akash swot 1

TRANSCRIPT

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 1/14

Thomas Cook has been granted an authorized dealers' license (category II) by RBI to dealin foreign exchange through its designated branches. Under this license, we have been,inter-alia, granted permission to undertake the following activities:

1. Retail purchases of foreign currencies and travelers cheques.

2. Bulk purchases/sales of foreign currencies from/to authorized dealers, money

changers and franchisees.

3. Release / remittance of foreign exchange for the following activities:

a. Private Visits

b. Remittance by tour operators/travel agents to overseas agents/principals/hotels

c. Business Travel (including for Central and State Government officials)

d. Fee for participation in global conferences and specialized training

e. Payment of crew wages

f. Film Shooting

g. Medical Treatment abroad

h. Overseas Education

i. Remittance under educational tie up arrangements with universities abroad

j.Maintenance of close relatives abroad

k. Stall rentals and participation fees in connection with participation in overseasexhibitions / fairs

4. Import and export of foreign currency and export of encashed Traveler's Cheques

5. Maintenance of foreign currency accounts with banks abroad and undertaking forexcover operations in India and abroad.

TCIL presently operates in over 72 cities across over 180 locations.

The Company employs over 2,200 resources and is listed on both the Bombay Stock Exchange as well as the National Stock Exchange.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 2/14

Foreign Exchange - Products and Services

•Purchase and Sale of currency notes in 26 destination currencies

•Purchase and Sale of foreign currency denominated travelers cheques

•Thomas Cook Global Money Card and Citibank World Money Card as prepaid cards,which is a convenient way to carry money overseas

•Foreign Currency Drafts.

•Wire transfer of Funds.

•Remittance of money into India through Money Gram.

•Cash Advances against International Credit Card.

Salient Features:-

Thomas Cook Titanium MasterCard features in brief:

•The card has been specially designed for frequent travelers.

•Attractive 6 reward points for each spend of Rs.100 on the card on Thomas Cook products

- Free Delivery of Foreign Exchange within city limits.

•Rs. 5,000 discount on any Thomas Cook GIT product.

•1 Free Air ticket to a domestic destination on the issuance of new card

•Complimentary travel inconvenience insurance policy

•Access to MasterCard travel lounges at Airports across the world

•Redemption of reward points for Thomas Cook holiday packages, hotel stays, air tickets, airline upgrades, etc

•Conversion of Thomas Cook reward points to frequent flyer miles - convert thereward points earned on card to frequent flyer miles on select domestic airlines.

•Positioned as a comprehensive travel card.

•Assured gifts for the joining fees - free air ticket / discount voucher

•Higher reward points for card swipes at Our Company's outlets

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 3/14

•Redemption of reward points against Thomas Cook products encouraged.

Merger with MyTravel announced February 2007, completed June 2007

In June 2006, Thomas Cook (India) acquired LKP Forex Limited and Travel Corporation(India) Pvt. Ltd. (TCI).

2008 Thomas Cook Group announces the acquisition of Canada's TriWest TravelHoldings, French tour operator Jet Tours, and UK independent travel companies Hotels 4U, Gold Medal and Elegant Resorts.

Thomas Cook Group plc, UK, is one of the world’s leading leisure travel groupswith sales of £8.8 billion, 22.3million customers,

31,000 employees, a fleet of 93 aircraft and a network of over 3,400 owned andfranchised travel stores and interests in 86 hotel s and resort properties.

It operates under five geographic segments in 21 countries, and is number oneor two in all its core markets.

• Led industry consolidation and created one of the world’s largest travel groups• Over 30k employees in 15 source markets and two distinct cultures to integrate• A single majority shareholder (Arcandor with 52%)• Strong management individuals with a track record of turning around businesses• A set of industry leading travel brands, under the Thomas Cook umbrella•

• Best Travel Agency - India for the year 2008 by TTG Asia - Part of PacificAsia Travel Association (PATA.)

• Best Tour Operator by CNBC Awaaz in 2008.

• Best Outbound Tour Operator in the 4th Hospitality India & Explore the worldAnnual International Awards - 2008.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 4/14

