Replacement Rates (SRR)

SRR in hybrids crops like Cotton, Sunflower, Bajra, and J owar is 100%

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 67/89

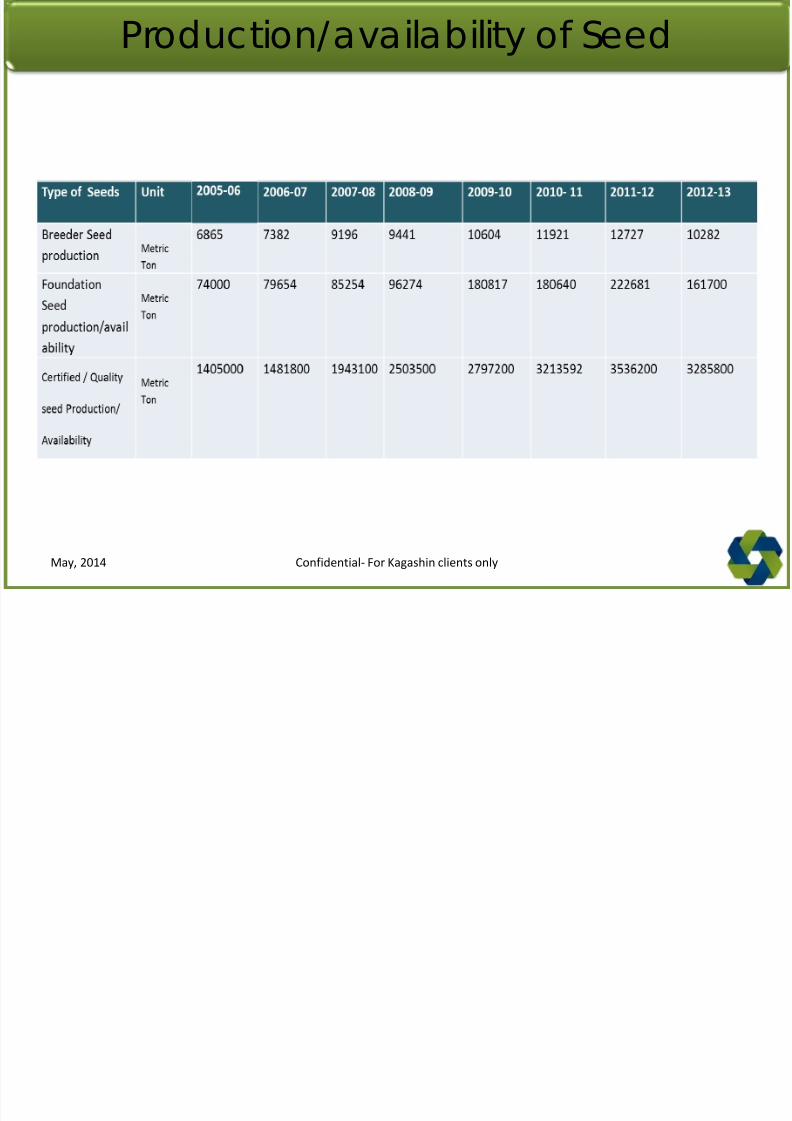

Production/availability of Seed

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 68/89

oduc o /a a ab y o Seed

Confidential- For Kagashin clients onlyMay, 2014

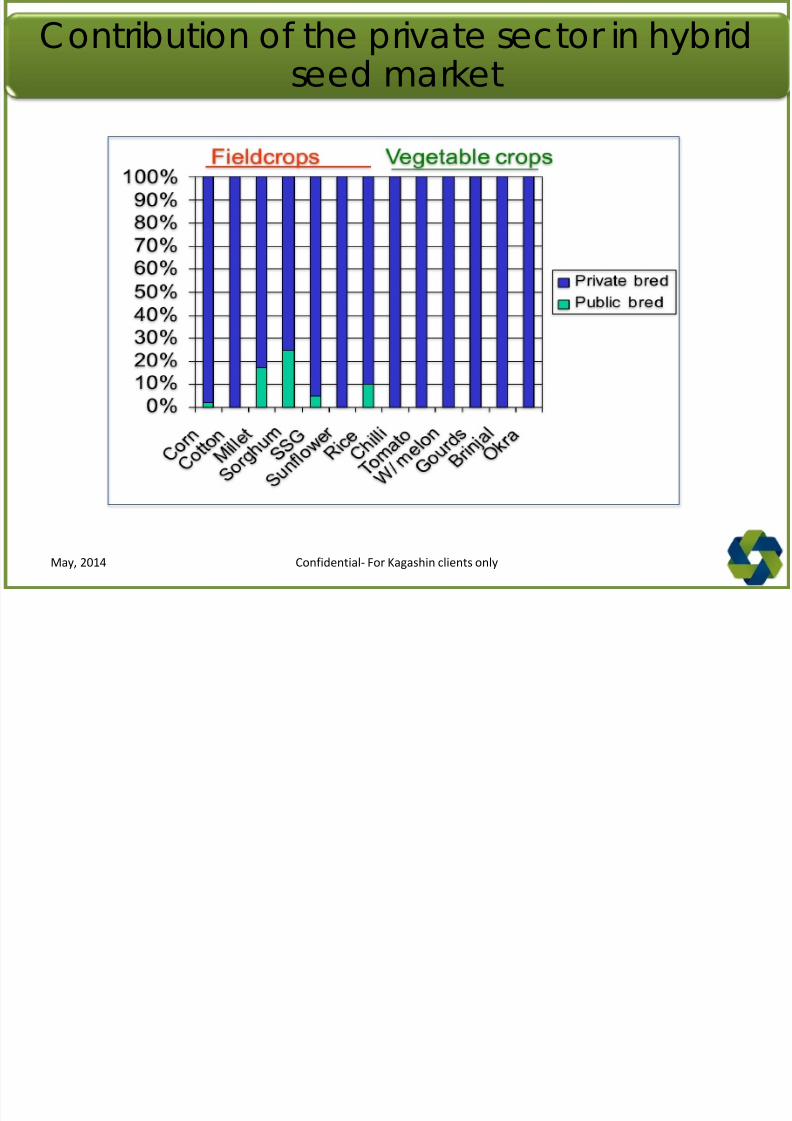

Contribution of the private sector in hybrid

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 69/89

p yseed market

Confidential- For Kagashin clients onlyMay, 2014

E olution of the Indian Seed Industr

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 70/89

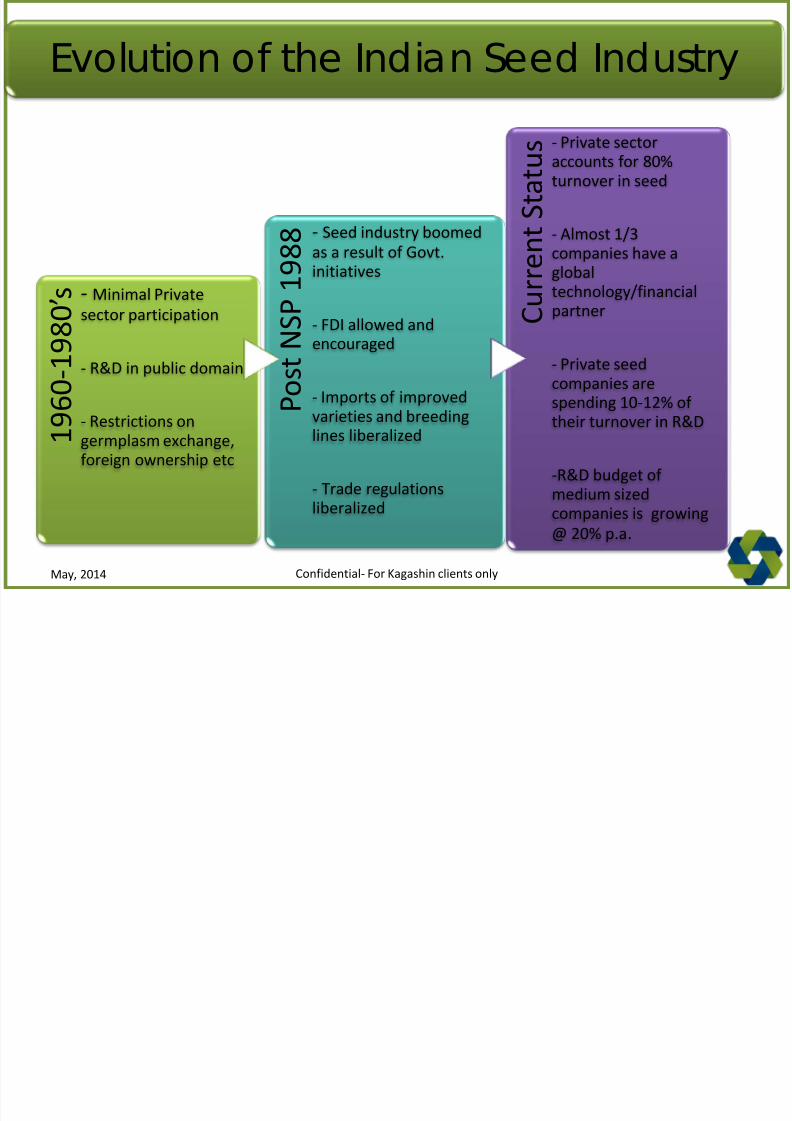

Evolution of the Indian Seed Industry

1 9

6 0 - 1 9 8 0 ’ s- Minimal Private

sector participation

- R&D in public domain

- Restrictions ongermplasm exchange,foreign ownership etc

P o s t N S P 1

9 8 8- Seed industry boomed

as a result of Govt.initiatives

- FDI allowed andencouraged

- Imports of improvedvarieties and breedinglines liberalized

- Trade regulationsliberalized

C u r

r e n t S t a t u s- Private sectoraccounts for 80%

turnover in seed

- Almost 1/3companies have aglobal