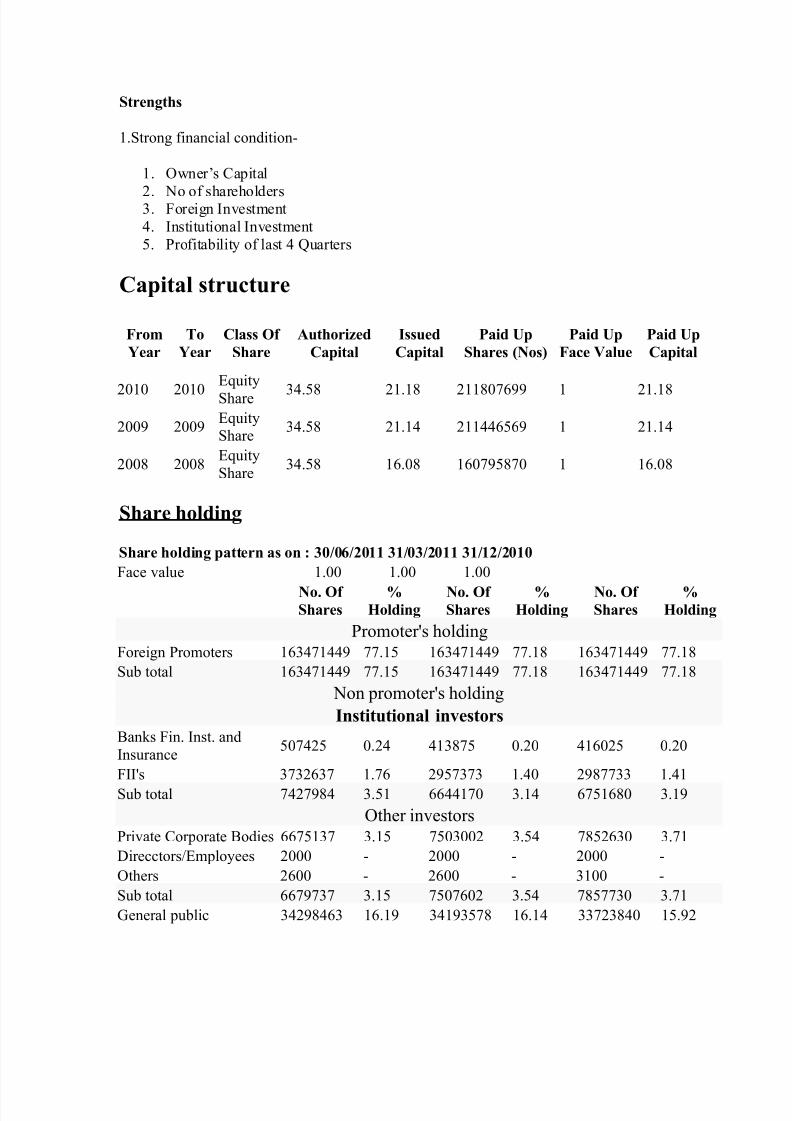

Strengths

1.Strong financial condition-

1. Owner’s Capital

2. No of shareholders3. Foreign Investment4. Institutional Investment5. Profitability of last 4 Quarters

Capital structure

FromYear

ToYear

Class Of Share

AuthorizedCapital

IssuedCapital

Paid UpShares (Nos)

Paid UpFace Value

Paid UpCapital

2010 2010EquityShare 34.58 21.18 211807699 1 21.18

2009 2009 EquityShare 34.58 21.14 211446569 1 21.14

2008 2008 EquityShare 34.58 16.08 160795870 1 16.08

Share holding

Share holding pattern as on : 30/06/2011 31/03/2011 31/12/2010Face value 1.00 1.00 1.00

No. Of Shares

%Holding

No. Of Shares

%Holding

No. Of Shares

%Holding

Promoter's holdingForeign Promoters 163471449 77.15 163471449 77.18 163471449 77.18Sub total 163471449 77.15 163471449 77.18 163471449 77.18

Non promoter's holdingInstitutional investors

Banks Fin. Inst. andInsurance 507425 0.24 413875 0.20 416025 0.20

FII's 3732637 1.76 2957373 1.40 2987733 1.41Sub total 7427984 3.51 6644170 3.14 6751680 3.19

Other investorsPrivate Corporate Bodies 6675137 3.15 7503002 3.54 7852630 3.71Direcctors/Employees 2000 - 2000 - 2000 -Others 2600 - 2600 - 3100 -Sub total 6679737 3.15 7507602 3.54 7857730 3.71General public 34298463 16.19 34193578 16.14 33723840 15.92

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 5/14

No. Of Shares

%Holding

No. Of Shares

%Holding

No. Of Shares

%Holding

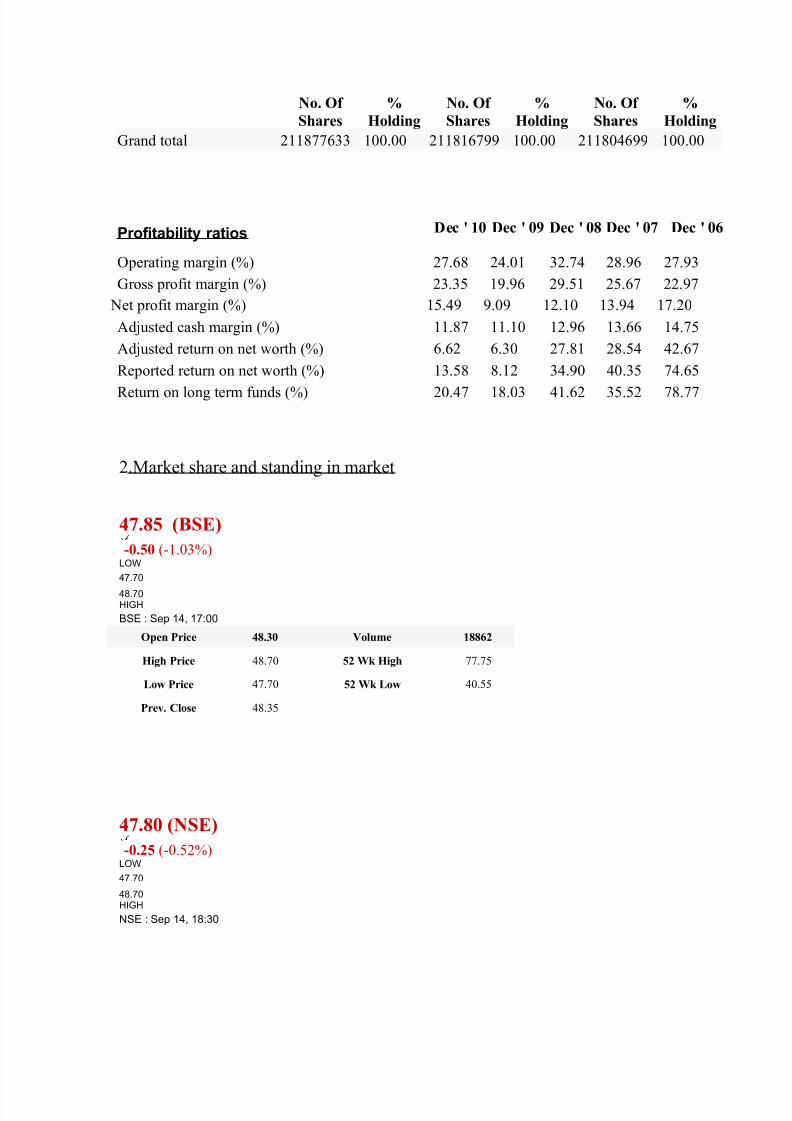

Grand total 211877633 100.00 211816799 100.00 211804699 100.00

Profitability ratios Dec ' 10 Dec ' 09 Dec ' 08 Dec ' 07 Dec ' 06

Operating margin (%) 27.68 24.01 32.74 28.96 27.93Gross profit margin (%) 23.35 19.96 29.51 25.67 22.97

Net profit margin (%) 15.49 9.09 12.10 13.94 17.20Adjusted cash margin (%) 11.87 11.10 12.96 13.66 14.75Adjusted return on net worth (%) 6.62 6.30 27.81 28.54 42.67Reported return on net worth (%) 13.58 8.12 34.90 40.35 74.65

Return on long term funds (%) 20.47 18.03 41.62 35.52 78.77

2.Market share and standing in market

47.85 (BSE)-0.50 (-1.03%)

LOW47.70

48.70HIGHBSE : Sep 14, 17:00

Open Price 48.30 Volume 18862

High Price 48.70 52 Wk High 77.75

Low Price 47.70 52 Wk Low 40.55

Prev. Close 48.35

47.80 (NSE)-0.25 (-0.52%)