technology/financialpartner

- Private seedcompanies arespending 10-12% of

their turnover in R&D

-R&D budget ofmedium sizedcompanies is growing

@ 20% p.a.

Confidential- For Kagashin clients onlyMay, 2014

C

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 71/89

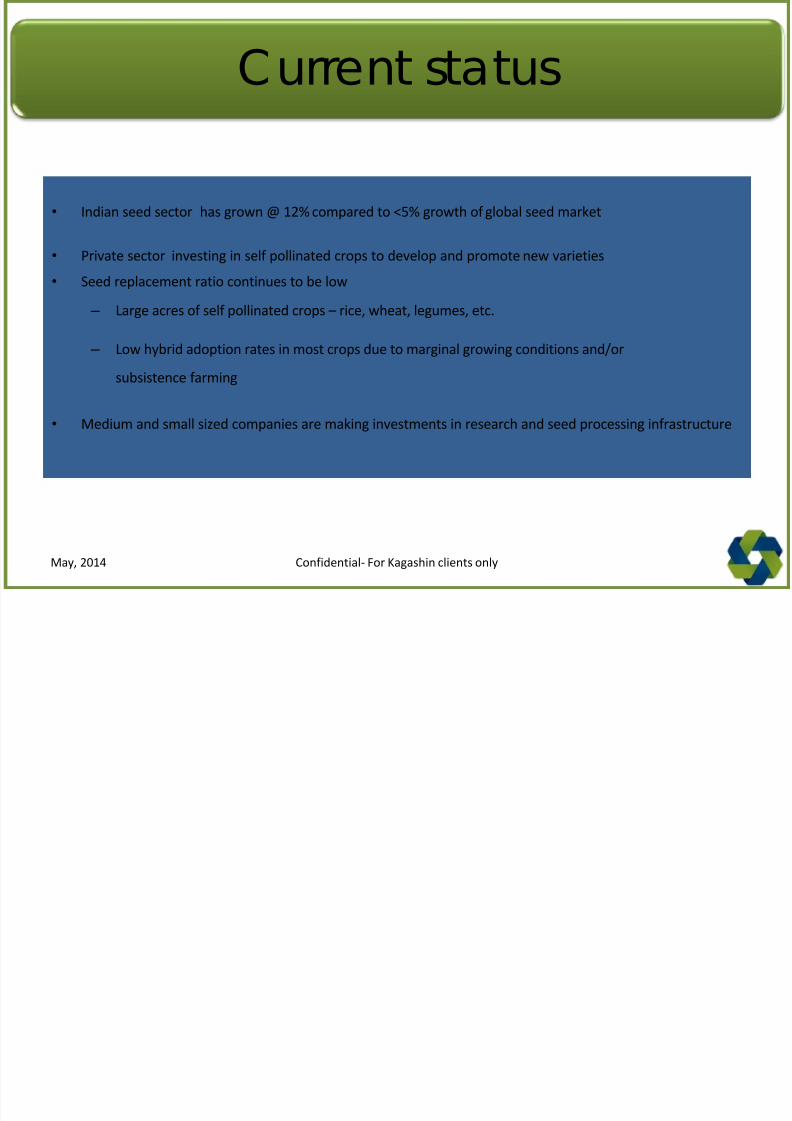

Current status

• Indian seed sector has grown @ 12% compared to <5% growth of global seed market

• Private sector investing in self pollinated crops to develop and promote new varieties

• Seed replacement ratio continues to be low – Large acres of self pollinated crops – rice, wheat, legumes, etc.

– Low hybrid adoption rates in most crops due to marginal growing conditions and/or

subsistence farming

• Medium and small sized companies are making investments in research and seed processing infrastructure

Confidential- For Kagashin clients onlyMay, 2014

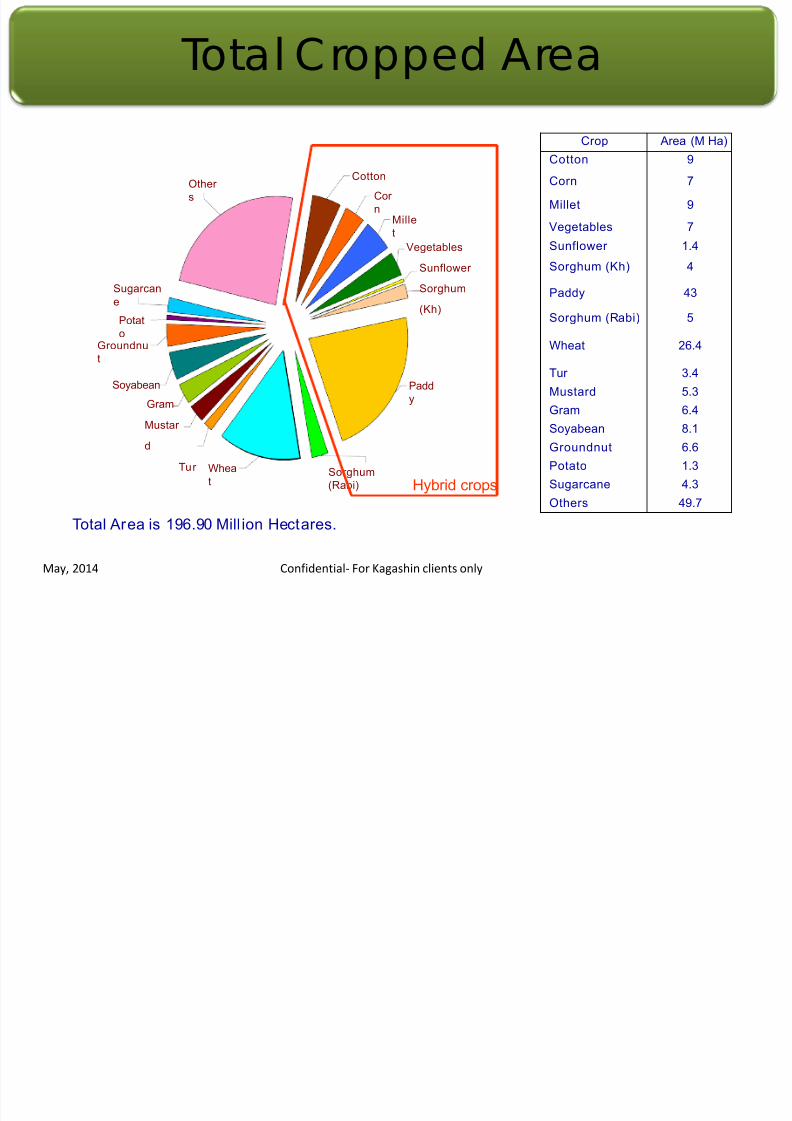

Total Cropped Area

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 72/89

Cotton

Cor

n Mille

t

Vegetables

Sunflower

Sorghum

(Kh)

Padd

y

Whea

t

Sugarcane

Potat

o Groundnu

t

Soyabean

Gram

Mustar

d

Tur Sorghum

(Rabi)

Other

s

Total Area is 196.90 Mill ion Hectares.

Total Cropped Area

Hybrid crops

Crop Area (M Ha)

Cotton 9

Corn 7

Millet 9

Vegetables 7

Sunflower 1.4

Sorghum (Kh) 4

Paddy 43

Sorghum (Rabi) 5

Wheat 26.4

Tur 3.4

Mustard 5.3

Gram 6.4

Soyabean 8.1

Groundnut 6.6

Potato 1.3

Sugarcane 4.3

Others 49.7

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 73/89

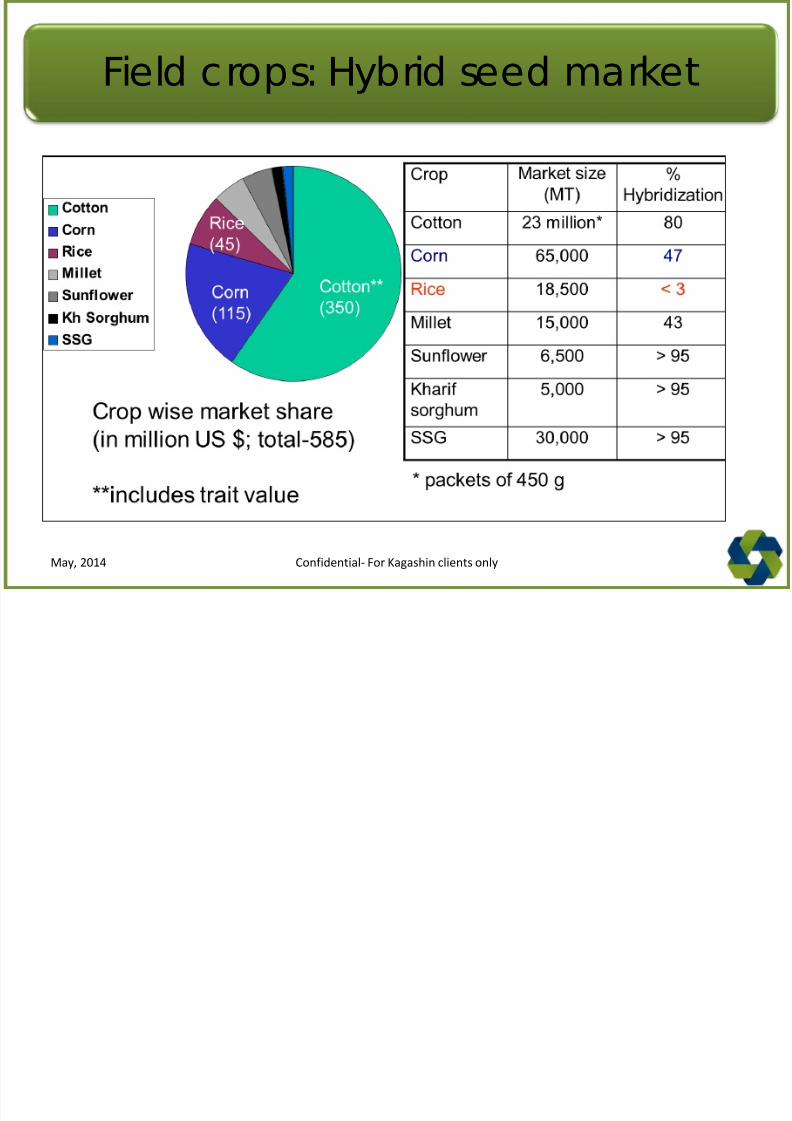

Field crops: Hybrid seed market

Confidential- For Kagashin clients onlyMay, 2014

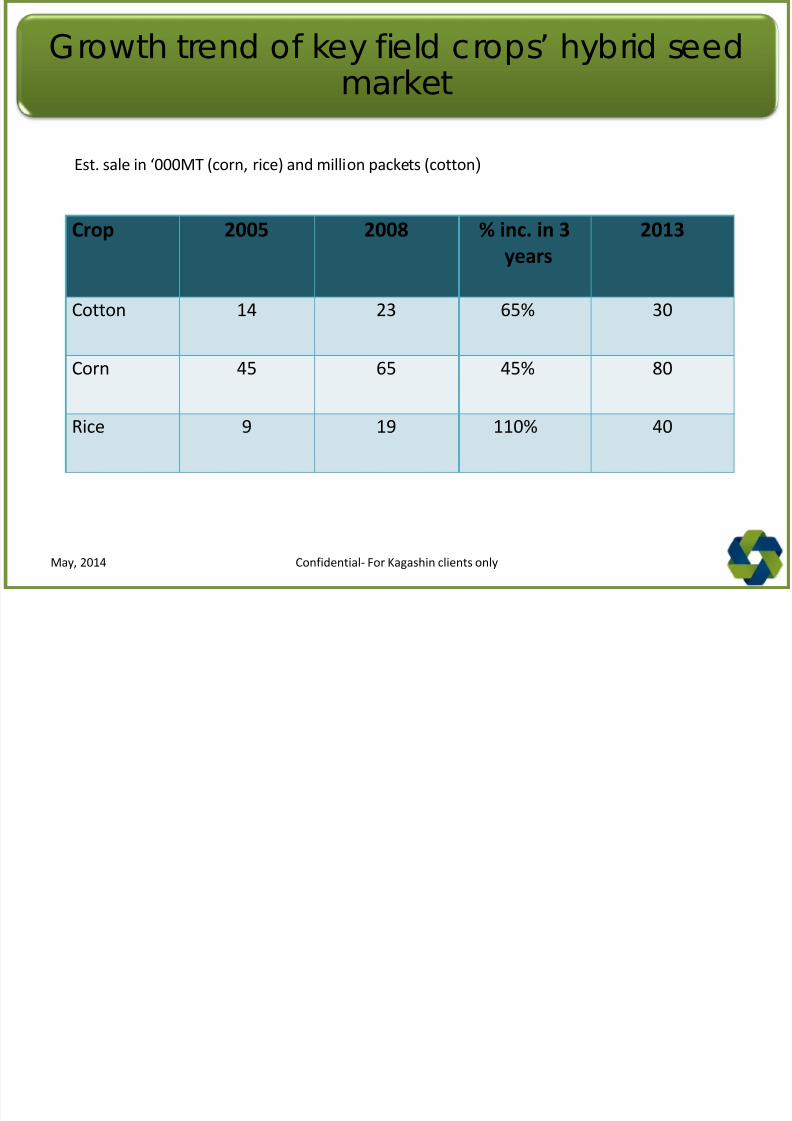

Growth trend of key field crops’ hybrid seed

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 74/89

Growth trend of key field crops hybrid seedmarket

Est. sale in ‘000MT (corn, rice) and million packets (cotton)