LOW47.70

48.70HIGHNSE : Sep 14, 18:30

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 6/14

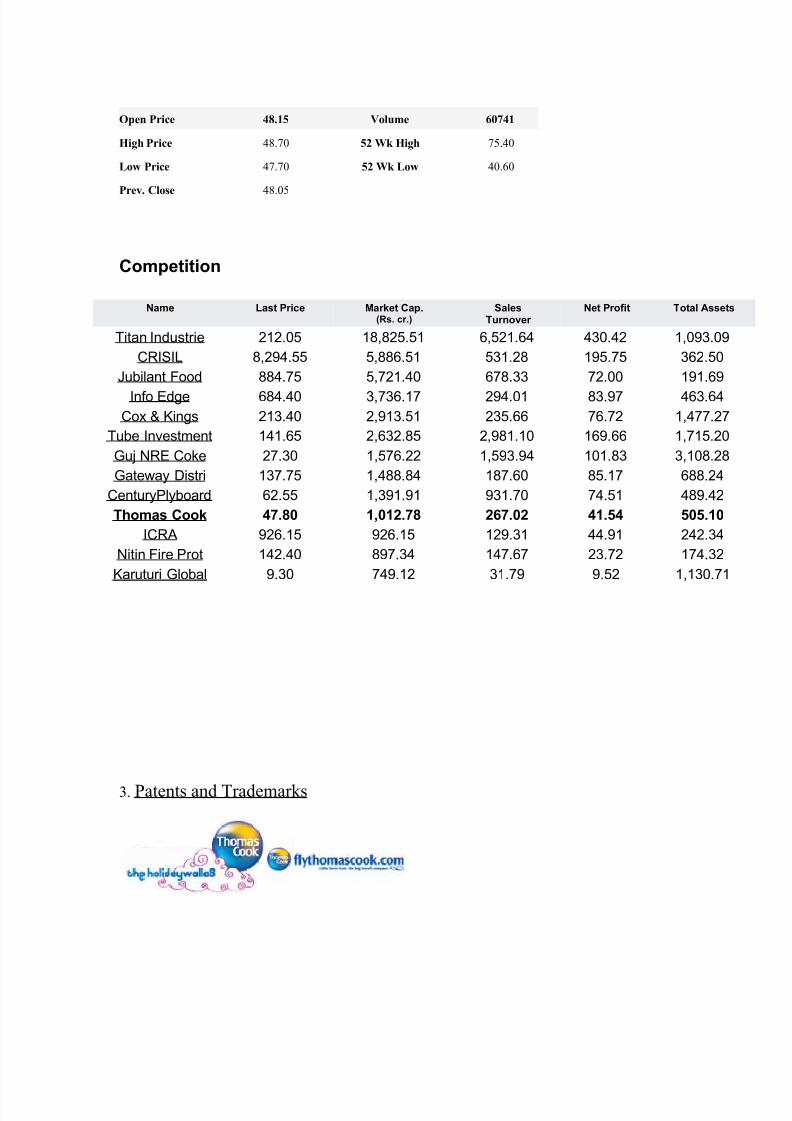

Open Price 48.15 Volume 60741

High Price 48.70 52 Wk High 75.40

Low Price 47.70 52 Wk Low 40.60

Prev. Close 48.05

Competition

3. Patents and Trademarks

Name Last Price Market Cap.(Rs. cr.)

SalesTurnover

Net Profit Total Assets

Titan Industrie 212.05 18,825.51 6,521.64 430.42 1,093.09CRISIL 8,294.55 5,886.51 531.28 195.75 362.50

Jubilant Food 884.75 5,721.40 678.33 72.00 191.69

Info Edge 684.40 3,736.17 294.01 83.97 463.64Cox & Kings 213.40 2,913.51 235.66 76.72 1,477.27

Tube Investment 141.65 2,632.85 2,981.10 169.66 1,715.20Guj NRE Coke 27.30 1,576.22 1,593.94 101.83 3,108.28Gateway Distri 137.75 1,488.84 187.60 85.17 688.24

CenturyPlyboard 62.55 1,391.91 931.70 74.51 489.42Thomas Cook 47.80 1,012.78 267.02 41.54 505.10

ICRA 926.15 926.15 129.31 44.91 242.34Nitin Fire Prot 142.40 897.34 147.67 23.72 174.32