Crop 2005 2008 % inc. in 3

years

2013

Cotton 14 23 65% 30

Corn 45 65 45% 80

Rice 9 19 110% 40

Confidential- For Kagashin clients onlyMay, 2014

V bl H b id d k

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 75/89

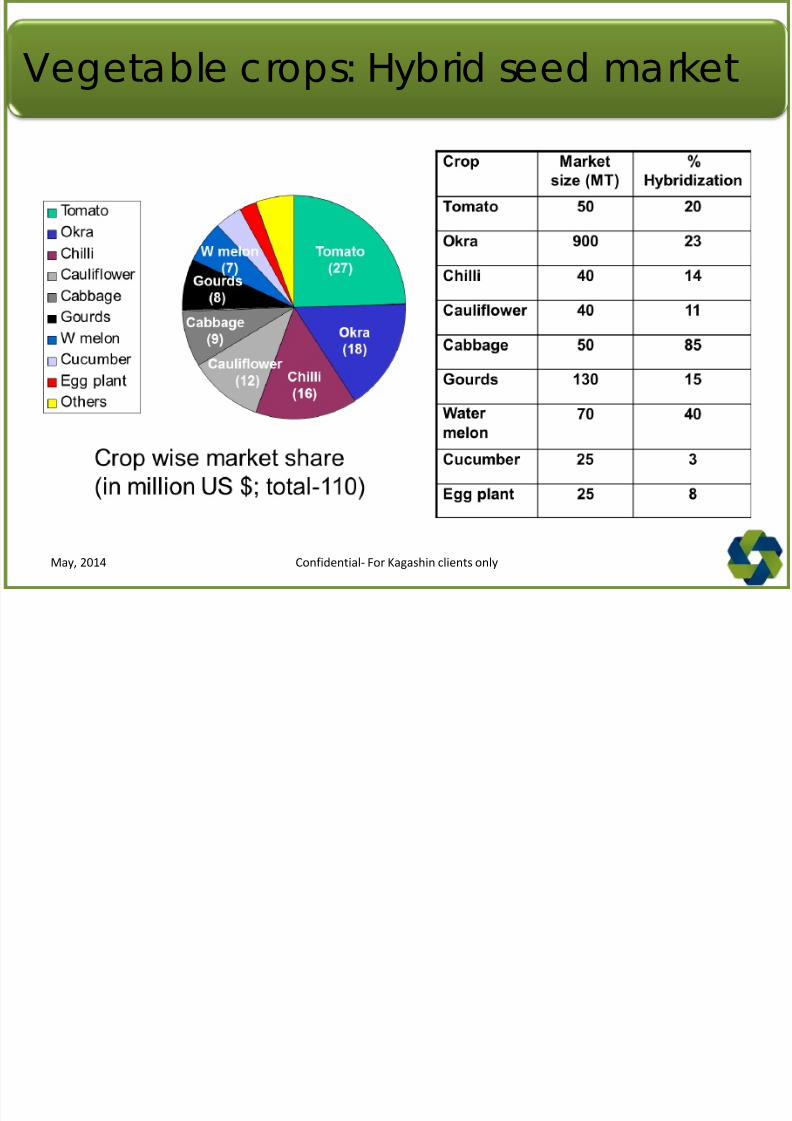

Vegetable crops: Hybrid seed market

Confidential- For Kagashin clients onlyMay, 2014

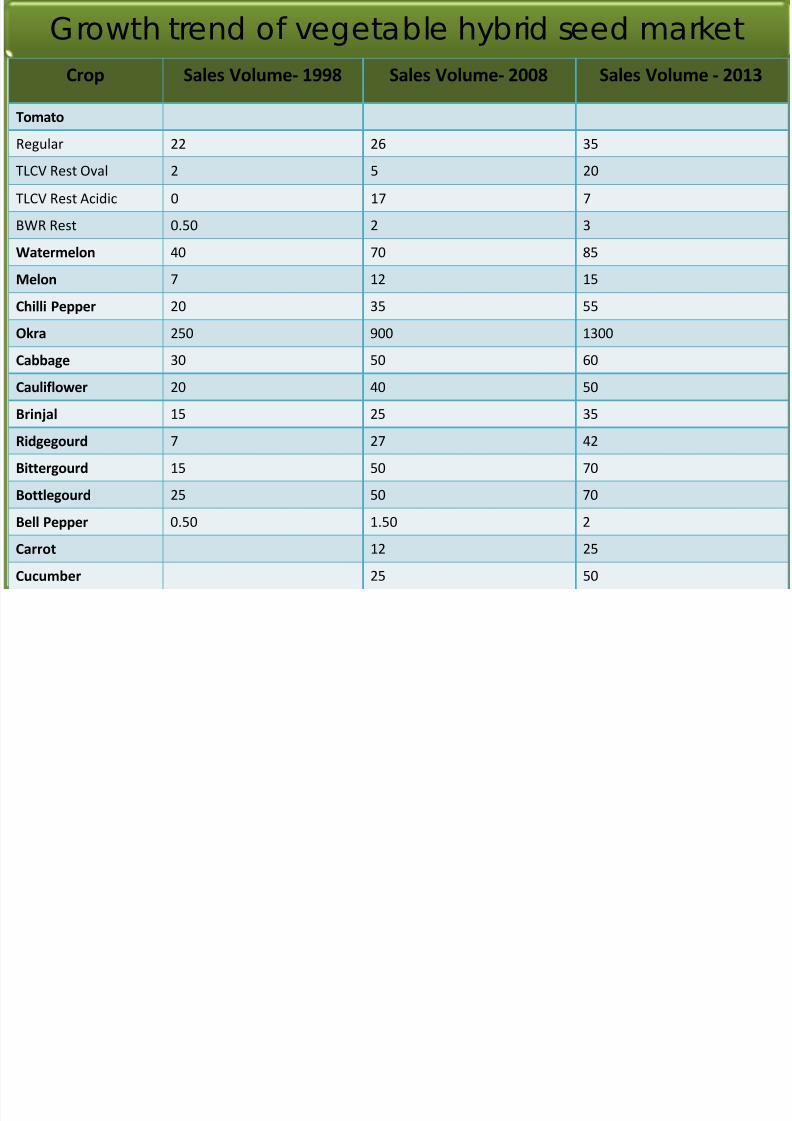

Growth trend of vegetable hybrid seed market

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 76/89

Crop Sales Volume- 1998 Sales Volume- 2008 Sales Volume - 2013

Tomato

Regular 22 26 35TLCV Rest Oval 2 5 20

TLCV Rest Acidic 0 17 7

BWR Rest 0.50 2 3

Watermelon 40 70 85

Melon 7 12 15

Chilli Pepper 20 35 55

Okra 250 900 1300

Cabbage 30 50 60

Cauliflower 20 40 50

Brinjal 15 25 35

Ridgegourd 7 27 42

Bittergourd 15 50 70

Bottlegourd 25 50 70

Bell Pepper 0.50 1.50 2

Carrot 12 25

Cucumber 25 50

Impact of new technology on Cotton

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 77/89

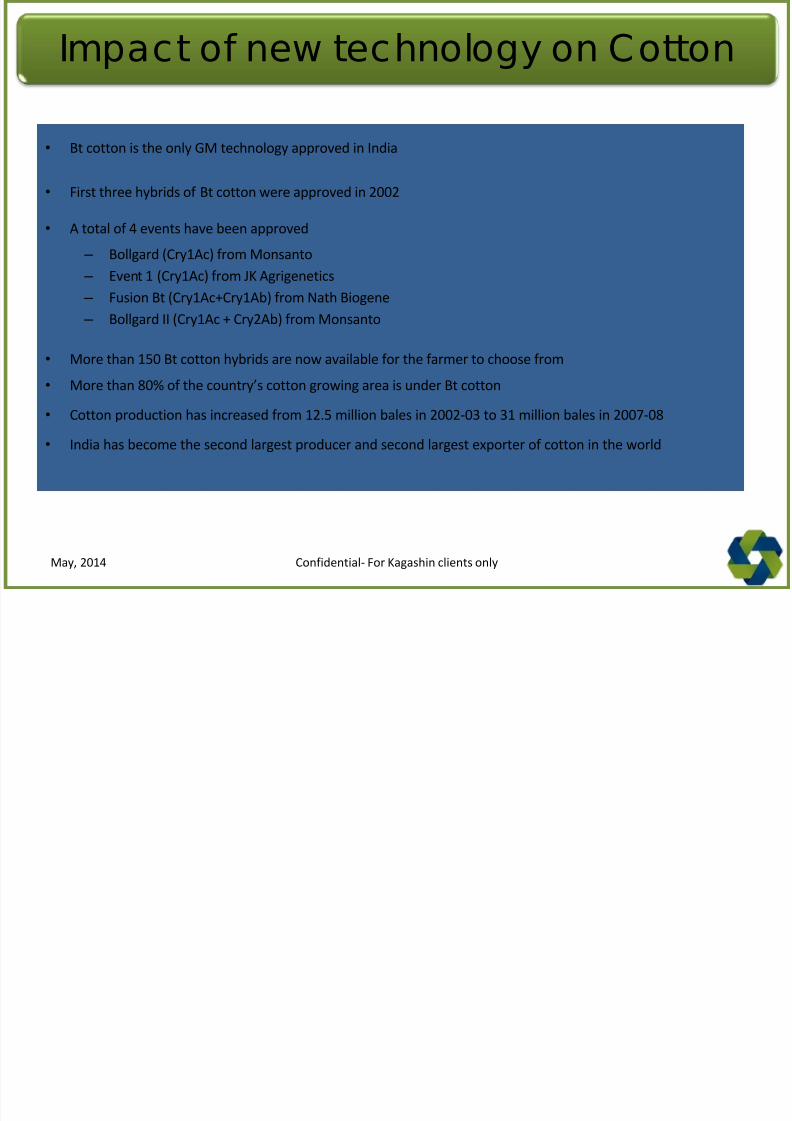

Impact of new technology on Cotton

• Bt cotton is the only GM technology approved in India

• First three hybrids of Bt cotton were approved in 2002

• A total of 4 events have been approved

– Bollgard (Cry1Ac) from Monsanto

– Event 1 (Cry1Ac) from JK Agrigenetics

– Fusion Bt (Cry1Ac+Cry1Ab) from Nath Biogene

– Bollgard II (Cry1Ac + Cry2Ab) from Monsanto

• More than 150 Bt cotton hybrids are now available for the farmer to choose from