Karuturi Global 9.30 749.12 31.79 9.52 1,130.71

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 7/14

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 8/14

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 9/14

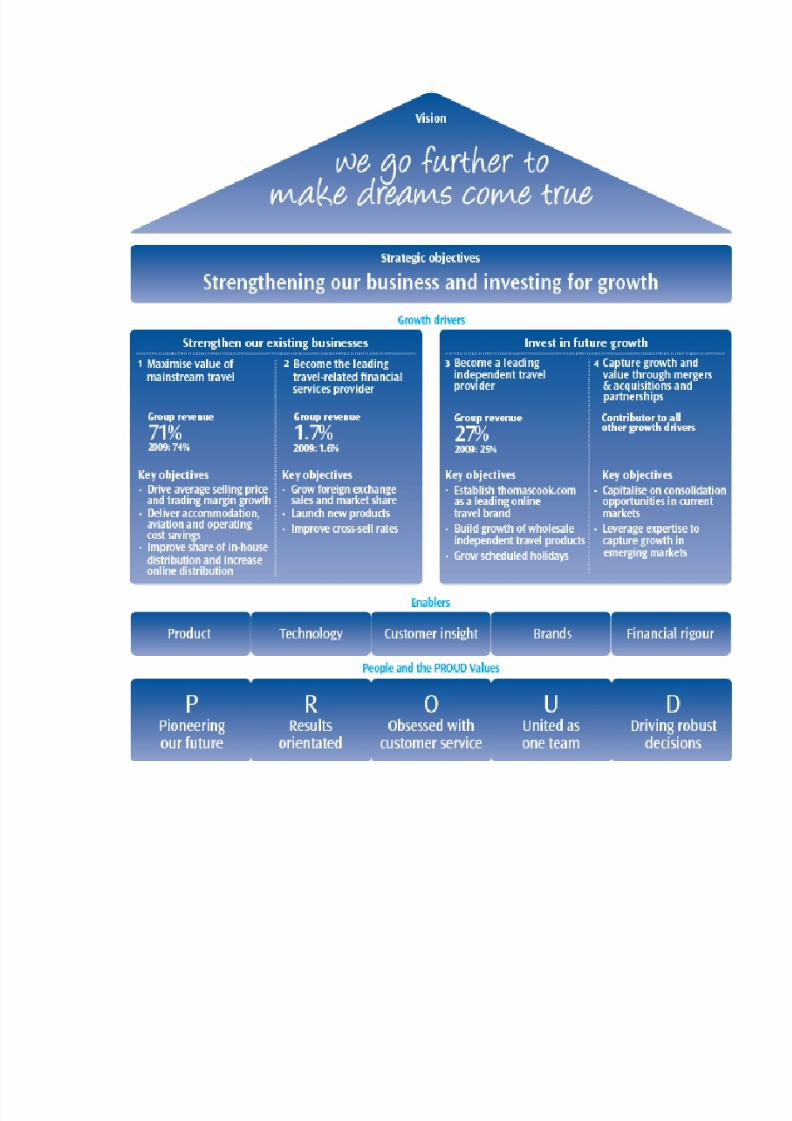

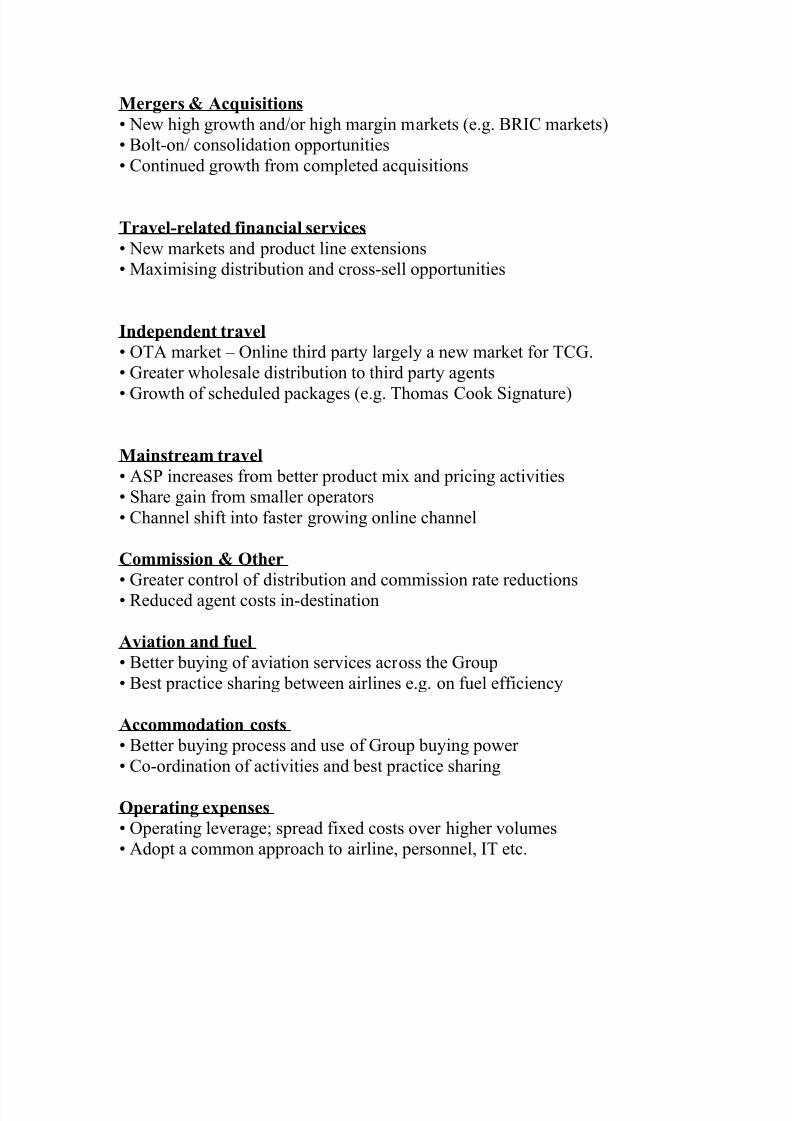

Mergers & Acquisitions• New high growth and/or high margin markets (e.g. BRIC markets)• Bolt-on/ consolidation opportunities• Continued growth from completed acquisitions

Travel-related financial services• New markets and product line extensions• Maximising distribution and cross-sell opportunities

Independent travel• OTA market – Online third party largely a new market for TCG.• Greater wholesale distribution to third party agents

• Growth of scheduled packages (e.g. Thomas Cook Signature)

Mainstream travel• ASP increases from better product mix and pricing activities• Share gain from smaller operators• Channel shift into faster growing online channel

Commission & Other• Greater control of distribution and commission rate reductions• Reduced agent costs in-destination

Aviation and fuel• Better buying of aviation services across the Group• Best practice sharing between airlines e.g. on fuel efficiency

Accommodation costs• Better buying process and use of Group buying power • Co-ordination of activities and best practice sharing

Operating expenses• Operating leverage; spread fixed costs over higher volumes• Adopt a common approach to airline, personnel, IT etc.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 10/14