• More than 80% of the country’s cotton growing area is under Bt cotton

• Cotton production has increased from 12.5 million bales in 2002-03 to 31 million bales in 2007-08

• India has become the second largest producer and second largest exporter of cotton in the world

Confidential- For Kagashin clients onlyMay, 2014

l f k

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 78/89

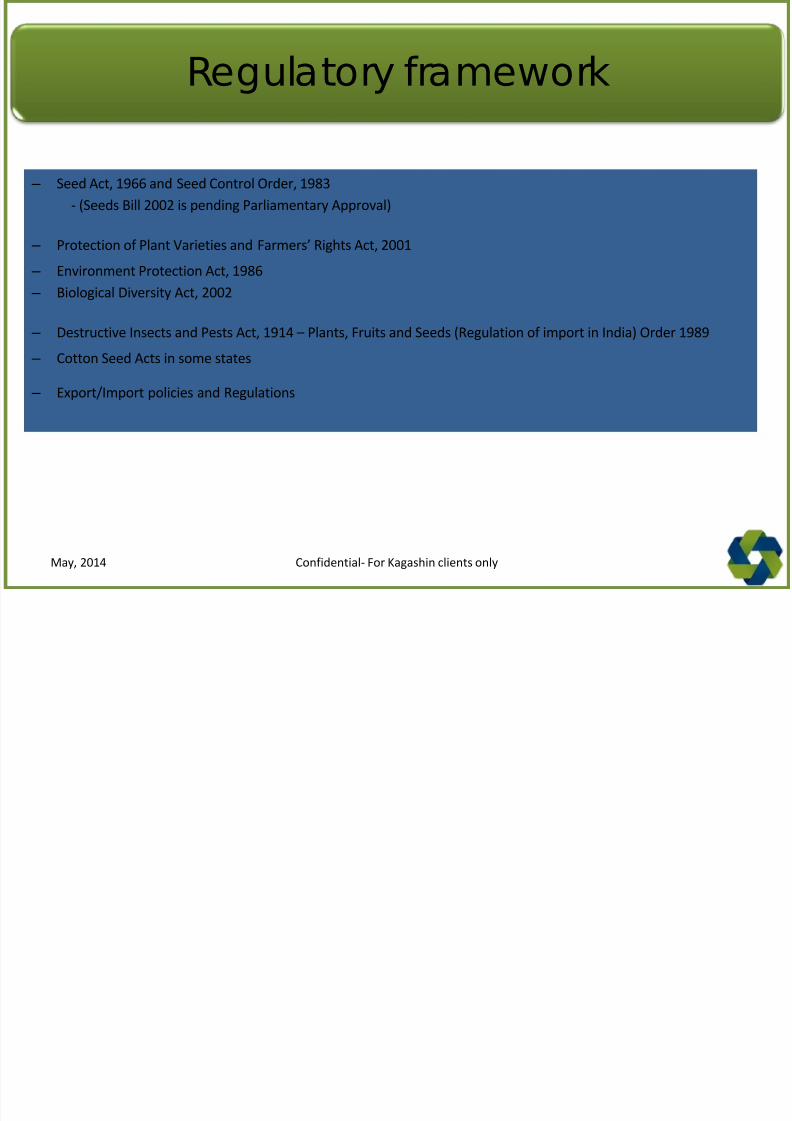

Regulatory framework

– Seed Act, 1966 and Seed Control Order, 1983

- (Seeds Bill 2002 is pending Parliamentary Approval)

– Protection of Plant Varieties and Farmers’ Rights Act, 2001

– Environment Protection Act, 1986

– Biological Diversity Act, 2002

– Destructive Insects and Pests Act, 1914 – Plants, Fruits and Seeds (Regulation of import in India) Order 1989

– Cotton Seed Acts in some states

– Export/Import policies and Regulations

Confidential- For Kagashin clients onlyMay, 2014

Regulatory Challenges

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 79/89

g y g

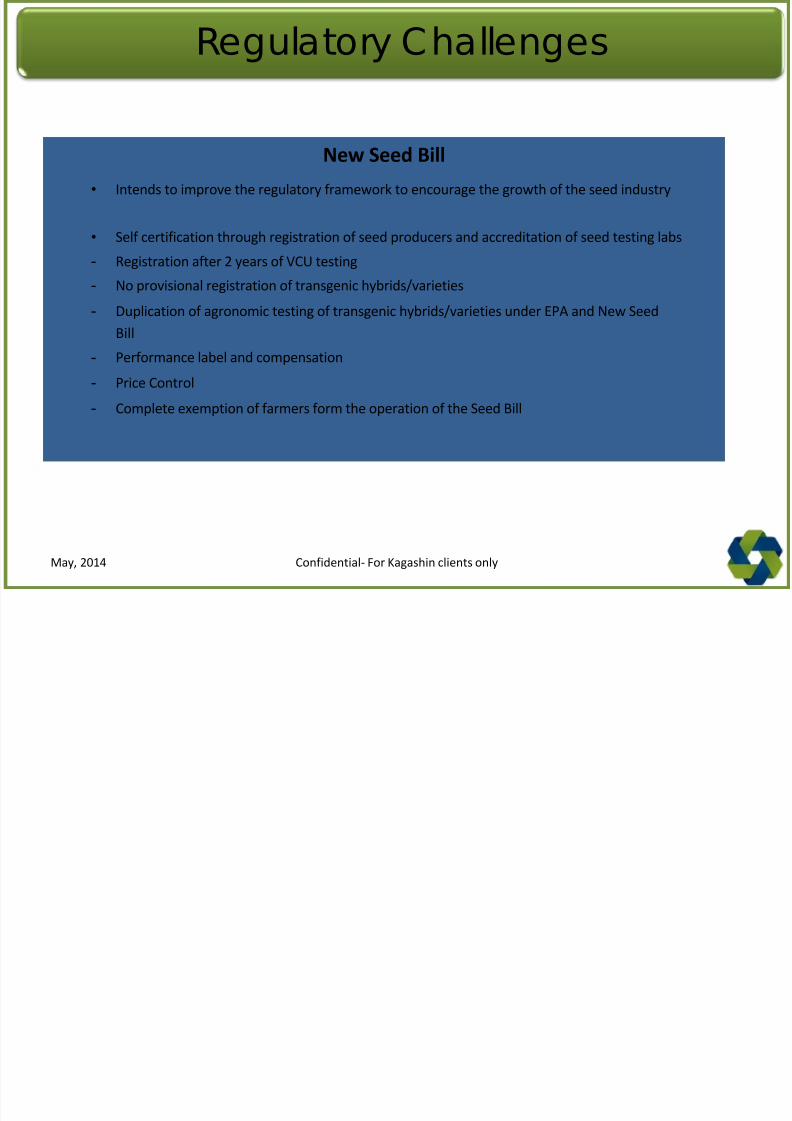

New Seed Bill

• Intends to improve the regulatory framework to encourage the growth of the seed industry

• Self certification through registration of seed producers and accreditation of seed testing labs

- Registration after 2 years of VCU testing

- No provisional registration of transgenic hybrids/varieties- Duplication of agronomic testing of transgenic hybrids/varieties under EPA and New Seed