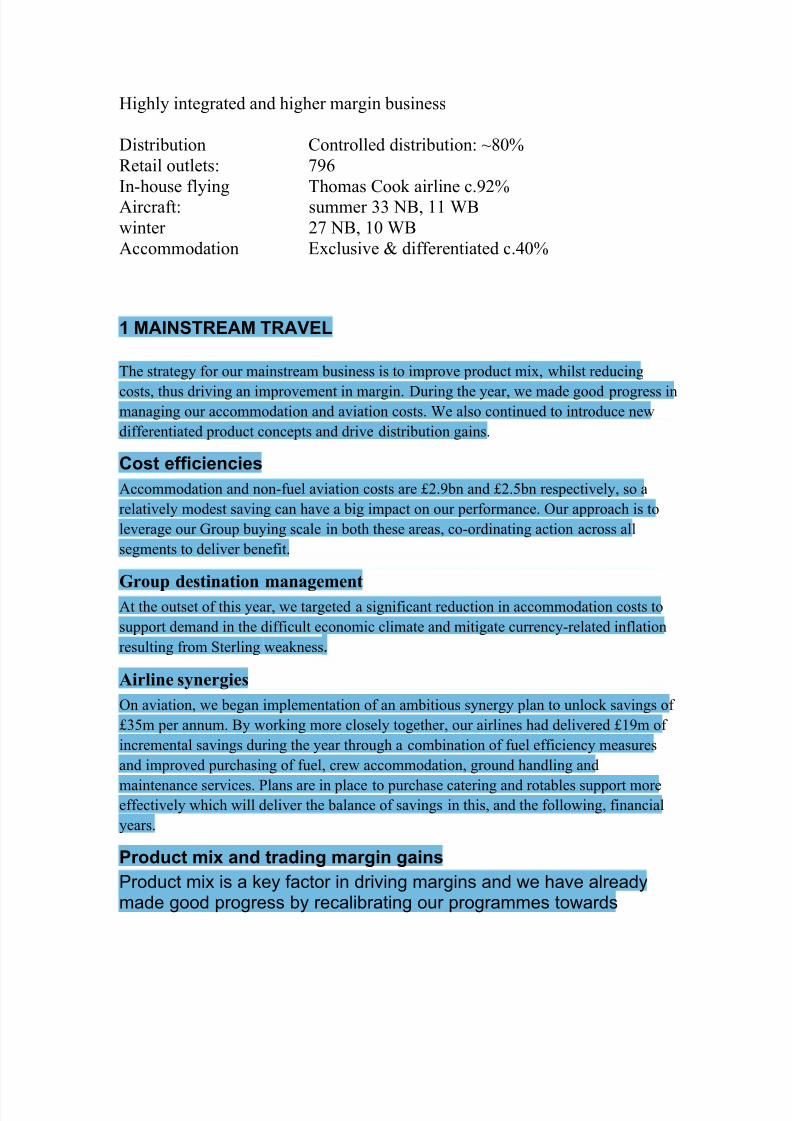

Highly integrated and higher margin business

Distribution Controlled distribution: ~80%Retail outlets: 796In-house flying Thomas Cook airline c.92%Aircraft: summer 33 NB, 11 WBwinter 27 NB, 10 WBAccommodation Exclusive & differentiated c.40%

1 MAINSTREAM TRAVEL

The strategy for our mainstream business is to improve product mix, whilst reducing

costs, thus driving an improvement in margin. During the year, we made good progress inmanaging our accommodation and aviation costs. We also continued to introduce newdifferentiated product concepts and drive distribution gains.

Cost efficienciesAccommodation and non-fuel aviation costs are £2.9bn and £2.5bn respectively, so arelatively modest saving can have a big impact on our performance. Our approach is toleverage our Group buying scale in both these areas, co-ordinating action across allsegments to deliver benefit.

Group destination managementAt the outset of this year, we targeted a significant reduction in accommodation costs tosupport demand in the difficult economic climate and mitigate currency-related inflationresulting from Sterling weakness .

Airline synergiesOn aviation, we began implementation of an ambitious synergy plan to unlock savings of £35m per annum. By working more closely together, our airlines had delivered £19m of incremental savings during the year through a combination of fuel efficiency measuresand improved purchasing of fuel, crew accommodation, ground handling and

maintenance services. Plans are in place to purchase catering and rotables support moreeffectively which will deliver the balance of savings in this, and the following, financialyears.

Product mix and trading margin gainsProduct mix is a key factor in driving margins and we have alreadymade good progress by recalibrating our programmes towards

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 11/14

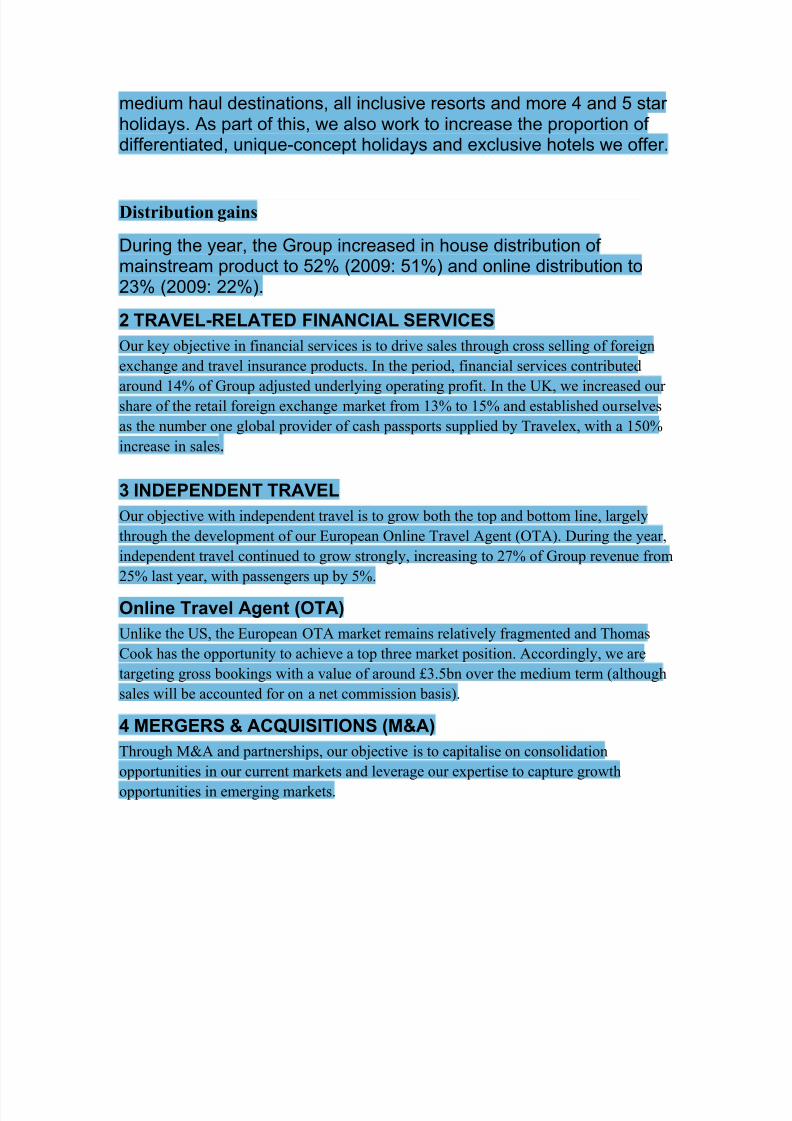

medium haul destinations, all inclusive resorts and more 4 and 5 star holidays. As part of this, we also work to increase the proportion of differentiated, unique-concept holidays and exclusive hotels we offer.

Distribution gains

During the year, the Group increased in house distribution of mainstream product to 52% (2009: 51%) and online distribution to23% (2009: 22%).

2 TRAVEL-RELATED FINANCIAL SERVICESOur key objective in financial services is to drive sales through cross selling of foreignexchange and travel insurance products. In the period, financial services contributed

around 14% of Group adjusted underlying operating profit. In the UK, we increased our share of the retail foreign exchange market from 13% to 15% and established ourselvesas the number one global provider of cash passports supplied by Travelex, with a 150%increase in sales .

3 INDEPENDENT TRAVELOur objective with independent travel is to grow both the top and bottom line, largelythrough the development of our European Online Travel Agent (OTA). During the year,independent travel continued to grow strongly, increasing to 27% of Group revenue from25% last year, with passengers up by 5%.

Online Travel Agent (OTA)Unlike the US, the European OTA market remains relatively fragmented and ThomasCook has the opportunity to achieve a top three market position. Accordingly, we aretargeting gross bookings with a value of around £3.5bn over the medium term (althoughsales will be accounted for on a net commission basis).

4 MERGERS & ACQUISITIONS (M&A)Through M&A and partnerships, our objective is to capitalise on consolidationopportunities in our current markets and leverage our expertise to capture growthopportunities in emerging markets.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 12/14