Bill

- Performance label and compensation

- Price Control

- Complete exemption of farmers form the operation of the Seed Bill

Confidential- For Kagashin clients onlyMay, 2014

R l Ch ll C ’d

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 80/89

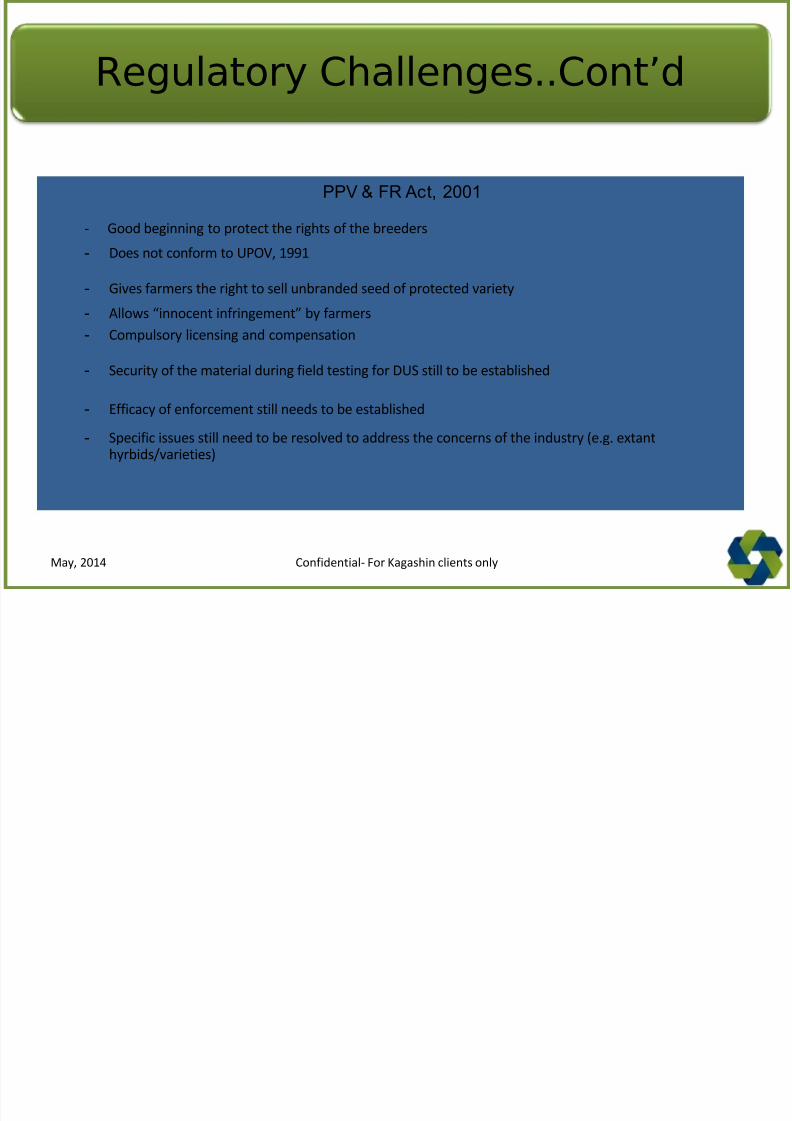

PPV & FR Act, 2001

- Good beginning to protect the rights of the breeders

- Does not conform to UPOV, 1991

- Gives farmers the right to sell unbranded seed of protected variety

- Allows “innocent infringement” by farmers

- Compulsory licensing and compensation

- Security of the material during field testing for DUS still to be established

- Efficacy of enforcement still needs to be established

- Specific issues still need to be resolved to address the concerns of the industry (e.g. extanthyrbids/varieties)

Regulatory Challenges..Cont’d

Confidential- For Kagashin clients onlyMay, 2014

Regulatory Challenges..Cont’d

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 81/89

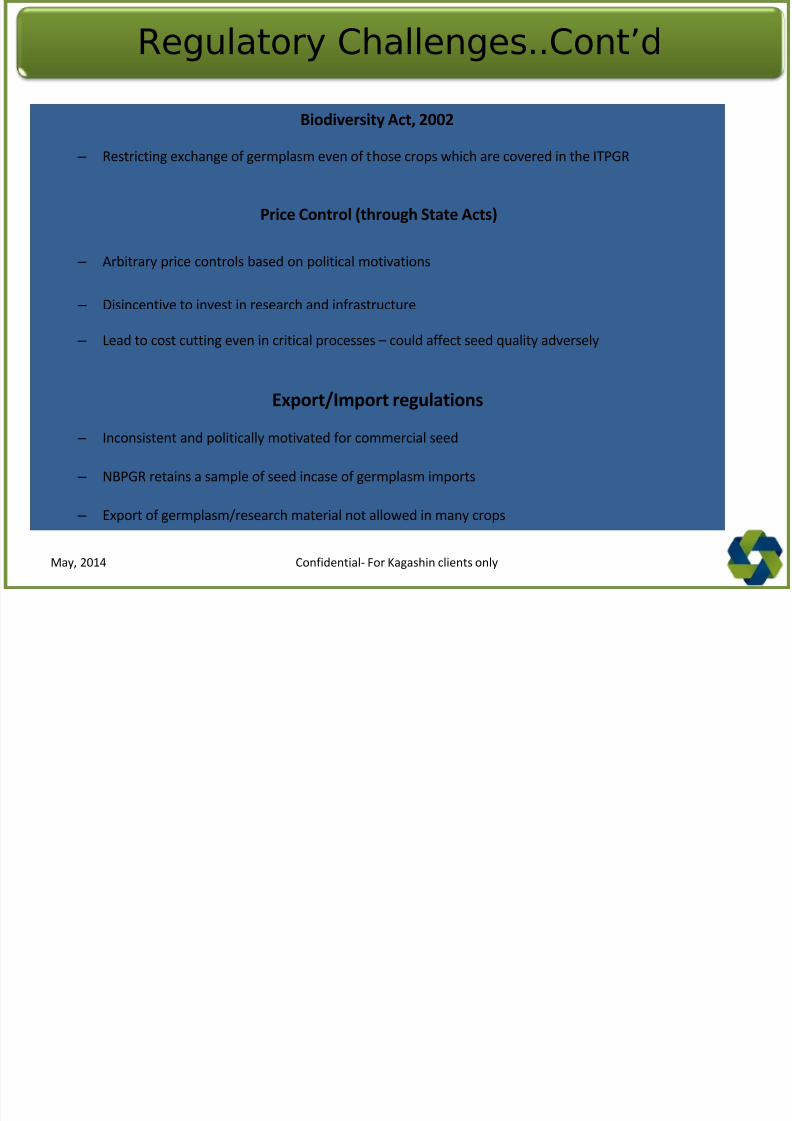

Biodiversity Act, 2002

– Restricting exchange of germplasm even of those crops which are covered in the ITPGR

Price Control (through State Acts)

– Arbitrary price controls based on political motivations

– Disincentive to invest in research and infrastructure

– Lead to cost cutting even in critical processes – could affect seed quality adversely

Export/Import regulations

– Inconsistent and politically motivated for commercial seed

– NBPGR retains a sample of seed incase of germplasm imports

– Export of germplasm/research material not allowed in many crops

g y g

Confidential- For Kagashin clients onlyMay, 2014

Productivity challenges

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 82/89

Productivity challenges

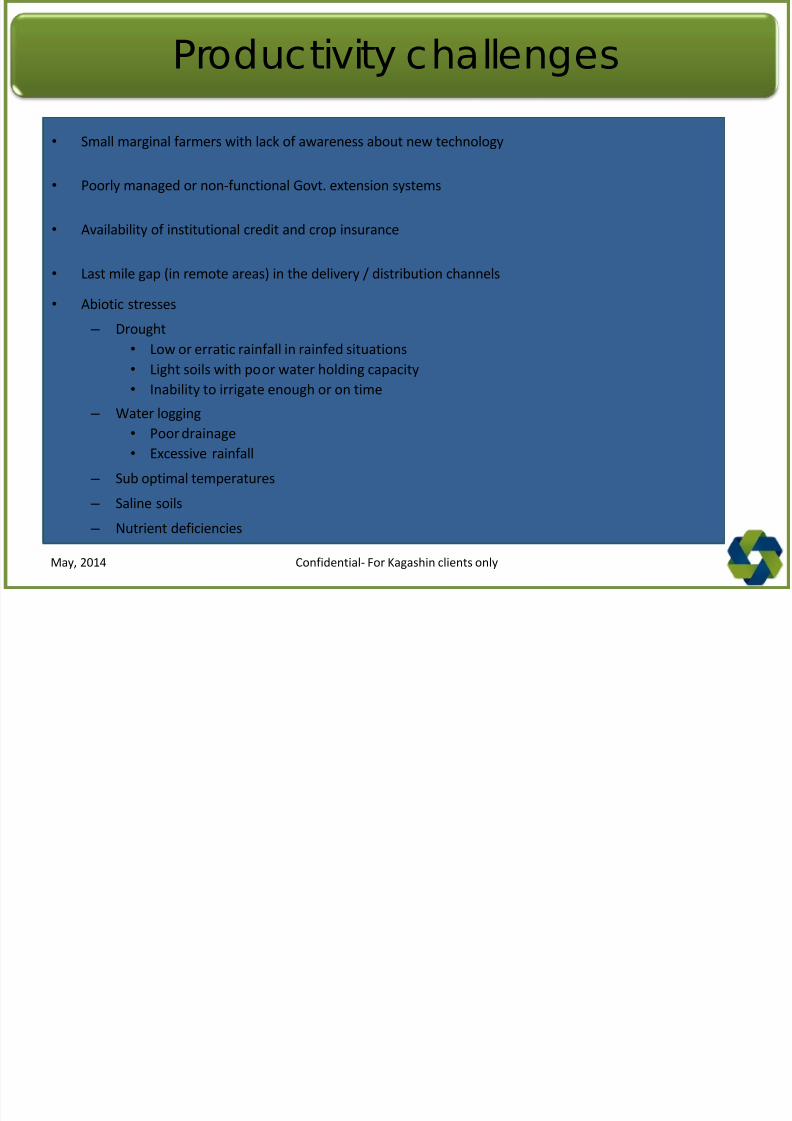

• Small marginal farmers with lack of awareness about new technology

• Poorly managed or non-functional Govt. extension systems

• Availability of institutional credit and crop insurance

• Last mile gap (in remote areas) in the delivery / distribution channels

• Abiotic stresses

– Drought

• Low or erratic rainfall in rainfed situations

• Light soils with poor water holding capacity

• Inability to irrigate enough or on time

– Water logging

• Poor drainage

• Excessive rainfall

– Sub optimal temperatures

– Saline soils

– Nutrient deficiencies

Confidential- For Kagashin clients onlyMay, 2014

P d ti it h ll C t’d

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 83/89

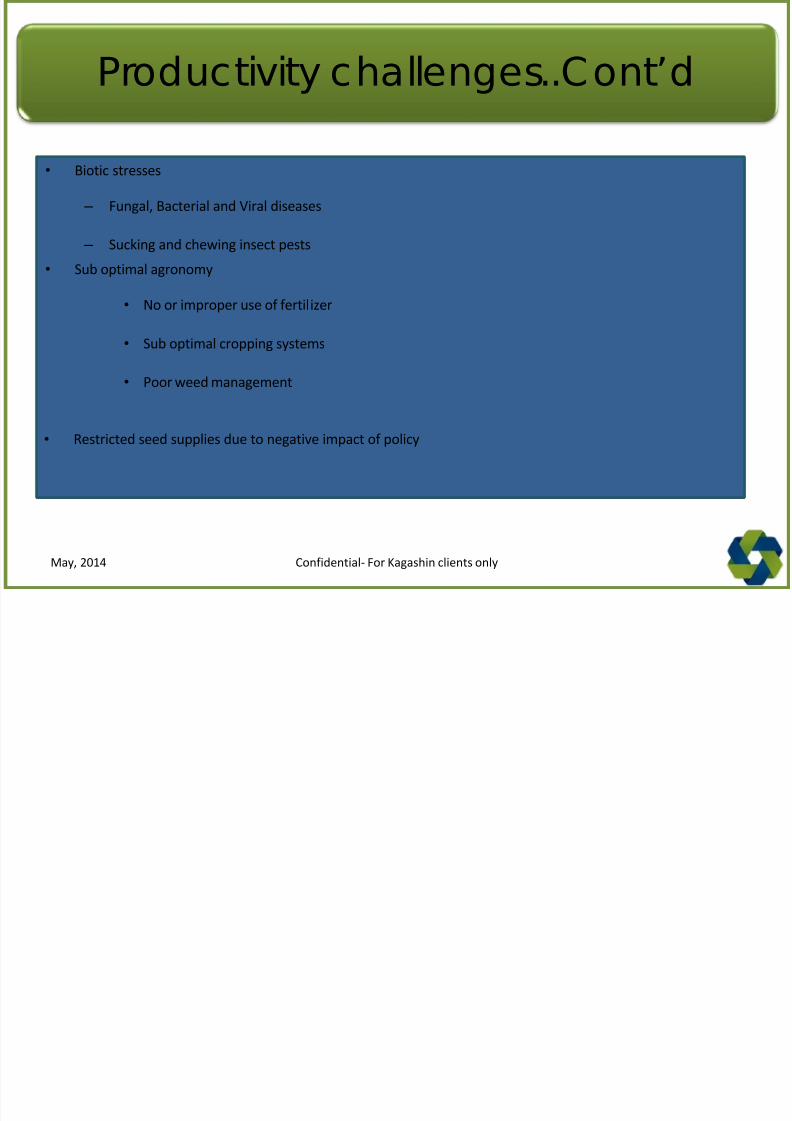

Productivity challenges..Cont’d

• Biotic stresses

– Fungal, Bacterial and Viral diseases

– Sucking and chewing insect pests

• Sub optimal agronomy

• No or improper use of fertilizer

• Sub optimal cropping systems

• Poor weed management

• Restricted seed supplies due to negative impact of policy

Confidential- For Kagashin clients onlyMay, 2014

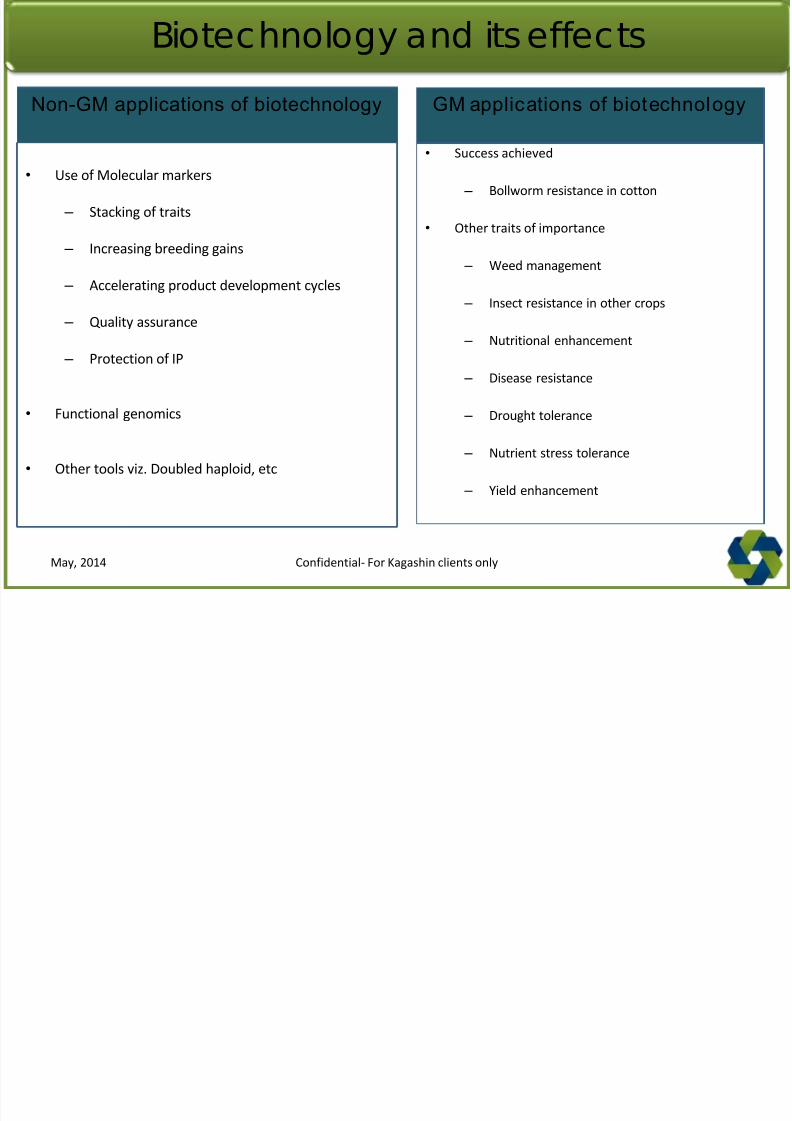

Biotechnology and its effects

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 84/89

• Use of Molecular markers

– Stacking of traits

– Increasing breeding gains

– Accelerating product development cycles

– Quality assurance

– Protection of IP

• Functional genomics

• Other tools viz. Doubled haploid, etc

• Success achieved

– Bollworm resistance in cotton

• Other traits of importance

– Weed management

– Insect resistance in other crops

– Nutritional enhancement

– Disease resistance

– Drought tolerance

– Nutrient stress tolerance

– Yield enhancement

GM applications of biotechnologyNon-GM applications of biotechnology