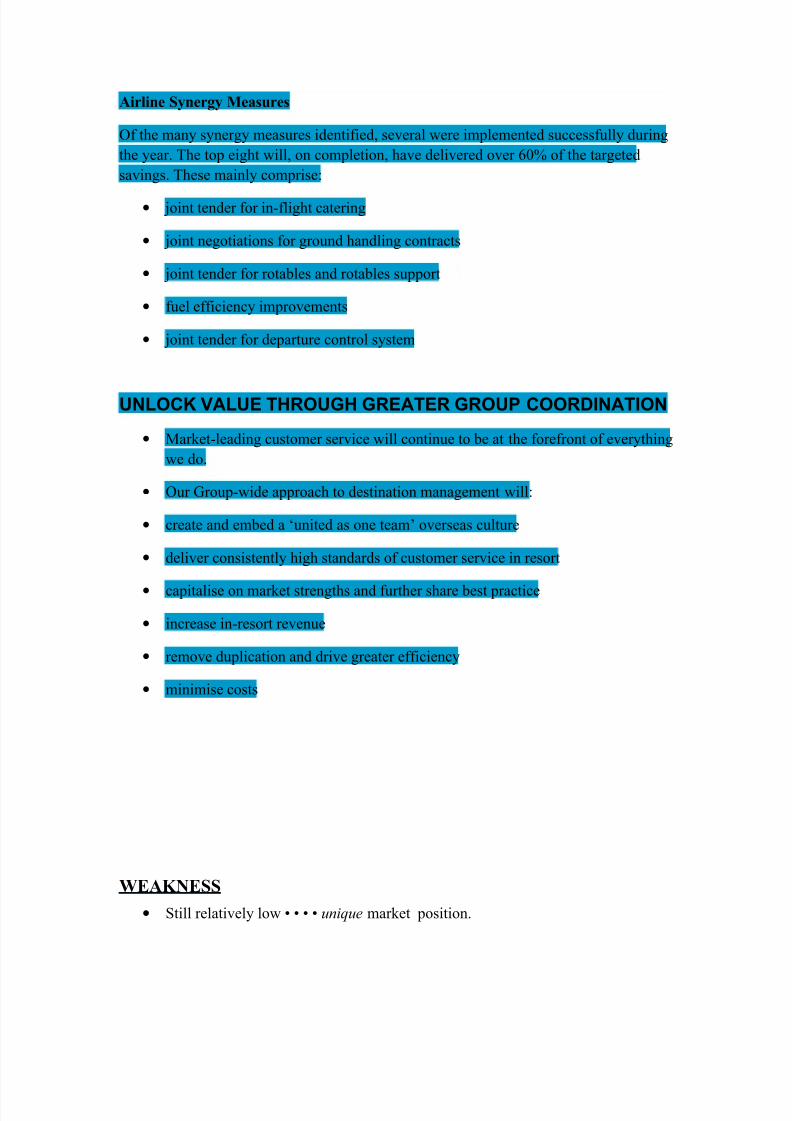

Airline Synergy Measures

Of the many synergy measures identified, several were implemented successfully duringthe year. The top eight will, on completion, have delivered over 60% of the targetedsavings. These mainly comprise:

• joint tender for in-flight catering

• joint negotiations for ground handling contracts

• joint tender for rotables and rotables support

• fuel efficiency improvements

• joint tender for departure control system

UNLOCK VALUE THROUGH GREATER GROUP COORDINATION

• Market-leading customer service will continue to be at the forefront of everythingwe do.

• Our Group-wide approach to destination management will:

• create and embed a ‘united as one team’ overseas culture

• deliver consistently high standards of customer service in resort

• capitalise on market strengths and further share best practice

• increase in-resort revenue

• remove duplication and drive greater efficiency

• minimise costs

WEAKNESS• Still relatively low • • • • unique market position.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 13/14

• Lack of adequate infrastructure. The airlines in India, for example, are inefficientand do not provide basic facilities at airports. The road condition in India is very

bad.• No proper marketing of India's tourism abroad.•

Foreigners still think of India is one of poverty, superstition, and diseases.• The case of plague in Surat in 1994 led to decrease of 36% in arrival of foreign

tourists in India.• Focus on higher margin products.• Yield management improvements.• Growing strong independent Travel proposition.• Strengthening financial services position.• Increase controlled distribution from 83% to 90% and online from 54% to 80%.• Increase share of concept hotels from 25% to 30% of total bed capacity.• Improve value proposition to grow the family and 50+ segments.• Grow independent travel business, focusing on major destinations.• Continue cost efficiencies, reducing overheads and commissions.

Opportunities

• Leading Tour Operator with strong distribution:• Multi-destination Tour Operator .• Retail focus on key regions.• Leveraging core destinations.• Leverage existing expertise:• Brand• strong positions in key destinations.• More proactive role from the government of India in terms of framing policies.• Allowing entry of more multinational companies into the country giving us a

global perspective.• Growth of domestic tourism. The advantage here is that domestic tourism and

international tourism can be segregated easily owing to the different in the periodof holidays.

•

Continue focus on duty free sales in the airline.• Maximise the value of mainstream .• Become a leading independent travel provider .• Become the leading travel-related financial services provider .

Threats

• Major travel markets continue to grow faster than the general economy.

8/4/2019 AKASH SWOT 1

http://slidepdf.com/reader/full/akash-swot-1 14/14

• Intermediaries continue to capture around a third of total expenditure .• Mainstream travel market will continue to be large and togrow in value terms.• Independent travel to drive majority of the growth in the intermediary market.

• Online growth will be faster than offline; growth in both mainstream andindependent.

• Consumers will continue to drive change in the industry.• Political turbulence within India in Kashmir and Gujarat has also reduced tourist

traffic.• Aggressive strategies adopted by other countries like Australia, Singapore in

promoting tourism