Confidential- For Kagashin clients onlyMay, 2014

Technologiesunder development in India

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 85/89

Technologies under development in India

Confidential- For Kagashin clients onlyMay, 2014

Way Forward

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 86/89

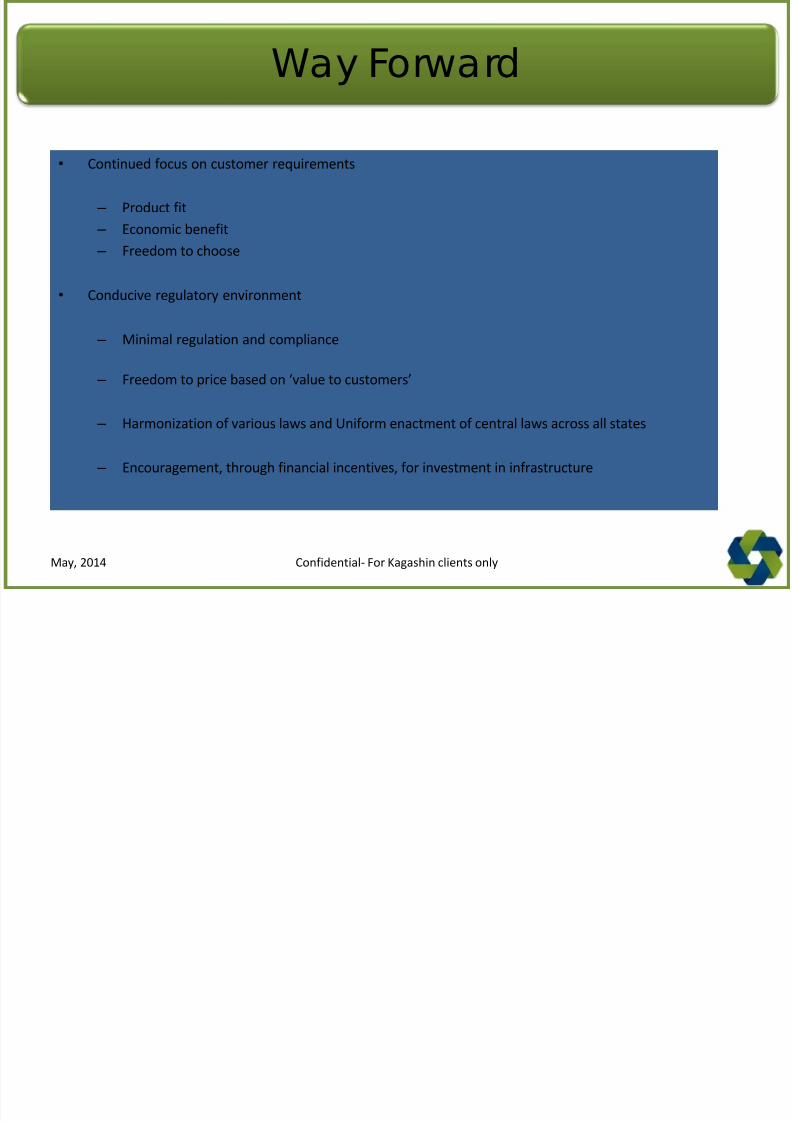

Way Forward

• Continued focus on customer requirements

– Product fit

– Economic benefit

– Freedom to choose

• Conducive regulatory environment

– Minimal regulation and compliance

– Freedom to price based on ‘value to customers’

– Harmonization of various laws and Uniform enactment of central laws across all states

– Encouragement, through financial incentives, for investment in infrastructure

Confidential- For Kagashin clients onlyMay, 2014

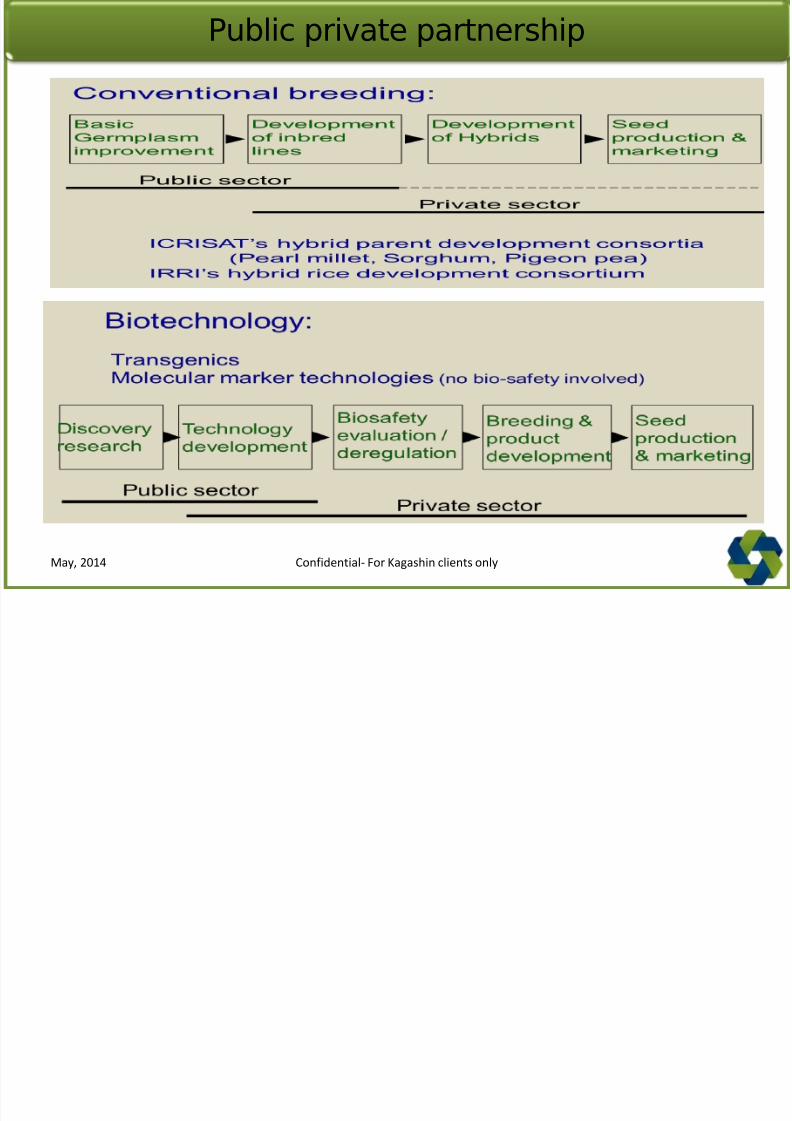

Public private partnership

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 87/89

Confidential- For Kagashin clients onlyMay, 2014

Summary

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 88/89

Summary

• Indian seed industry is poised to grow at a rate faster than the global rate (huge opportunity to increaseSRR)

• It has made tremendous contribution to increase productivity through development of superiorhybrids

• It is investing in research and infrastructure

• It has spearheaded the introduction of new technology (Bt cotton)

• Indian seed industry needs policy support to make even bigger contributions in the future:

– Encouragement for investment in research and infrastructure

– Minimal regulation and compliance

– Freedom to operate based on free market principles

– Streamlining of regulatory processes to accelerate the development and introduction of new GMtechnology

• Robust PPP models are needed to better serve the farmers by removing the various productivity constraints

through technological interventions

Confidential- For Kagashin clients onlyMay, 2014

8/11/2019 IndianAgriculture a Snapshot

http://slidepdf.com/reader/full/indianagriculture-a-snapshot 89/89

Thank You

Office No 339, Regus Business Centre3rd Floor Neo Vikram

New Link Road, Andheri (W)Mumbai 400 053Email: [email protected]